The Big Idea

Looking for labor market slack

This material is a Marketing Communication and does not constitute Independent Investment Research.

Economists are constantly trying to gauge slack in the labor market. When the unemployment rate reached 4.6% in November and appeared to be on a clear uptrend, Fed policymakers responded with rate cuts at three straight meetings. The subsequent decline in the unemployment rate in December and January has brought it back to 4.3%, close to FOMC estimates of the long-run full-employment level. With no clear sign of slack from joblessness, economists can turn to other margins of labor market behavior such as the U-6 underemployment rate and labor force participation. Both suggest the labor market is close to full employment.

Margins of labor market slack

The most obvious way to gauge weakness in labor market conditions is the level of the unemployment rate. Economists can debate what reading of joblessness is consistent with full employment, but there is fairly broad agreement. For example, the median projection of 19 FOMC participants puts the long-run equilibrium level of the unemployment rate is 4.2%, and the central tendency, which drops the three highest and lowest individual submissions, is a relatively narrow range of 4.0% to 4.3%.

In the first half of 2025, the unemployment rate was squarely in that range, but it backed up noticeably late last year. Fed officials became quite worried about downside risks to the labor market when the jobless rate rose to a high of 4.6% in November, although that reading has since been revised to 4.5%. Through December and in January, the rate fell to 4.3%.

However, there may be slack in the labor market beyond unemployment. One measure that gained prominence in the 2010s was involuntary part-time employment. Then Fed Chair Yellen highlighted the broader U-6 underemployment rate, which also includes those in the household survey who say that they are only working part-time but want to have full-time employment. Back in the mid-2010s, an elevated pool of people who were unable to attain full-time hours pointed to some lingering slack in the labor market even as the unemployment rate fell to around the FOMC’s estimate of full employment.

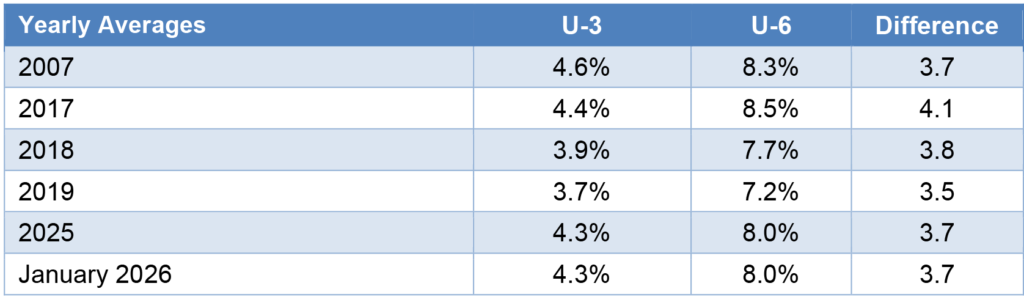

In the current situation, the U-6 underemployment rate fell sharply in January to 8.0%. That puts the gap between the traditional (U-3) unemployment rate and the U-6 gauge roughly in line with previous instances when the jobless rate was at roughly the current level (Exhibit 1). The current gap of 3.7 percentage points is about where it was in 2007 and in 2018 and 2019. By contrast, the gap in 2015 was over 5 percentage points. This suggests that the level of involuntary part-time workers is about where we would expect and thus does not point to an alternative source of excess slack.

Exhibit 1: U-3 vs. U-6 Unemployment

Source: BLS.

The other main potential source of slack is labor force participation. People are only designated as unemployed in the household survey if they are out of work and actively seeking a job during the month. If respondents want to work but fail to pursue a job over the course of the month, perhaps because they do not believe there are any good opportunities—so-called “discouraged workers”—they show up in the household survey as out of the labor force and thus not unemployed.

If the labor force participation rate (LFPR) is lower than would normally be associated with a given unemployment rate, it might point to slack in the labor market.

Assessing labor force participation is not as straightforward as simply examining the overall LFPR. The U.S. population is aging, which means that a rising proportion of the “working-age population”—defined by the BLS as 16 and up, meaning no upper limit—is over 65, the traditional retirement age. As a result, the overall LFPR is trending lower over time.

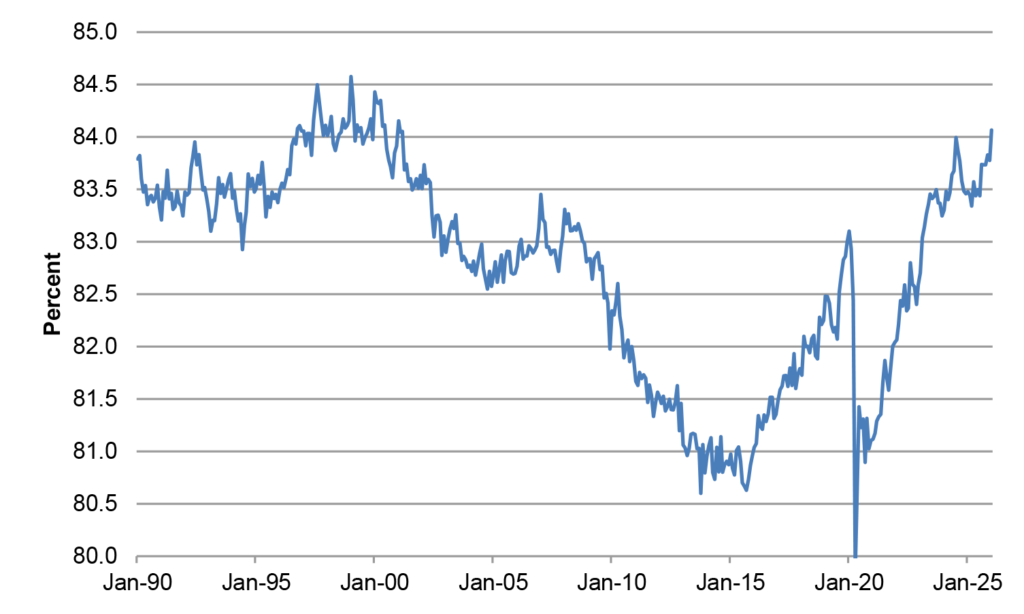

The most straightforward way to adjust for shifting demographics is to focus on the prime-age LFPR, covering ages 25 to 54 (Exhibit 2). The prime-age LFPR has been trending higher since the pandemic, even as the pace of job gains has cooled. In January 2026, the gauge exceeded 84% for the first time since 2001.

Exhibit 2: Prime-age labor force participation rate

Source: BLS.

The lofty level of the prime-age LFPR clearly indicates that there is not an outsized reservoir of idle workers who are waiting for improved job prospects to jump back into the labor force. Instead, this measure also points to a labor market that is at worst near full employment and perhaps even marginally tight.

Signs of stabilization

The improvement in labor market data over the past few months extends beyond just the decline in the unemployment rate in December and January. Two other key measures of the health of the labor market from the household survey also confirm that the economy is near or at full employment. The improved tone of the data helps to explain the notable swing in Fed rhetoric, from emphasizing downside risks to the labor market and cutting rates in late 2025 to being firmly on hold and citing “signs of stabilization” in labor market conditions in early 2026.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.