The Big Idea

Lessons learned in corporate credit 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

Investment grade corporate bond spreads took a round trip in 2025 going from Liberation Day wides to the early fall tights. The index eventually landed net tighter by a few basis points to leave excess return positive at 1.09% and cap off a moderate year of 7.4% total returns. Over that run, the timing on individual credit calls and macro relative value plays was critical. A look back at some of those recommendations provides insight into how those strategies stand today and guidance for the future.

#1: Higher beta insurance brokers were a solid trade in 2025

While an overweight to the segment was a relative win in 2025, going forward the trade looks increasingly crowded, stretching valuations and suggesting more of a market weight allocation.

Insurance brokerage credits have remained a favored segment of the broader insurance sector given their relative stability to traditional property and casualty names. As traditional P&C underwriters had struggled in recent years to bear catastrophe costs, those market conditions have helped the profitability of global insurance brokers. Furthermore, ongoing interest rate volatility still creates investment portfolio risk that more directly impacts insurance underwriters. The biggest credit risk to the industry has been the prospect of debt-funded M&A growth.

Santander US Capital Markets recommendations:

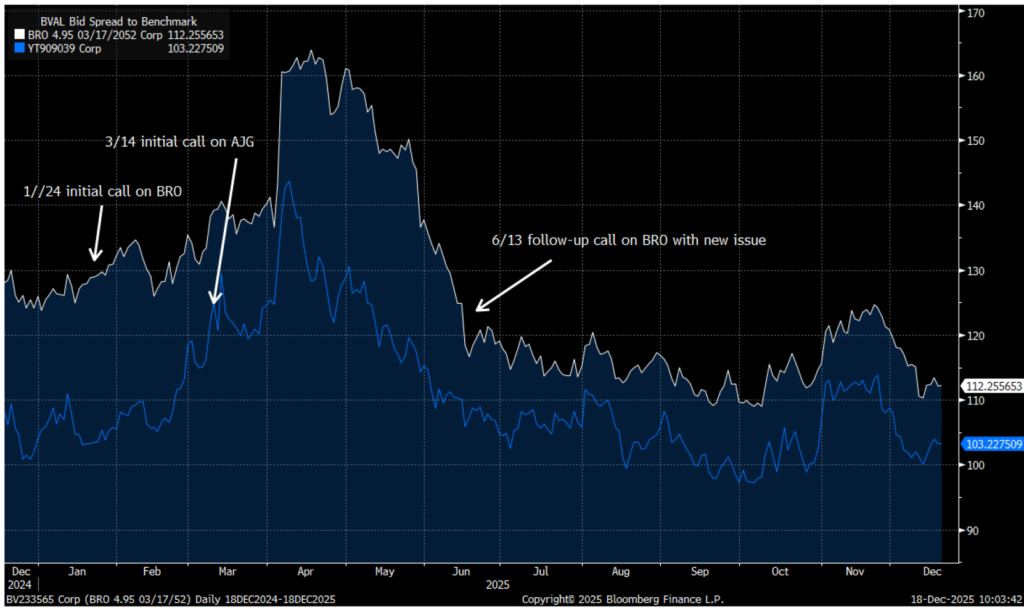

The segment performed relatively well throughout the year, benefitting names with more sensitivity to market conditions (BRO and AJG vs AON or MMC) as investors sought to add more credit risk in a favored operating environment (Exhibit 1). The most disruptive credit event was when BRO launched a 6-part debt launch funding package for their $9.8 billion June acquisition of RSC/Accession. They priced just over $4 billion for deal financing with the rest coming from an equity raise ($4 billion) and cash on hand. The bonds performed well in the days following their debut and existing debt only experienced a little bit of pressure with the announcement. Management remains committed to investment grade ratings. The acquisition boosted leverage to about 3.5x from in the 2x to 2.5x range, and the company is committed to deleveraging over the next several years.

Exhibit 1: BRO (white) and AJG (blue) 30-year note spread performance

Source: Santander US Capital Markets LLC, Bloomberg/TRACE BVAL Bid indications

#2: Surplus notes gather momentum, and a few caveats

Surplus notes largely performed well throughout 2025 as trading volume and investor demand ebbed and flowed with Treasury moves and rate expectations. Going forward, there is cause for more caution in the segment until Mass Mutual’s SEC investigation into potential accounting issues is resolved.

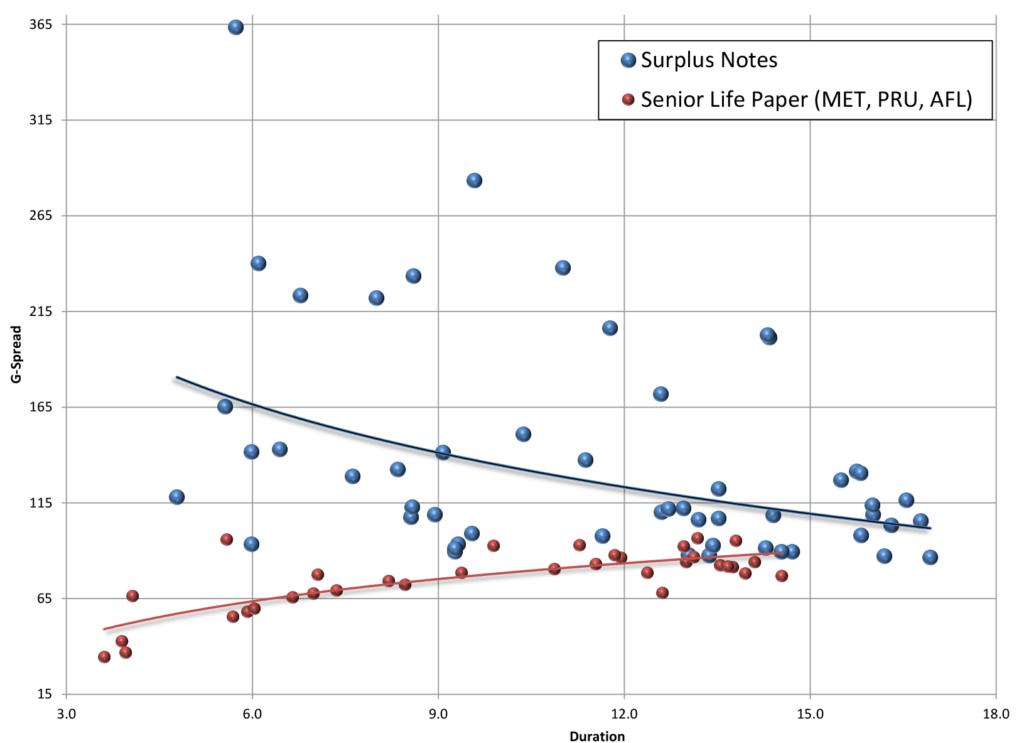

Insurance company surplus notes offer a way for investors to target higher (often ‘AA’) ratings while potentially adding spread over comparable or lower-rated senior unsecured notes issued by public insurance companies. While the spread between surplus notes and senior, publicly issued benchmarks has compressed over the years, these structures still allow conservative investors to get exposure to higher-rated credits in the long-end of the curve, without conceding much spread (Exhibit 2). There was limited new issued this year (below) but there still seems opportunity for growth ahead, and surplus issuers often come in waves.

Santander US Capital Markets recommendations:

MASSMU is one of the prominent issuers in the space. Earlier this year, the SEC raised concerns about the insurer’s investment accounting practices. The investigation is ongoing, with the SEC issuing subpoenas regarding the company’s bookkeeping related to billions of dollars of loans held in its general investment account. The concern for surplus notes is if accounting irregularities do exist and, in a worst-case scenario, results in a delay of payment on MASSMU’s coupons. That would likely cause the segment to reassess risk in surplus notes, serving as a reminder to investors that despite high ratings overall, the securities qualify as hybrid capital. At a minimum, investors should exercise a little more caution around the sector, particularly given that liquidity on these securities can fluctuate highly with interest rates.

Exhibit 2: Surplus notes compared to senior unsecured life insurance paper

Source: Santander US Capital Markets LLC, Bloomberg/TRACE BVAL G-spread indications

#3: Mixed results in JDE Peets and Keurig Dr Pepper

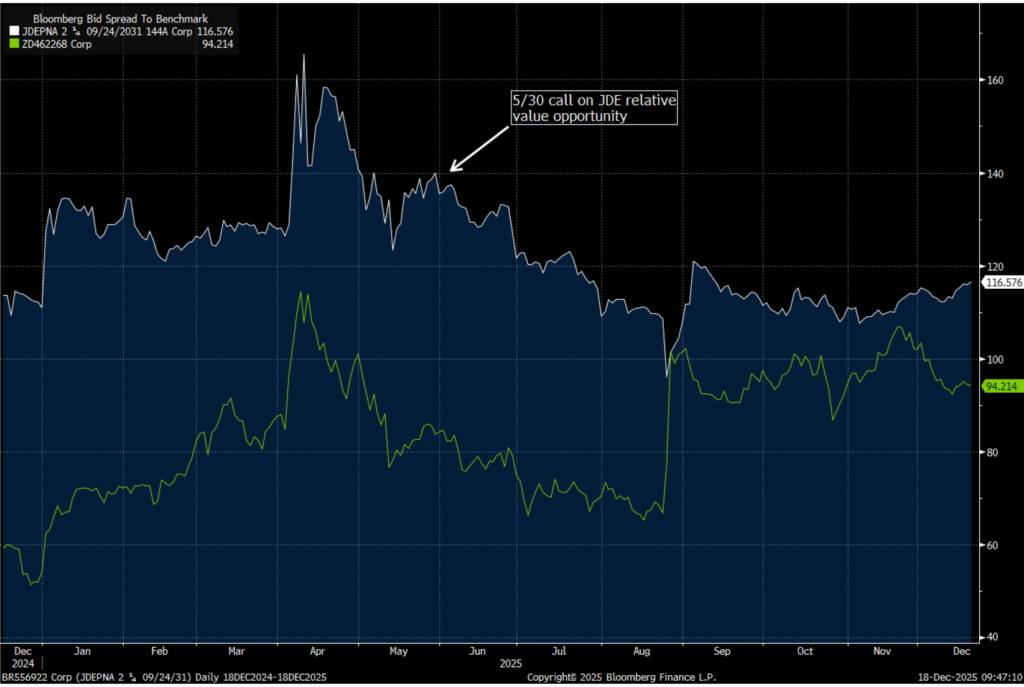

The call on JDE Peet (JDEPNA: Baa3/BBB-/BBB*-) in May worked as a function of timing with spreads still wide following April tariff concerns. But the announcement of the debt-funded acquisition by Keurig Dr Pepper (KDP: Baa1*-/BBB*-/BBB-) and spin-off plans in August served as a major credit event that will influence valuation going forward that were not part of that stand-alone recommendation. Going forward there does appear to be some attractive compression available in JDEPNA relative to KDP paper (exhibit 3), but the fundamental risks of the eventual combined entities and spin-off plans are worrisome.

Santander US Capital Markets recommendation:

The all-cash merger carries a transaction value of approximately $22.7 billion with equity valuation of roughly $18.1 billion. Pro forma net leverage for the combined company is north of 5.0x, with plans to spin off the combined coffee operations into a separate entity. Management has indicated that is committed to IG ratings at both eventual issuers, while the agencies have indicated low-BBB outcomes. The acquisition is expected to close within the first half of the coming year, with the tax-free spin-off coming later. The prospective debt issuance on the horizon and eventual debt issuance at CoffeeCo bring too much technical supply to suggest anything other than a marketweight approach to the KDP complex.

Exhibit 3: JDEPNA ‘31s (white) and KDP ‘31s (green) 1-year spread performance

Source: Santander US Capital Markets LLC, Bloomberg/TRACE BVAL Bid indications

#4: Net supply matters

During two of the slower issuance months of 2025 (May-June), the investment grade index saw two consecutive months of net negative supply to par value. It appeared then that may be keeping spreads artificially tight. And while temporarily true as spreads reached their local tights in September at a spread of 72 bp over the Treasury curve, new issue rapidly increased setting three consecutive months of record gross volume in Sept – Nov contributing to wider spreads over that stretch (Exhibit 4) before settling lower in December.

Santander US Capital Markets recommendations:

The huge new issue calendar was a big story for 2025 as gross new issue volume of $1.659 trillion was the most in any year since 2022. There is a broad range of expectations for both gross and net new issue volume in 2026, running from as low as $1.4 trillion to as high as $2.2 trillion. Most are leaning toward another banner year with the tech sector expected to lead the way on further AI infrastructure buildout. With that in mind, trying to time seasonal or monthly lulls in net issuance seems a difficult strategy to pursue in the year ahead.

Exhibit 4: Index size by par value (white) and spread performance (blue)

Source: Santander US Capital Markets LLC, Bloomberg LP

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.