The Big Idea

Special Report: Risk and reward as data centers tap the debt markets

Steven Abrahams and Dan Bruzzo, CFA | May 8, 2026

This material is a Marketing Communication and does not constitute Independent Investment Research.

Surging demand for computing power has set off one of the biggest waves of capital spending in decades. Planned investment in data centers and related technology already stands at $656 billion this year. Demand for capital has started to outstrip the ability of equity or operating cash flow to deliver, and the debt markets are seeing the impact. Exposure to data centers and related infrastructure already shows up in investment grade and high yield debt, leveraged loans and private debt, ABS and CMBS. Each market is likely to see good performance in the bullish case. But in the bearish cases, each market might be unhappy in its own way.

The risks for issuers and investors fall into a few major categories:

- Execution risk in finding land, engaging community support, building data centers and outfitting them with computing capacity, power and cooling

- Obsolescence risk in maintaining the value of the completed facility as computing algorithms, CPUs and GPUs, cooling and power technology evolve

- Supply and demand risk as the supply of computing capacity and the demand for it fluctuate

- Guarantor and counterparty risk from third-party guarantees of data center cash flows, market value or both and from leases that secure the same, and

- Complexity risk from transactions where guarantees, structural subordination, cash flow performance triggers and other mechanisms provide credit support

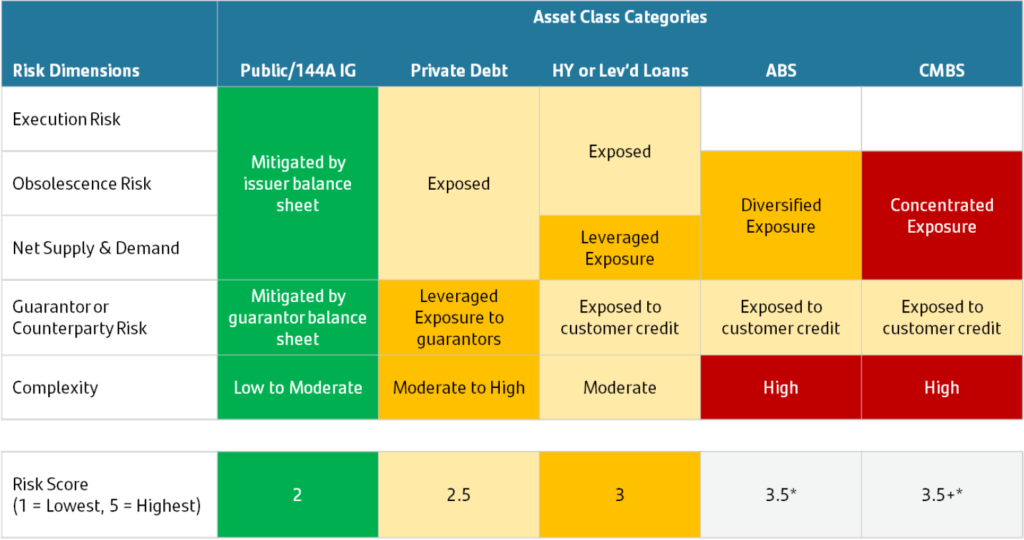

The risks do not fall equally across the different markets (Exhibit 1). In particular:

- Execution risk falls mainly on corporate issuers using debt proceeds to build data or outfit centers, with ABS and CMBS relying on completed facilities with current cash flow

- Obsolescence and supply and demand risk fall across all debt markets, although sensitivity ranges from low in public investment grade debt to high in single-asset single-borrower CMBS

- Exposure to guarantors and counterparties also falls across all markets although sensitivity varies from low with guaranteed debt to moderate in ABS and CMBS secured by leases, and

- Complexity also applies across executions varying again from low in public investment grade debt to high with ABS and CMBS

Exhibit 1: Key risks in data center debt and the sensitivity of different debt forms

Note: ABS and CMBS should trade at a spread concession to corporate debt of the same rating, but issuers may still issue ABS and CMBS on properties with cash flow because of the ability to source debt at ratings higher than the data center owner or sponsor.

Individual issuers, deals and structures will vary in exposure across these risk dimensions within each asset category. But this broad map of risk and its market impact suggests overall risk for now varies from lower to higher across public investment grade, private debt, high yield and leveraged loans, ABS and CMBS.

All else equal, spreads should reflect the variation in risk, and current spreads roughly do. Spreads at any rating category generally are tighter for corporate issues and wider in ABS and CMBS, those markets compensating generously for complexity.

In the likely bullish case over the next few years where demand for computing power continues to outstrip supply and where new technology does not suddenly displace old, all diversified forms of exposure to data centers and their infrastructure should perform well. The bullish incentive is to take as much diversified spread exposure as possible. But at longer horizons, the balance between supply and demand becomes less clear and the potential for disruption rises. The bearish incentive is to take less risk at longer horizons. That would tilt relative value toward public investment grade debt with longer maturities, and ABS instead of CMBS.

The rest of this note lays out the details and rationale for this approach to relative value across US debt market exposurse to data centers and related technology. It continues in the following sections:

- The race for computing power

- Data centers as utilities

- Location matters

- Reliability matters

- The cost to build

- Own or lease

- Funding the big build

- Funding out of cash flow

- Funding out of investment grade debt

- Funding out of high yield debt and leveraged loans

- Funding out of private debt

- Funding out of ABS

- Funding out of CMBS

- Current risk, spread and relative value

The race for computing power

The current race to build computing power is starting to compare to other watershed moments in US economic growth. Railroads. Electrification. Highways. Telecom and fiber. If actual investment over the next five years meets current expectations, the building of computing power and related technology will join this list. There are early signs. In the last quarter of 2025, which included a damaging federal government shutdown, investment in technology accounted for all of US GDP growth.

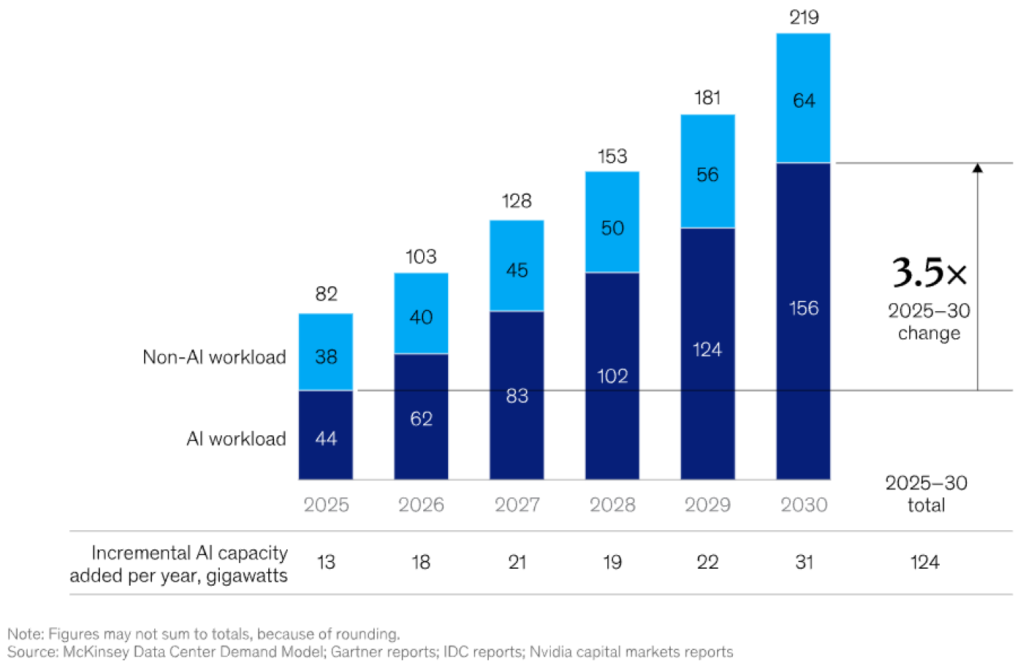

At the heart of the race are the computing demands of AI. Consulting firm McKinsey estimates that AI today consumes 53% of the 82 gigawatts in current worldwide computing workload (Exhibit 2). AI workload alone could more than triple in the next five years, according to McKinsey, rising from 44 gW to 156 gW. Worldwide demand could approach 220 gW by 2030.

Exhibit 2: AI and non-AI workload should drive data center demand

Note: AI workload includes training and inference. Non-AI workload includes cloud computing, streaming, social media, ecommerce and other uses.

The demand for this processing is led by a handful of companies trying to win at least a niche if not more in a world with increasing use of AI. Companies directly facing AI users, known as hyperscalers, include Meta along with Alphabet (Google), Amazon, Microsoft, Oracle, Alibaba and ByteDance. Companies offering infrastructure, known as neoclouds, include CoreWeave, Crusoe, FluidStack, Lambda, Nebius and Nscale.

Data centers turn out to be the modern factory for turning information into AI and other technology products. But building modern data centers takes significant capital. The hyperscalers alone have announced plans to invest $656 billion in data centers and other AI infrastructure this year, putting pressure on operating cash flow and pushing them toward the debt markets to help fund the investment.

Issuers of debt in this race can now choose from a range of markets including investment grade and high yield debt, leveraged loans and private credit, ABS and CMBS. Investors across these markets face varying forms of exposure to data centers and related infrastructure and varying risks. Issuers and investors across these markets appear likely to face important choices for years.

Data centers as utilities

Data centers have long served as utilities for storing, processing and managing information. Before the surge in AI, they served providers of cloud computing, social media, ecommerce, streaming, wireless telecommunications and others. Companies doing AI training and AI inference are just the latest customers.

A center physically has some components provided by the owner and others provided by the user, who may also own the center. The owner provides components with longer average lives, according to Green Street, including the land, building, cooling and power systems. The user provides components with shorter average lives including computer servers, networking equipment and storage.

Each of these components has a different useful life depending on evolving technology and user needs, with power consumption and systems a good example. A standard 42-server computer rack using legacy NVIDIA chips for cloud computing might run on 5 to 10 kilowatts (kW) of electricity, according to NVIDIA. Upgrade to the NVIDIA Hopper and Blackwell chips needed for generative AI, and consumption rises to 60 to 80 kW. Upgrade again to the NVIDIA Vera Rubin chips used for next-gen AI and consumption goes to 130 to 250 kW or more. To put this in context, the US Energy Information Administration indicates the average US household draws 1.2 kW.

Demand for power traditionally has required plugging into the local power grid, but limits to local grid capacity, concern about reliability and periodic opposition from local communities has led some new data centers to build their own power plants and battery installations to make them more independent from local power sources.

Rising power consumption raises the bar for cooling. Older data centers today might still use cold air cooling for 10 to 15 kW racks. Upgraded centers might use heat exchangers that put water-cooled panels at the exhaust vents of each rack to handle 20 to 30 kW. New data centers designed for AI training and inference today often use direct circulation of coolant through cold plates on CPUs and GPUs to handle 100 kW. Advanced approaches include coolant piped directly to a cold plate on each chip or having servers submerged in dielectric fluid for handling up to 200 kW or more.

Location matters

Like any piece of real estate, location matters for data centers. Access to power and water, ability to find or replace tenants, time latency between AI user prompt and response and even local government support or opposition all matter.

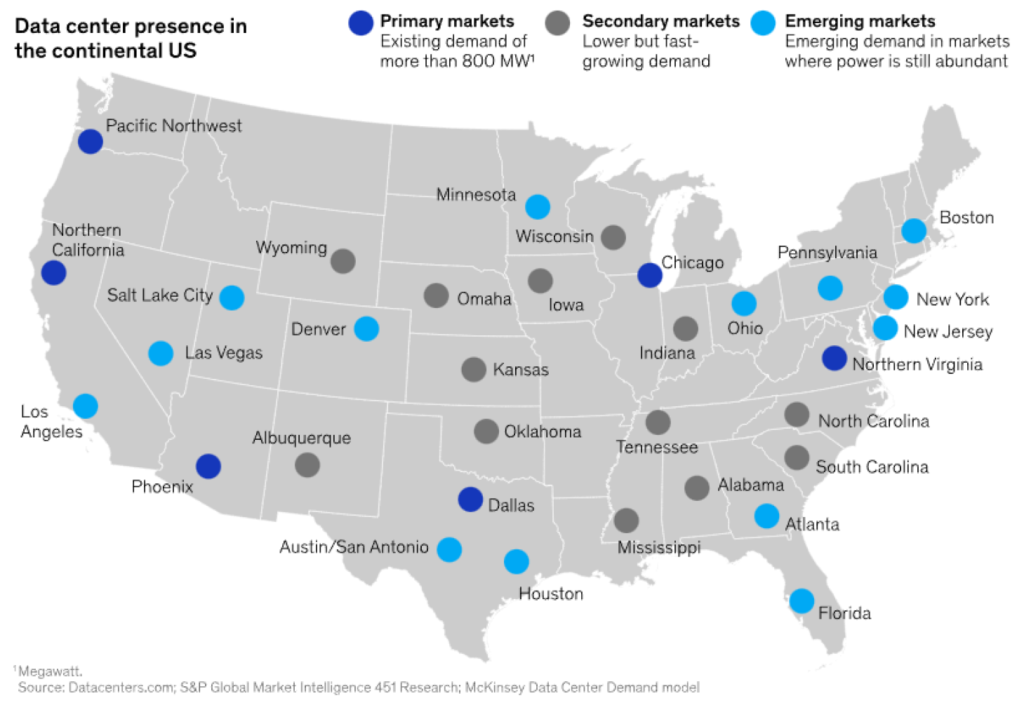

Tier 1 locations currently include Northern Virginia, Silicon Valley, Seattle, Phoenix, Chicago, Dallas and similar locations (Exhibit 3). These all offer good access to power and water and most importantly have the highest prospect of finding another tenant if the original tenant backs out or cannot fulfill lease obligations.

Tier 2 locations include Atlanta and Houston, for example, and Tier 3 locations include Raleigh, NC, Nashville, TN and Oklahoma City. These all boast lower land and power costs than Tier 1 but with less power available and with limited carriers and interconnection.

Exhibit 3: Data center location matters

Source: McKinsey & Co.

The data center market also distinguishes between locations close to population centers where latency in response to AI prompts is low and locations far away with higher latency. Closer locations may be best for AI inference, farther locations for AI training.

Meta, for example, has 30 locations across different markets in the US and internationally. Some of the more prominent:

- The Hyperion AI Campus in Richland Parish, LA, which started development in late 2025 with an expected cost of $27.3 billion and is specifically designed for large-scale AI model training.

- Boone County, IN, a roughly $10 billion investment, is expected to bring 1 gW online in 2026 and is also designed to facilitate AI-ready computing.

- The Kansas City Northland Campus, where Meta invested over $1 billion, with multiple data center buildings, chosen for strong grid reliability, connectivity and local staffing talent.

- Other noteworthy Meta locations include Altoona, PA, New Albany, OH, Sarpy County, NB, Dekalb, IL, Huntsville, AL, Newton County, GA, Eagle Mountain, UT, Mesa, AZ and Temple, TX.

Reliability matters

The Uptime Institute has developed a system for classifying data centers into different tiers based on operating reliability. Tier I and II centers offer limited if any redundancies, leaving multiple points of failure and taking them out of the running for any user with mission-critical jobs. Tier III, the minimum standard for mission-critical applications, allows servicing of any component without taking the center offline but is still vulnerable to equipment failure or operator error. Tier IV keeps running through major equipment failure or grid outages. Higher tiers obviously cost more to build but attract better tenants and command higher rents.

The cost to build

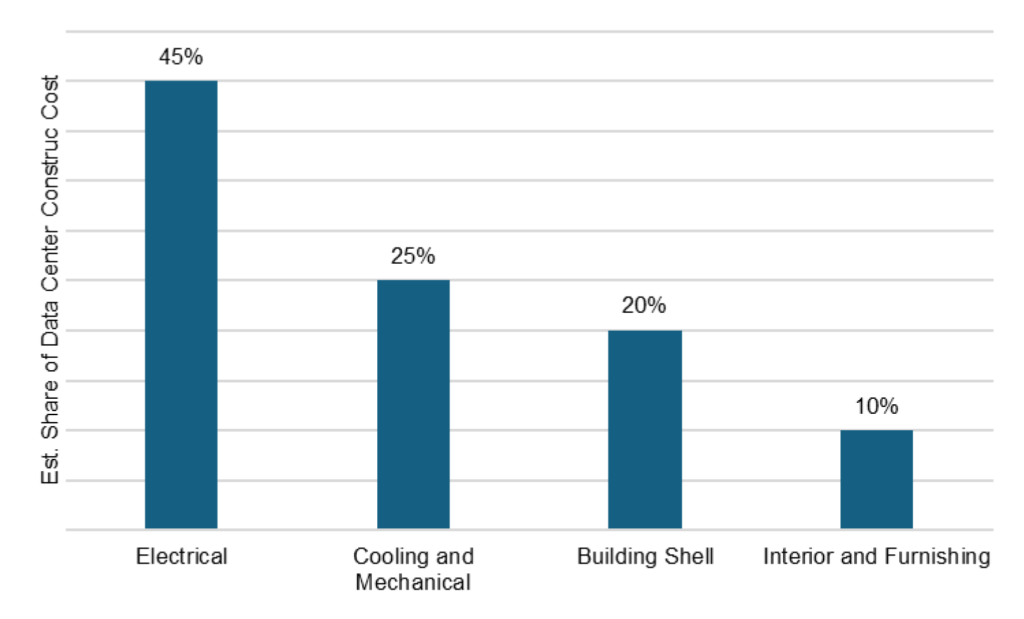

Building and outfitting data centers to current standards takes significant capital. Green Street estimates that building and outfitting a new 200 megawatt (mW) facility runs around $8.2 billion:

- The building costs $2.1 billion or slightly more than 25% of the total. Current cost for a square foot runs around $1,500, with an industry rule of thumb assuming around 7,000 square feet for every megawatt of capacity and a new facility producing 200 mW of power. However, the rising power density of data centers is making the rule less useful. Alternatively, data centers cost $11 million for every mW. Most of the money goes into electrical systems, cooling, the building shell and interior space and furnishings (Exhibit 4).

Exhibit 4: Allocation of cost for building a current data center

Note: Electrical includes uninterruptible power, generators, power distribution units, batteries. Cooling and mechanical include water storage, HVAC, air conditioning, piping. Building shell includes exterior. Interior and furnishing include lobby, shipping and receiving, furniture and others.

Source: Green Street.

- Computing infrastructure and electrical connection to the grid costs $6 billion or closer to 75% of the total. The GPU servers, networking equipment, data storage, racks and other elements for a 200 mW facility adds an estimated $5.6 billion. And the substations, transmission upgrades and electrical grid connections add another $400 million, although that cost could rise if data centers need to build their own power sources.

Data center supply consequently is rising to meet expected demand. Data Center Map counts 4,213 data centers in the US today with around 3,000 operational and the balance under development. Data centers also have started becoming bigger, with some AI-optimized facilities between 500 mW to 2 gW. Some newer facilities can scale up to as much as 5 gW, such as Meta’s Richland Parish, LA, campus.

Own or lease

At this point, the decision to own data centers or lease space is mainly a matter of the user’s available cash flow and the need to get computing capacity quickly. Owning a data center is a choice only open for now to a hyperscaler. An owner may be able to customize a data center to its own particular needs, but lately that comes in a distant second priority to getting capacity as quickly as possible. Most marginal capacity comes through leasing, which has the additional benefit of preserving cash for other immediate or future projects. It also puts some of the supply and demand and obsolescence risk onto the providers of the leased space.

Leased data centers come broadly in two categories:

- Hyperscale data centers, leased to one or several hyperscalers and other large tenants

- Wholesale data centers, leased to companies that need 500 kW or more of capacity

- Retail colocation data centers, leased to hundreds of smaller tenants

Although each tenant negotiates terms to their lease, most have common features:

- Initial lease term. Typical leases run from three to five years for co-location centers and 10 to 15 years for hyperscale centers

- Extension options. Leases often come with options to renew for additional years at the discretion of the tenant

- Make whole provisions. Leases usually come with provisions that compensate the landlord for the value of remaining lease payments if the tenant leaves.

- Costs covered by tenants. Hyperscale facilities often require tenants to reimburse taxes, insurance, power and maintenance, wholesale tenants only to cover power expenses, while co-location centers often partially pass through these costs.

- Conditions allowing the tenant out. Service-level agreements (SLAs) detail when the client can break the lease without penalty. Tenants can get credits for outages or even walk away if there is significant business interruption. A common provision, the five nines, allows a tenant out if center uptime falls below 99.999%.

- Residual value guarantees. RVGs have become critical tools for allowing borrowers with a speculative grade rating or none at all to borrow by relying on a RVG from an investment grade tenant. The tenant providing a RVG is required to make a capped cash payment to the owner based on the asset’s current valuation if they choose to walk away.

- Others. These may include take-or-pay power commitments, where the tenant pays for power whether used or not, sub-leasing rights, rent escalations and others.

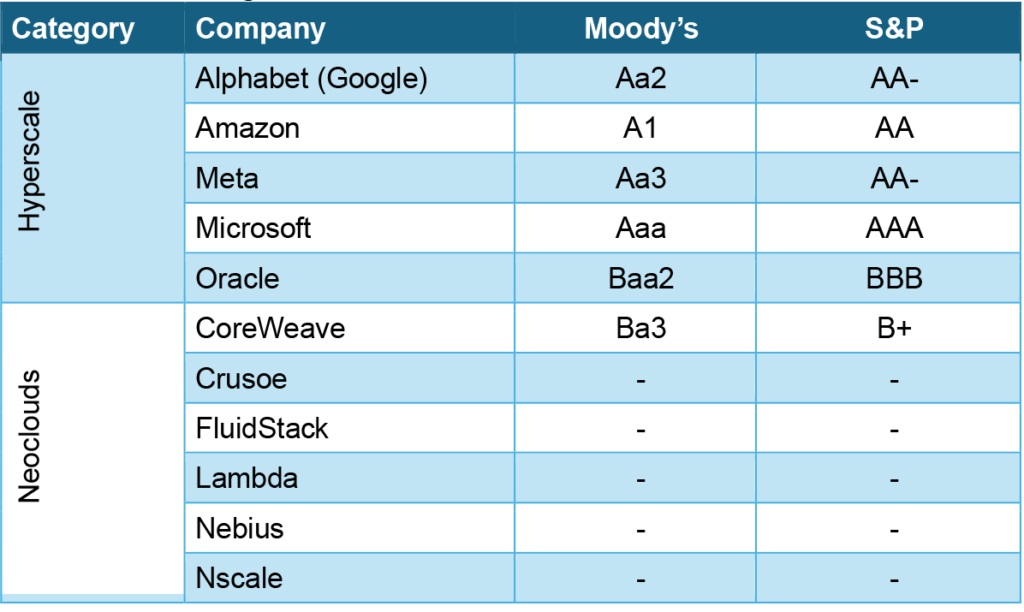

The lease terms and the quality of tenants can have a big impact on the data center builder’s or owner’s access to and cost of debt. Hyperscalers come with investment grade ratings that improve access to debt at lower cost while neoclouds currently have speculative grade ratings or no rating at all (Exhibit 5). Facilities where a hyperscaler is the only tenant often can ride along on the tenant’s rating. Co-location facilities, where hundreds of tenants can lease capacity, require more careful analysis of lease terms and degree of diversification across tenants and their various businesses.

Exhibit 5: Ratings of common data center tenants

Source: Van Nieuwerburgh, Data Centers: Financing the AI Buildout, Marcus Academy presentation, March 19, 2026.

Funding the big build

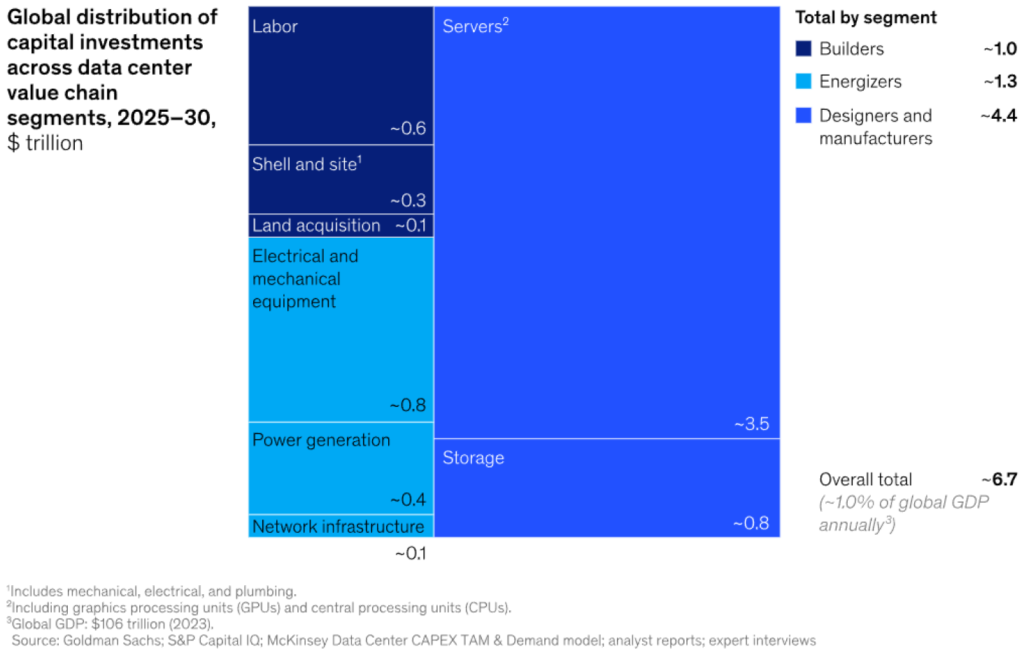

The estimated cost to fund data centers depends on the source. Moody’s estimates that investment in data centers could top $2 trillion in the next four years. McKinsey takes a broader view of data center infrastructure and puts the price tag at $6.7 trillion globally—with 40% in the US—including land, building, equipment, servers, storage and labor (Exhibit 6). Either case should draw on a substantial amount of debt funding

Exhibit 6: McKinsey estimates $6.7 trillion in data center buildout through 2030

Source: McKinsey & Co.

Funding out of cash flow

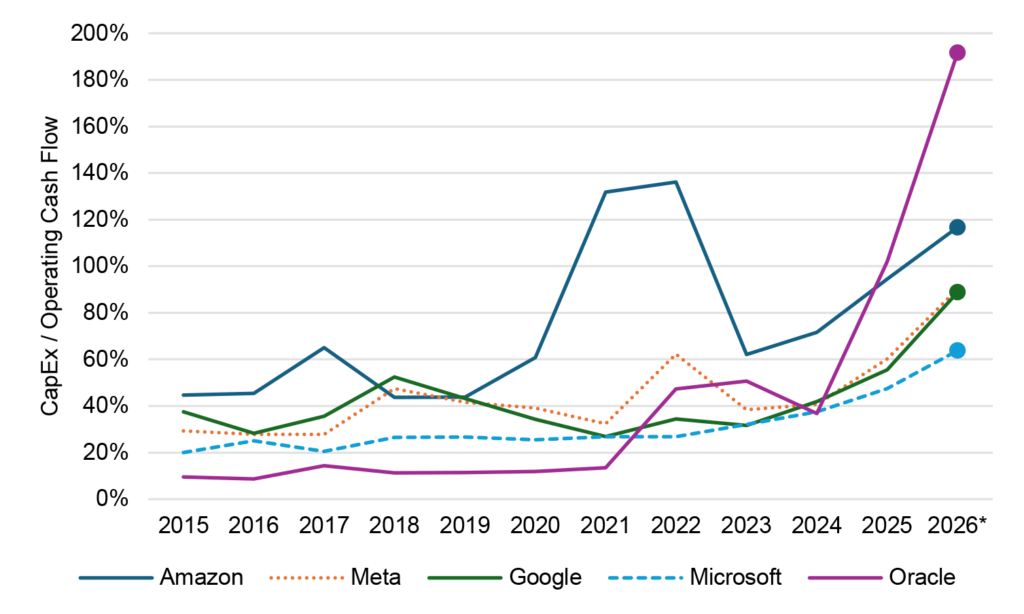

Much of the buildout of data centers and related infrastructure for hyperscalers has come so far out of operating cash flow, but that source of funding is approaching practical limits. Most hyperscalers in 2020 devoted less than 40% of operating cash flow to capital expenses, but since 2023 the share has been rising (Exhibit 7). If equity analyst expectations for 2026 play out, the share should range between 60% and 190%. The race for computing capacity has steadily pushed hyperscalers away from operating cash and into the debt markets. Nevertheless, the equity of hyperscalers carries a significant component of data center exposure. Operating cash flow is probably best suited to take the risk of data center construction.

Exhibit 7: Capex is taking up a rising share of hyperscalers’ operating cash flow

Note: Ratio at the end of each fiscal year. Microsoft and Oracle operate on fiscal years ending June 30 and May 31 respectively, while all others’ end December 31. Estimates for 2026 based on Bloomberg equity analyst consensus. Amazon not available.

Source: Bloomberg, Santander US Capital Markets.

Funding out of investment grade debt

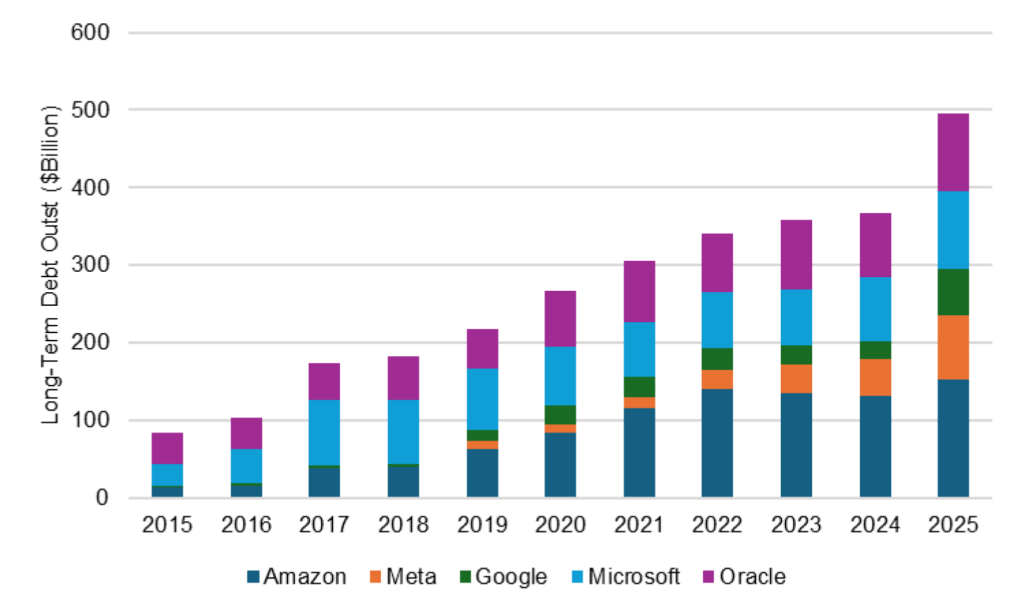

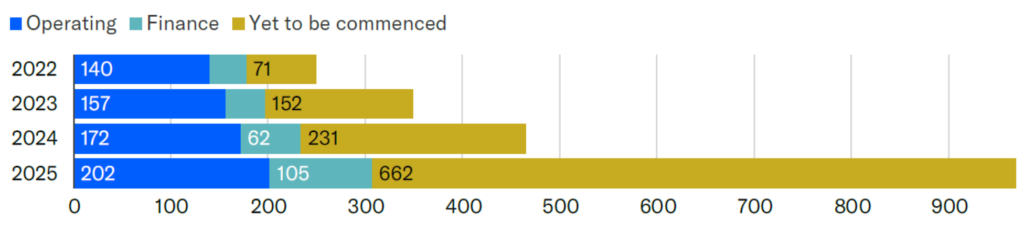

Demand on operating cash flow has tracked with a steady rise in long-term debt from hyperscalers. In 2025, outstanding long-term debt jumped $128 billion or 35% (Exhibit 8). This year, long-term debt should grow aggressively again with announced capital investments of $656 billion or 94% of projected consensus operating cash flow. Debt this year should rise by several hundred billion. Issuing corporate debt takes advantage of the hyperscalers’ generally strong balance sheet and good rating. For investors, exposure to data centers through the debt of hyperscalers is diversified by the other assets on the balance sheet. Operating cash flow and senior unsecured debt is also well suited to take the risk of data center construction.

Exhibit 8: A rising balance of investment grade debt from hyperscalers

Note: Debt outstanding at the end of each fiscal year. Microsoft and Oracle operate on fiscal years ending June 30 and May 31 respectively, while all others end December 31.

Source: Bloomberg, company financial statements.

Investment grade debt also has started coming from issuers relying on a lease to a highly rated hyperscaler or a guarantee of the lease from a hyperscaler. This gets the debt to investment grade even though the issuer may be speculative grade or unrated. The unrated neocloud FluidStack recently used a guarantee to get a $3.25 billion senior secured note to market with a ‘BBB-/BBB-‘ rating. The 16.5-year note came from Hut 8 DC LLC, a bitcoin miner expanding into digital infrastructure, to build a 245 mW data center in St. Francisville, LA. FluidStack signed a 15-year triple net lease with three 5-year renewal options with Alphabet providing the financial backstop guarantee on the lease obligations. The guarantee is subordinated to Alphabet’s debt and other obligations.

Investors should consider the impact of lease renewal periods and guarantees on the balance sheet of the guarantors. As Moody’s points out in a February 26 note, a renewal does not show up on a guarantor’s balance sheet unless it is “reasonably certain” to renew. Guarantors typically claim they are not reasonably certain. Residual value guarantees also only get recorded on balance sheet if there is a “probable future outflow,” which guarantors typically would contest. However, it is highly likely that guarantors either pay rents and renew leases or pay out residual value guarantees. If rating agencies eventually add these guarantees to the debt of the guarantors, balance sheets could become more leveraged and ratings weaker. From 2024 to 2025, outstanding guarantees from Amazon, Meta, Alphabet, Microsoft and Oracle jumped from $465 billion to $969 billion (Exhibit 9).

Exhibit 9: Hyperscaler guarantees surged in 2025

Note: Amount in billions USD as of 12/31/2025 for Amazon, Meta, Alphabet, Microsoft, Oracle.

Source: Moody’s Ratings

Funding out of high yield debt and leveraged loans

While they are inherently more cyclical and risk-sensitive than investment grade markets, leveraged finance markets are attractive because they can be used to finance individual projects and growth initiatives not initiated or guaranteed by the hyperscalers. High yield bonds and term loans can also be structured to align with cash flow life of the data center itself. This allows issuers to put more leverage on contractual revenues often with a bullet structure in the case of public high yield debt. These markets also offer an attractive alternative to equity financing as they enable the sponsor to raise capital without issuing new equity or diluting ownership by bringing in new partners or joint owners.

In April, CoreWeave (CRWV: B1/B/BB-) priced a $2.75 billion high yield 5-year note offering at a 9.75% yield. This followed two US dollar note offerings in 2025 totaling an additional $3.75 billion. Meanwhile, the issuer secured $8.5 billion in additional financing through a term loan facility to expand its AI cloud platform last month.

Funding out of private debt

Some data centers under construction have started using project finance structures, which are well suited to handle construction risk. Hyperscalers’ rationales for leasing data centers and entering into joint ventures often center on strategic flexibility and optionality while managing the capital requirements of their AI initiatives. Critical to the issuer is effectively keeping the data center off balance sheet as a long-term liability.

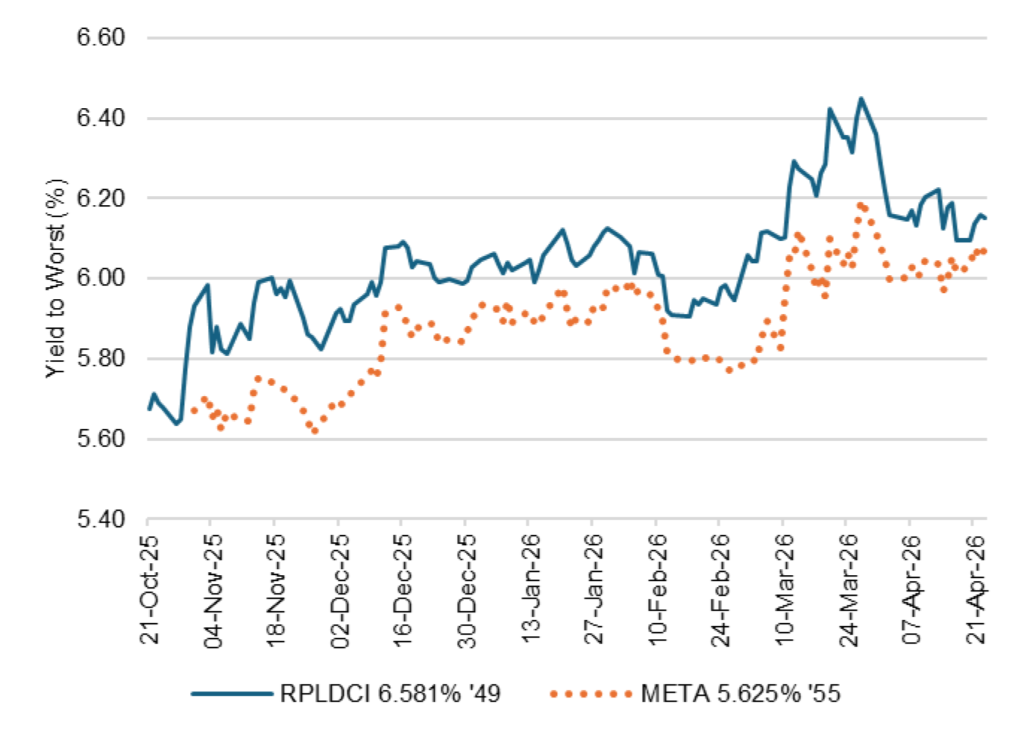

The market was presented a case study for these types of financing structures in late 2025 with Meta’s joint venture to fund its Hyperion AI Campus in Richland Parish, LA, known as the Beignet Investor LLC transaction. Meta partnered with Blue Owl Capital to issue $27.3 billion in private debt in October of last year. Meta holds just 20% ownership interest in the structure. Blue Owl owns 80% interest in the special purpose vehicle after putting up $2.5 billion in equity. The operating lease classification helps Meta by keeping it off the books as long-term debt to the company. Additionally, Meta was able to negotiate terms that it viewed as beneficial, including an initial 4-year lease term, options to renew at 4-year increments, and a residual value guarantee.

PIMCO purchased $18 billion of the structure with Blackrock taking a $3 billion position as well. With a single agency rating of ‘A+’ from S&P and a maturity of 2049, the deal was marketed with a yield of just under 6.6%. That compares with a 30-year senior unsecured note issued directly out of Meta (META: Aa3/AA-/AA-) shortly thereafter at a yield of 5.625%. The Beignet notes quickly shot up to a peak dollar-price of about $110 or a yield of right around 5.6% in the immediate days following the transaction. It has since settled into a longer-term range between $104 to $106 and is currently yielding about 6.15% compared to 6.05% for the Meta-issued long bond.

Exhibit 10: Beignet Investor LLC notes trade only slightly wide to Meta notes

Source: Santander US Capital Markets LLC, Bloomberg/TRACE BVAL pricing

More recently, Nscale was able to get $1.4 billion in financing from PIMCO and Blue Owl Capital to fund chip purchases from Nvidia. The transaction was set up as a delayed-draw term loan. This represents a considerably different and smaller scale transaction than Beignet Investor LLC. But it highlights the flexibility afforded by private credit markets, as well as the burgeoning demand from investors.

Funding out of ABS

ABS structures have worked for fully built and leased data centers with established cash flows. From 2018 through early 2025, according to KBRA, ABS issued more than $34 billion in debt across 75 transactions backed by large data center assets.

The ABS sponsor transfers a portfolio of data centers as well as the rights to their customer contracts into a bankruptcy-remote trust that issues a few tranches of debt rated between ‘A’ and ‘BB’. The deals are structured as master trusts, which allow upsizing, issuing follow-on debt, adding collateral—important for centers rolling over contracts or operators funding new centers coming online. Master trusts also allow variable funding notes, which act like revolving lines of credit inside the trust and can expand, contract or convert into term paper. Data center revenues pay the debt interest and principal directly. The equity interest in the data centers, which serves as the risk-retention class, is also pledged as collateral. The debt is secured by the trust’s assets and governed by an indenture.

The inclusion of equity shortcuts the need to go through foreclosure if the data center cash flows fall short. This avoids the risk of rapid erosion in cash flow and data center value. Of course, the trust also takes on the risks of ownership, which include environmental lawsuits or other legal action.

The data center collateral backing ABS can vary from a few facilities mainly with investment grade tenants to dozens of data centers with thousands of mainly unrated tenants in the case of co-location centers. Facilities dominated by large investment grade tenants generally show longer contracts with less support from the facility operator. Co-location centers generally show shorter contracts mainly with unrated tenants and reply on the operator to re-lease capacity as contracts end. Co-location centers also commonly offer other tenant services such as installation, security, meeting rooms, cloud services and network connections, requiring more operator involvement and expertise.

The master trust directly controls cash flows from data center operations and distributes them according to deal priorities:

- Operating expenses

- Administrative and servicing fees

- Interest due on ABS notes

- Any required deposits in reserve accounts such as taxes or insurance

- Sequential repayment of principal after an anticipated repayment date

- Any remaining cash to equity or the sponsor

ABS deals also usually include performance triggers defined at the trust level rather than the loan level that can divert cash from equity into a reserve fund or to pay down senior debt. Triggers can include failure to repay by an ARD or a decline in debt service coverage ratio or loan-to-value.

Even though ABS does not allow recourse to the sponsor, many master trusts act as the sponsor’s major source of funds. The trust holds a single pool of collateral backing all ABS debt, so the sponsor would selectively default on certain data centers or classes of debt issued by the trust at significant cost. That would trigger forfeiting all performing assets.

Funding out of CMBS

CMBS structures also have worked for fully built and leased data centers with established cash flows but particularly ones dominated by investment grade tenants. From 2018 through early 2025, according to KBRA, CMBS had issued more than $14 billion in debt across 13 transactions backed by large data center assets.

The CMBS sponsor transfers a first lien mortgage on one or more data center properties to a REMIC trust, which then issues bonds to investors. The mortgage is secured by the data center land, building and fixtures and assignments of leases or rental income from tenants. Cash flows from the mortgage repay bond interest and principal. The REMIC allows significant tranching, so CMBS deals typically issue six to eight classes rated from ‘AAA’ to deep speculative grade along with a risk-retention class. The tranching helps a CMBS deal reach a broader pool of investors. In cases where a data center could fund through ABS or CMBS, REMIC tranching can lower the cost of debt.

The term of debt issued by the CMBS trust depends on the maturity of the underlying mortgages. Fixed-rate commercial mortgages often have 5- to 10-year maturities with significant prepayment penalties. CMBS notes can have a final maturity 12 to 15 years after final loan maturity, making loan refinancing a significant risk to repaying the note. Floating-rate commercial mortgages can have 2- to 3-year maturities with several 1-year extension options.

CMBS data center transactions typically involve a few large centers with a limited set of tenants. The larger tenants are almost all investment grade. They typically have signed 5- to 10-year leases with several extension options. This focuses risk on the credit quality of the tenants and the likelihood of lease renewal.

Control of cash with a CMBS deal stays in the hands of the borrowers. Tenants pay rent to the data center owner, who pays operating expenses along with principal and interest on the mortgage and keeps excess cash flow.

CMBS deals also include performance triggers, but at the level of the mortgage loan rather than the CMBS deal. If a loan defaults, it triggers a cash trap where rents go into a lockbox rather than to the property owner and then to the CMBS trust.

CMBS deals also do not offer recourse to the sponsor, and default on one has no effect on others. Borrowers consequently have more room to walk away from troubled properties than they might under an ABS trust.

Current risk, spread and relative value

The bullish likelihood that data centers keep generating cash flow and holding their value look strong for now. Signs that demand for computing power keeps outstripping supply shows up in the rising prices for land, buildings, power and cooling, CPUs and GPUs and even for the tools and materials needed to manufacture the technology. If demand for computing power plays out as projected and these conditions persist, most debt with data center exposure should perform well. The incentive is for investors to add risk, yield and carry as long as debt maturities fall within the bullish horizon.

But there are clear risks:

- Execution risk. For debt secured by data centers under construction, bottlenecks in access to power or cooling or CPUs and GPUs or local political opposition could extend development timelines, drive up costs and lower valuations.

- Obsolescence. For any debt or equity with data center exposure, technological obsolescence could reduce collateral value and the prospects of rolling over leases. The risk could come from more efficient algorithms for training AI, CPUs or GPUs that need less power, advances in cooling systems or other directions.

- Supply and demand. For debt secured by centers in development or fully built with cash flow, a temporary or permanent break in AI development could leave the industry with excess computing power, driving down lease rates as tenants renew and lowering the value of data centers. The prospect of a winner-takes-all outcome in the AI race also poses risk unless the winner needs the computing power previously used by the also-rans.

- Guarantor risk. For data center debt secured by hyperscaler credit or by their leases, the significant capital commitment from the hyperscalers along with the debt required to finance it could bias their ratings lower—or raise market concerns in advance of any rating actions—and widen spreads on related debt or leases. The market may also take a hard look at hyperscalers’ residual value guarantees on leases and begin to consider them in calculations of balance sheet leverage, another factor that could widen spreads on both hyperscaler debt and on deals relying on their guarantees.

- Counterparty or customer risk and complexity. The risk that counterparties or customers fail to perform on leases or that the operator struggles to replace expiring leases is a deal-by-deal analysis.

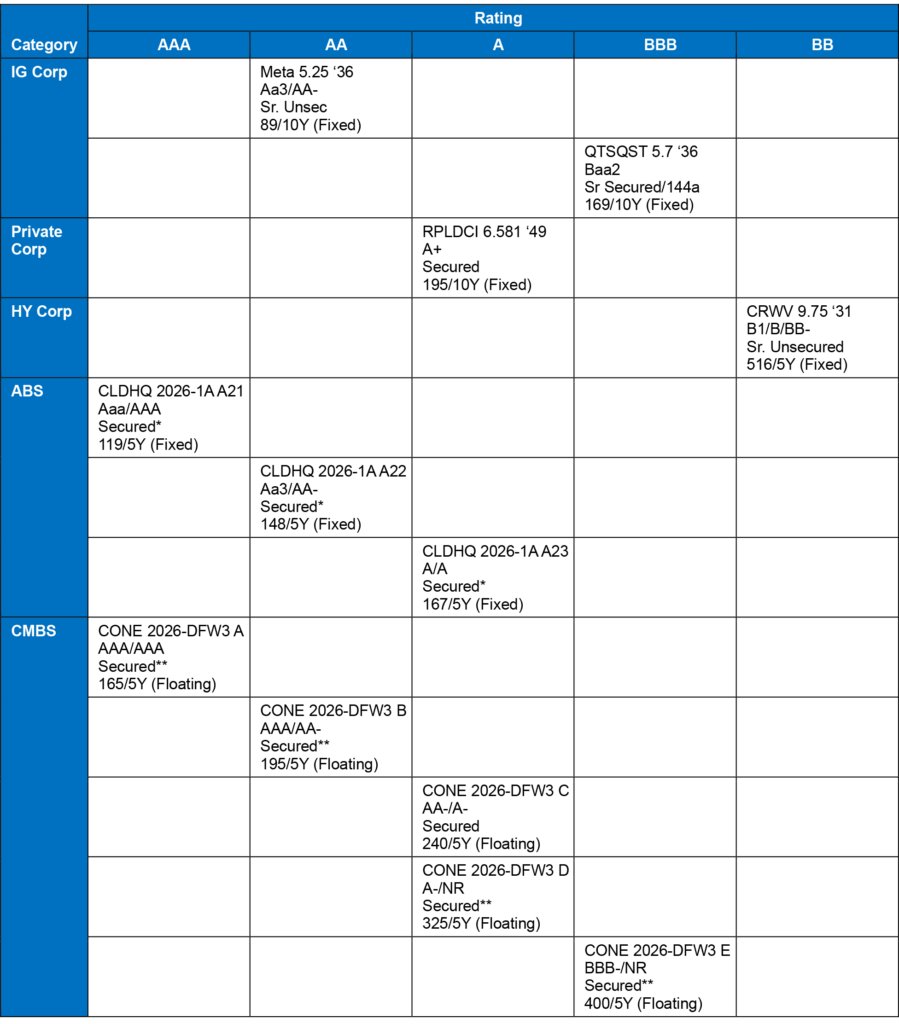

Relative value depends on where the bullish horizon ends and where more bearish possibilities start to rise. For example, the recent CLDHQ 2026-1A A22 ABS, secured by a data center with Meta and Microsoft as anchor tenants, trades at a spread of 148 bp over the 5-year Treasury. By comparison, the Meta 5.25% issue maturing in 2036 currently trades at a spread of 89 bp over the 10-year Treasury. The rating for each instrument is ‘Aa3/AA-‘, although the sources of credit enhancement are different—the broad Meta balance sheet backing the corporate debt, and the tenant leases and structural enhancement supporting the ABS. The market clearly penalizes the ABS for its structural complexity. The ABS looks like better value for a bullish horizon, but the Meta debt looks better over a longer horizon.

The same issue comes into play in considering CLDHQ 2026-1A A22 ABS at a spread of 148 bp to the 5-year Treasury to the CONE 2026-DFW3 CMBS at a spread of 195 bp to the 5-year. Both are ‘AA-‘ although the ABS is a fixed coupon and the CMBS is floating. The tighter spread on the ABS likely reflects the protection offered by an ABS master trust rather than a CMBS REMIC trust—the former cross-collateralized by all deals financed by the trust sponsor, the later only by the first lien mortgage on the deal property. The CMBS may be better in the short run, the ABS in the long run.

For speculative grade exposures, the market again penalizes CMBS more than similarly rated corporate exposures. The ‘Baa2’ corporate QTSQST 5.70% of 2036, for example, has traded recently at a spread of 169 bp over the 10-year Treasury. But the CONE 2026-DFW3 ‘BBB-‘ CMBS issue has traded at 400 bp over SOFR with a 5-year weighted average life. For investors able to take the higher complexity of the CMBS, the market compensates well.

Exhibit 11: Recent yield spreads on data center and related exposures

Note: All markets levels as of 5 May 2026. *CLDHQ 2026-1A secured by data center leases to Meta and Microsoft for facilities in Ashburn, VA.**CONE 2026-DFW3 secured by a single-asset single-borrower data center in Allen, TX, 99.8% leased to 35 unique tenants.

Source: Santander US Capital Markets.

The risks around data centers and the buildout of AI will almost certainly continue evolving over the next few years, as will the relative impact across the different sectors of the US debt markets where the effort gets funding. The framework of identifying the core risks, assessing their impact across sectors and looking for proper compensation should continue giving issuers guidance on where to source funds and investors guidance on where to find relative value.