The Big Idea

Shifting forces in housing

Stephen Stanley | August 5, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

The housing market is currently subject to a mix of unusually strong forces pushing in opposite directions. Cyclical forces are creating short-term weakness as soaring home prices and surging mortgage rates have cut housing affordability dramatically. Home sales have consequently declined in recent months and may remain soft for a while. Nonetheless, underneath the short-term gyrations, longer-term secular forces continue to point to a housing market that is undersupplied. After a period of adjustment, the housing sector should find its footing far more easily than it did after the Global Financial Crisis, when there was a significant excess supply left over from the 2004-2006 boom.

Affordability problems

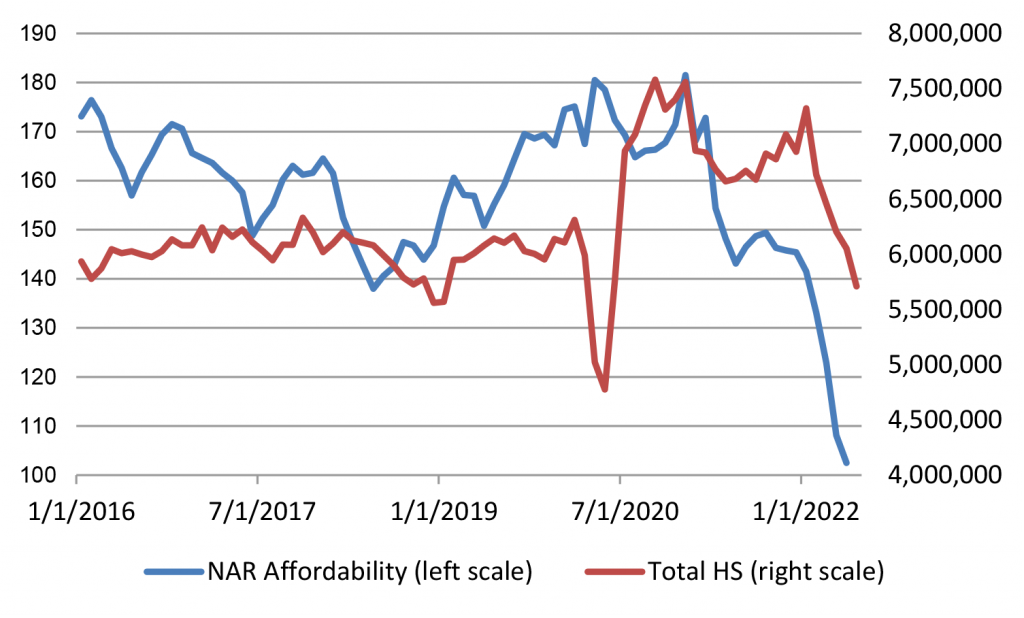

The slowdown that we are seeing in the housing market in 2022 is mainly induced by a precipitous drop in affordability. Home prices have surged since the early days of the pandemic. On top of that, mortgage rates shot up in early 2022, with the 30-year mortgage rate nearly doubling from the turn of the year to its recent peak in June. The impact shows up by tracking home sale—combined existing and new home sales—and the National Association of Realtors affordability gauge, which is based on the median level of personal income weighed against the cost of buying a home, which mainly reflects home prices and mortgage rates (Exhibit 1).

Exhibit 1: Housing affordability versus home sales

Source: NAR, Census Bureau.

Tracking home sales against affordability shows clearly why home prices have weakened in the first half of the year, and it suggests that further declines may be likely. Broadly, however, the affordability issue should be self-correcting over time. If housing demand weakens, home price appreciation should moderate. In addition, if the overall economy cools, mortgage rates would be expected to drop. In fact, the 30-year rate has already declined to around 5% from a peak of about 5.80% in June. While the housing sector is exhibiting weakness at the moment and may continue to do so for a while, cycles, by their nature, come and go.

Secular forces

Over a longer horizon, the tone of the housing market is governed by supply and demand trends. Key factors include population growth, household formation, and the cost and availability of land, materials, and skilled construction labor. For example, the housing industry boomed in the 1970s because the massive Baby Boomer generation reached the age when they began to buy homes. Housing starts exceeded 2 million regularly in the 1970s, a level never reached since, including during the 2000s Housing Boom (even with a larger overall population level).

Prior to the pandemic, the housing market was generally considered tight, with firm prices and thin inventories. Home builders never fully reconstituted the capacity to build seen during the 2000s, as skilled labor moved to other industries during the lean years of the bust and buildable lots became increasingly difficult to find (and expensive) in some parts of the country.

Nonetheless, things could have been better. For years, analysts projected that the large age cohorts representing the children of Baby Boomer parents, who had reached the traditional age of first-time home buyers, would move out of their apartments and into single-family homes. However, this generation got married at a later age, had kids at a later age, and thus waited until a later stage of life to seek larger accommodations. That demographic wave was just starting to show itself before Covid hit.

The pandemic fundamentally altered the course of the housing sector. The combination of a desire to social distance and the massive shift toward an acceptance of remote work led to meaningful changes in housing demand.

Many families moved from urban apartments to larger homes in suburbs or even rural areas. From a unit perspective, that one-for-one trade need not affect the quantity of housing units needed, though it may generate an increase in the aggregate dollar value of housing construction (since single-family homes are, as a rule, more expensive to build per unit than apartment buildings).

More importantly, more people sought their own place. Much of the doubling and tripling up that had been increasingly common in the 2010’s, whether it be multiple generations of families living together (including the iconic young adult living in his or her parents’ basement) or a group of young friends cramming 5 or 6 people into a three-bedroom apartment, suddenly lost its appeal.

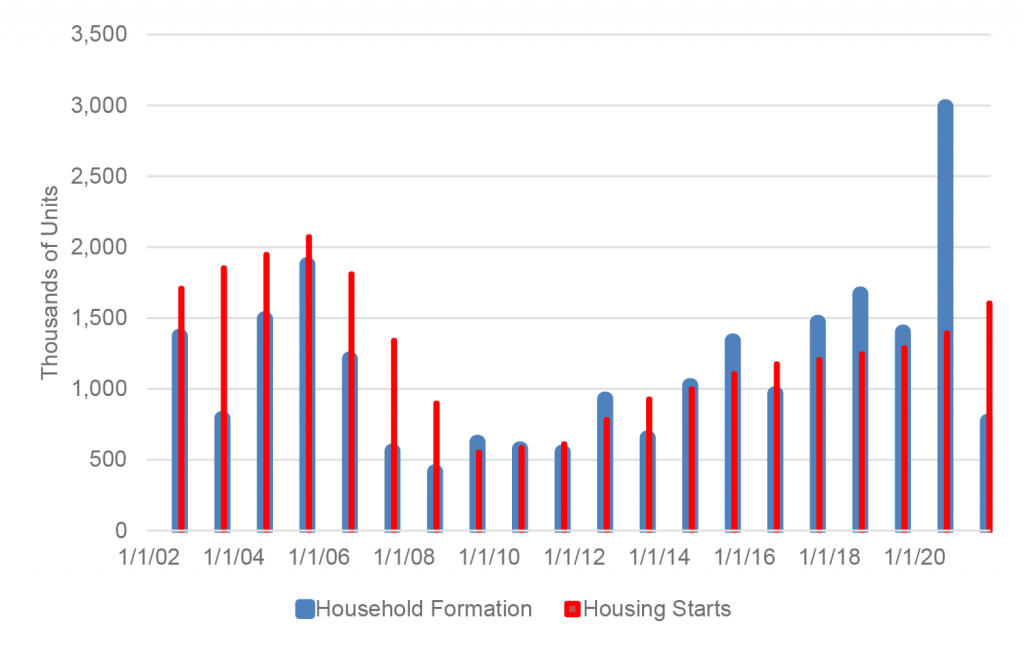

Imbalances between demand and supply shows in the annual rate of household formation in relation to housing starts (Exhibit 2). As noted above, supply was already arguably behind demand before the pandemic. This can be seen in the fact that household formation generally grew faster in the late 2010s than housing starts. It should be the other way around, as some percentage of housing starts are replacements for units that were demolished or destroyed by fire or natural disaster. Traditionally, 200,000 to 300,000 units are permanently lost each year. Thus, in theory, housing starts should exceed household formation by about that amount.

Exhibit 2: Household formation and housing starts

Source: Census Bureau.

In any case, the pandemic threw the housing market far out of balance. Household formation, which had averaged between 1.3 million and 1.4 million per year over the prior five years, spiked to 3 million in 2020. That means that the demand for housing units surged by an extra 1.7 million or so above and beyond the normal rate of growth. Builders were constrained during the pandemic. Housing starts did increase, even in 2020, but it will take builders years to catch up to the massive shift in demand for homes that took place in 2020.

It is worth looking at the latest figures and considering how much of the supply-demand gap created by the pandemic has been filled. There are two dynamics here that will help to close the imbalance. First, not all of the moves made during 2020 will be permanent. For example, some households may have procured second homes in remote locations during the worst days of the pandemic with the intent to revert back to their pre-COVID homes when the dust settled. In contrast, some of the shifts seen in 2020 will prove persistent. Then, of course, on the supply side, builders can be expected to step in over time and build more homes.

On the demand side, household formation did in fact moderate in 2021 to around 800,000, well below the pre-pandemic norm. The data for the first half of 2022 would equate to about a 1.1 million annual pace. Thus, if we assume that the pre-COVID benchmark was 1.3 million per year, then, of the 1.7 million excess in 2020, close to 700K has been reversed over the subsequent year and a half. That still leaves demand about 1 million units ahead of where it might have been if the pandemic had not occurred. Presumably, that figure may come down somewhat further over the next few years.

On the supply side, housing starts did step up in 2020 and 2021. The annual pace in 2020 of 1.4 million, even with the public safety restrictions imposed on activity in the spring of that year, was modestly higher than in previous years. Then, last year, housing starts surged to 1.6 million, the highest annual tally since 2006.

Still, if the underlying pace of household formation is 1.3 million to 1.4 million, then, in light of the loss rate of housing units, housing starts would need to run in the 1.6 million range simply to keep up. This should maintain a decent floor under housing activity going forward.

The extreme pressure in the housing market seen up until a few months ago, as evidenced by surging home prices, rock-bottom inventories, and bidding wars, represented in part a cyclical response, as household balance sheets have been flush and mortgage rates were historically low. However, the bulk of the impetus was likely a result of a persistent rise in demand for housing, independent of the business cycle. Once the economy works through the current housing recession, those positive fundamentals should re-emerge.