The Big Idea

A marginal firming in demand for workers

This material is a Marketing Communication and does not constitute Independent Investment Research.

Within the Fed, it has become a mantra that “the labor market is stabilizing.” The hard data suggest that the employment situation may actually be improving somewhat. My favorite proxy for the hiring side of the labor market equation, the Indeed Job Postings Index, is consistent with a marginal firming in the demand for workers in early 2026 and offers corroboration for the small swings in recent months portrayed in anecdotal data.

Mapping out the story from business sources

There is a rich array of qualitative information on the economy that can establish a narrative for the broad performance of activity and the labor market. There is ample anecdotal evidence from business comments, including the assessments relayed by Federal Reserve Bank presidents from their regular conversations with their networks of business contacts. We also have numerous business surveys, highlighted by the monthly ISM polls.

In very broad terms, this stream of information can be used to flesh out a running narrative for the labor market. Many firms took a step back last year, delaying major decisions on both hiring and layoffs. The primary impetus for this cautiousness was said to be policy-related uncertainty, deriving most notably from the administration’s unpredictable moves on the tariff front, which led many companies to delay decisions related to both investment and hiring.

Commentators have been discussing the reduction in churn in the labor market over the past year. Many call the current situation the “no hire, no fire” labor environment. This description is accurate, as both gross hiring and layoffs were historically weak for much of 2025 and into this year. This is a highly unusual alignment. The only explanation that in my mind offers a satisfactory rationale for this unusual situation is the fact that business cautiousness ratcheted up, so that executives were hesitant to make big moves on headcount, whether positive or negative.

By late last year, at least some of the firms that had moved to the sidelines were beginning to tiptoe back into the water, as the endgame on tariffs started to become a little clearer. Heading into early 2026, the tone of business sentiment picked up significantly, and labor market data similarly improved.

Then, unfortunately, at the beginning of March, the US-Iran conflict began, and the uncertainty associated with the fluid situation in the Middle East sent many businesses scurrying back to the sidelines again.

Hard data

The hard statistical data arguably paints a brighter picture than the Fed consensus of mere stabilization. Most notably, private sector payroll increases averaged 25,000 last year but accelerated to an 86,000 per month pace in the first four months of this year. Similarly, initial unemployment claims averaged 225,000 a week last year but slipped to a 211,000 weekly pace so far in 2026. Finally, the unemployment rate peaked at 4.5% in November and inched down to 4.3% in January, March, and April. So, I would argue that the Fed characterization might be a little conservative. It may be more precisely accurate to say that the labor market has firmed slightly early this year. Having said that, I do not rule out the prospect that the ongoing uncertainty in the Middle East, especially if it lingers or, worse yet, ratchets up further, could reverse some of those modest gains.

Indeed Job Postings Index

As I have discussed numerous times, the Indeed Job Postings Index is my favorite proxy for the hiring side of the labor market equation (I favor initial jobless claims on the layoff side of the ledger). Job search firm Indeed aggregates the postings on its site, creating an aggregate index of labor demand. The concept is quite similar to the JOLTS job openings series, but it does not feature the outsized high-frequency volatility that makes the JOLTS figures unreliable.

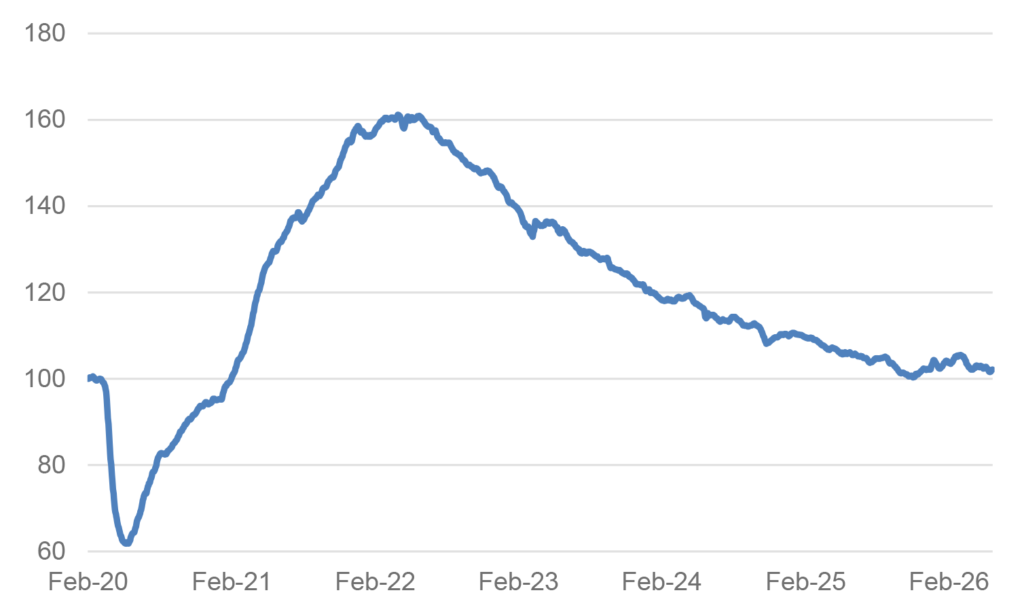

In any case, the Indeed index was set at 100 on February 1, 2020, providing a pre-Covid benchmark against which to compare as the economy reopened in 2021 and beyond. In broad strokes, the gauge peaked in early 2022, at the height of the post-pandemic labor shortage and gradually moderated for almost four years, finally leveling out late last year at roughly the pre-Covid level of labor demand (Exhibit 1).

Exhibit 1: Indeed Job Postings Index

Source: Indeed.

From this perspective, the Fed’s “stabilization” description looks about right. And I would not characterize the “stabilization” story as grossly wrong. However, if we zero in and take a closer look, there may be more nuance to the story.

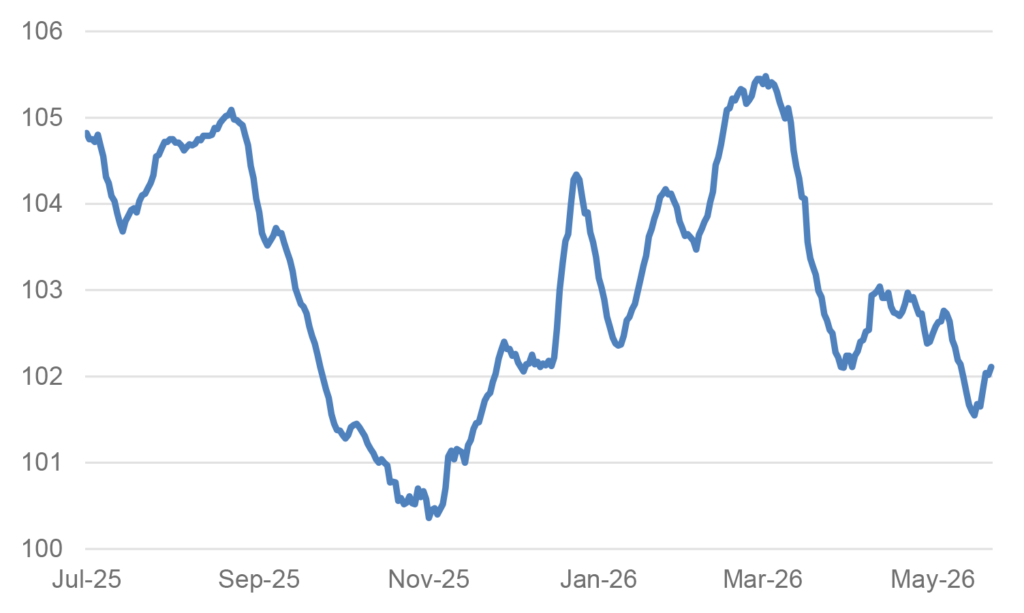

Focusing on the last year or so, we can see the limited swings in the gauge more clearly (Exhibit 2). Labor demand eroded significantly in September and October but bottomed out around the beginning of November and managed a solid rebound from November through February. This likely corresponds to the tentative re-engagement by businesses described above, as tariff-related uncertainty began to recede. Then, the beginning of the conflict in Iran probably led to a noticeable pullback in the demand for workers in March. Since the beginning of April, the Indeed index has been on balance little changed, with small moves in both directions over the last two months.

Exhibit 2: Indeed Job Postings Index

Source: Indeed.

In my view, this more detailed account of labor market developments is far more complete and accurate than the “labor market is stabilizing” characterization that comes from a 30,000 foot view.

Conclusion

For me, the most interesting aspect of the current labor market situation is that the erosion in demand seen in the Indeed index since the beginning of the Middle East conflict, corroborated by anecdotal commentary, has not yet shown up in the aggregate data. Payrolls posted surprisingly robust gains in both March and April, and initial jobless claims have averaged 208,000 a week in April and May, down slightly from the 212,000 average in the first quarter. My early May payroll forecast calls for a 100,000 gain in private payrolls, so I am not fully taking the notion of a marginal slackening in labor market conditions on board, though I would certainly not be shocked or worried if we saw a softer May reading. The encouraging news here is that the Middle East conflict is viewed as likely to be short-lived, and if uncertainty ebbs in a meaningful way in the months ahead, I suspect that there is a substantial reservoir of pent-up demand for workers that may be unleashed, perhaps later this year.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.