The Big Idea

Inflation expectations at a critical level

This material is a Marketing Communication and does not constitute Independent Investment Research.

Inflation is accelerating, and Fed officials, economists, and financial market participants are debating the relative importance of persistent underlying pressures compared to temporary tariff-related price hikes, with the energy price spike introducing another complication. The critical question is whether inflation will quickly revert to the 2% neighborhood once these temporary influences fade or whether the seemingly endless string of supply shocks will change the way that businesses and consumers view price setting, promoting a higher inflation trend. Consumer surveys asking about inflation predictions suggest that we have reached a critical point on longer-term expectations. Further increases from here will be especially problematic for the Fed.

Setting the stage

The textbook treatment of a temporary inflation force, such as a one-off wave of tariff-related price passthrough or an energy price shock, is that the central bank should ignore it and concentrate on the longer-term underlying inflation trend. This strategy worked numerous times in recent decades when inflation surged due to energy price shocks, such as when hurricane Katrina knocked out oil refineries.

However, the strategy backfired on the Fed in the aftermath of the pandemic, when a wave of supply restrictions pushed prices higher. Chair Powell and others at the Fed confidently declared that the ensuing inflation would prove “transitory.” What they missed is that the Fed had injected far too much liquidity into the economy, turning what might have indeed been a temporary adverse supply shock into an economy with grossly excessive demand at the same time that supply was constrained.

We find ourselves at a critical crossroads at the moment with regard to inflation. Having brought inflation back down to between 2.5% and 3.0% on a year-over-year basis by 2024, the Fed was optimistic that it would soon achieve its 2% target. However, progress stalled out at that point. Officials spent most of 2025 blaming too-high inflation on tariff-related passthrough and asking for patience. As we entered 2026, the continuing lack of progress on core inflation had some Fed officials beginning to grow restless.

More recently, layering on top of the ongoing tariff effects, energy prices spiked due to the repercussions of the conflict in the Middle East. Again, the traditional playbook calls for the Fed to look past these temporary effects. However, as a number of more hawkish policymakers have pointed out, that strategy presumes that the special factors will be generally viewed as strictly one-off.

In the current circumstances, when businesses and consumers have faced a seemingly endless series of adverse supply shocks beginning with the pandemic in early 2020, there is a risk that price setters (businesses) and price takers (consumers) will begin to regard supply disruptions as a common feature of the economic landscape and will incorporate them into inflation expectations. At that point, when what would formerly have been thought of as an anomaly becomes par for the course, the Fed (or any central bank) has a problem.

The question currently facing the FOMC is whether we are nearing that point in the US economy.

Consumer survey inflation expectations gauges

There are two consumer surveys that regularly ask households about their longer-term inflation expectations. The University of Michigan consumer sentiment survey has been asking about 1-year-ahead and 5- to 10-year-ahead inflation expectations for several decades. More recently, the New York Fed began publishing 1-year-ahead and 3-year-ahead inflation expectations in the early 2010s. The New York Fed also began reporting 5-year-ahead figures but only in 2022, leaving not enough history to be useful in this context. All of the figures described below represent the median responses of households.

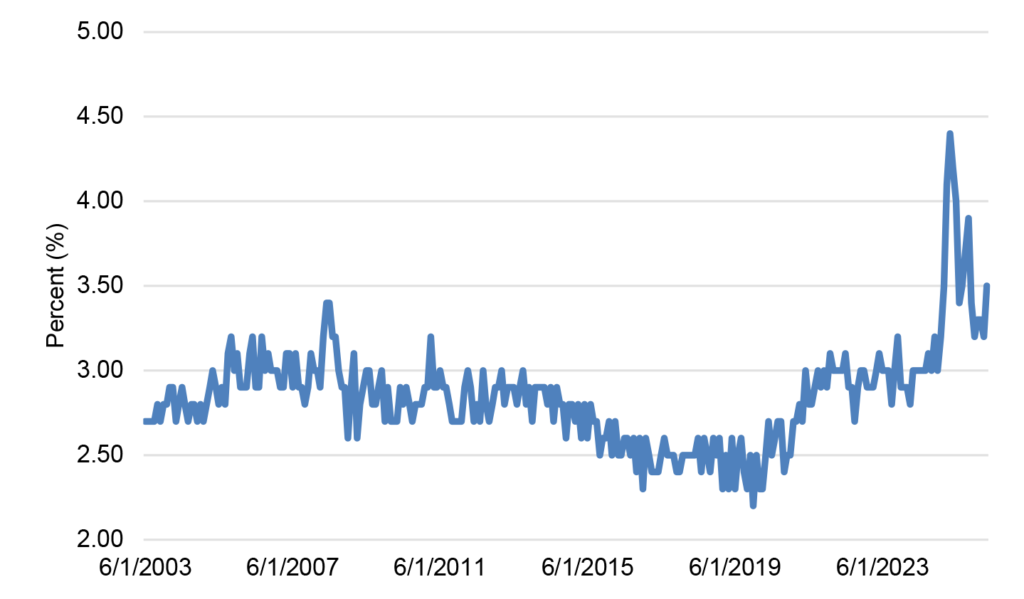

The recent history of the University of Michigan long-term (5- to10-year ahead) inflation expectation series is a bit surprising (Exhibit 1). The pre-pandemic norm was for this series to fluctuate at or below 2.5%. Recall, though, that this was a period when inflation ran on average modestly below the Fed’s 2.0% target. Perhaps the 2.5% to 3.0% range seen for much of the 2000s and early 2010s is a better range for tracking with actual inflation in the 2.0% vicinity. What is interesting is that longer-term inflation expectations never substantially exceeded 3.0% in the post-pandemic period, despite actual inflation peaking at close to 7.0%.

Exhibit 1: University of Michigan longer-term inflation expectations

Source: University of Michigan.

In contrast, in the runup to and aftermath of the Liberation Day tariff announcement last year, longer-term inflation expectations spiked, reaching as high as 4.4% in April before quickly receding to the low 3.0%’s by the end of last year.

Note that, historically, December’s 3.2% reading was probably already too high to be consistent with actual inflation of 2.0%. The April figure, however, jumped from 3.2% in March to 3.5%, the highest level, aside from a handful of readings last year, in 30 years.

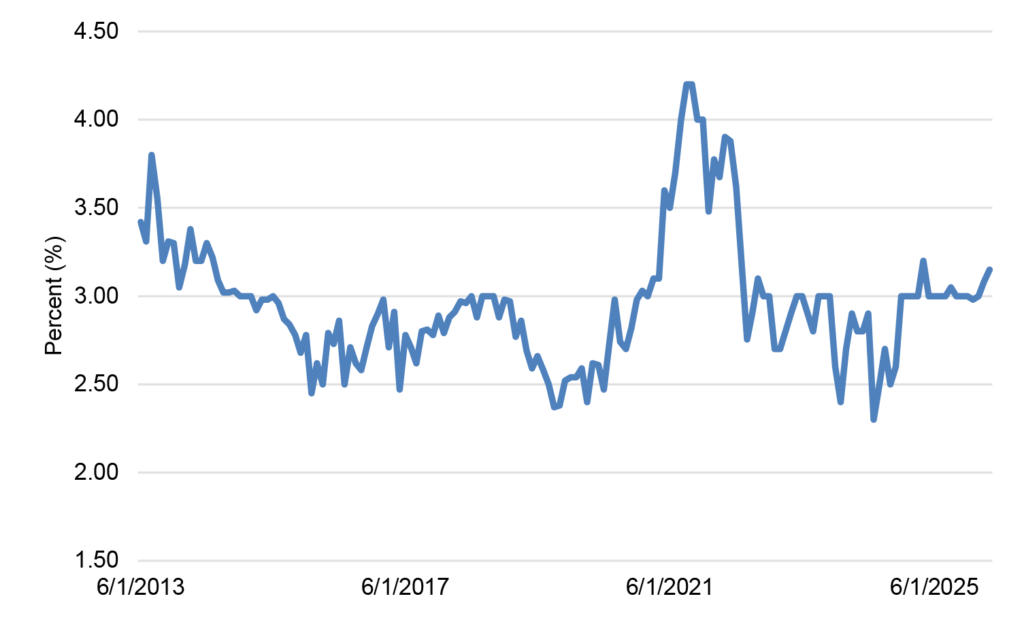

The evolution of the New York Fed’s 3-year-ahead survey during the 2020s is quite different, and more plausible in my view (Exhibit 2). Inflation expectations surged as actual inflation ballooned, peaking in 2021 at over 4.0% compared to a pre-pandemic norm of 2.5% to 3.0%. Fortunately, inflation expectations quickly receded, sliding back to the pre-pandemic prevailing range by 2024. Liberation Day elicited a small and brief uptick in expected inflation, but the series has generally been parked at 3.0% since the beginning of last year.

Exhibit 2: New York Fed 3-Year-Ahead Inflation Expectations

Source: NY Fed.

Unfortunately, the gauge crept higher in March and April, reaching 3.15% last month. This reading is not far from the previous prevailing level of 3.0%, but it is the highest in a decade aside from the single 3.2% figure in April 2025 and the post-COVID surge in 2021 and 2022.

Conclusion

The relatively small uptick in longer-term inflation expectations in the last few months is not out of line with prior episodes when oil prices spiked and, by itself, is not necessarily terribly alarming. However, a further significant ascent from here would take these gauges to rarely seen levels. Such a result would signal a danger that the fears of some policymakers that consumers are recalculating their views of what is normal for inflation in a way that will make it far more difficult for the Fed to achieve its 2.0% inflation target.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.