The Big Idea

More room for lending, investing under proposed new bank regs

Steven Abrahams | April 17, 2026

This material is a Marketing Communication and does not constitute Independent Investment Research.

Banks may eventually get more than $1.25 trillion of new room on their collective balance sheet for lending and investment if US regulators implement a set of proposals introduced last month. The proposals cover a wide range of bank activities but generally reduce the amount of required core capital and the size of risk-weighted assets. They also extend incentives to limit interest rate risk and create new incentives for banks to originate and hold residential mortgage loans.

The March 19 proposals from the Federal Reserve, the Office of the Comptroller of the Currency and the Federal Deposit Insurance Corp. break into several pieces designed to address banks of different sizes. They revise rules largely put in place in the years immediately after the Global Financial Crisis. In some places, the proposals interact directly with debt capital markets. In others, the proposals interact indirectly by giving banks new incentives to securitize or not or by freeing up capital for lending or investment.

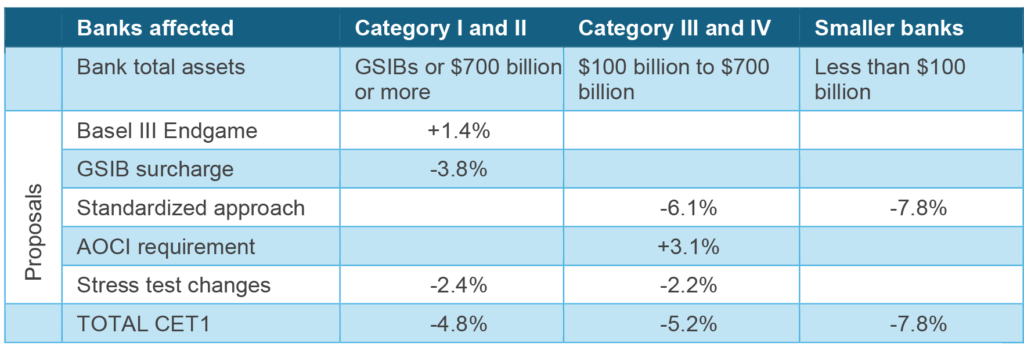

The most important net impact of the proposed rules would be to reduce the required amount of banks’ most expensive capital, Common Equity Tier I or CET1. Some of the new proposals raise CET1 but others, including treatment of capital gains and losses and new stress tests, more than offset those for a net drop of 4.8% for the largest banks, 5.2% for banks with total assets between $100 billion and $700 billion and 7.8% for smaller banks (Exhibit 1).

Exhibit 1: Bank regulators’ proposed rules would reduce required core capital

Source: Federal Reserve https://www.federalreserve.gov/aboutthefed/boardmeetings/files/board-memo-basel-gsib-standardized-approach-20260319.pdf

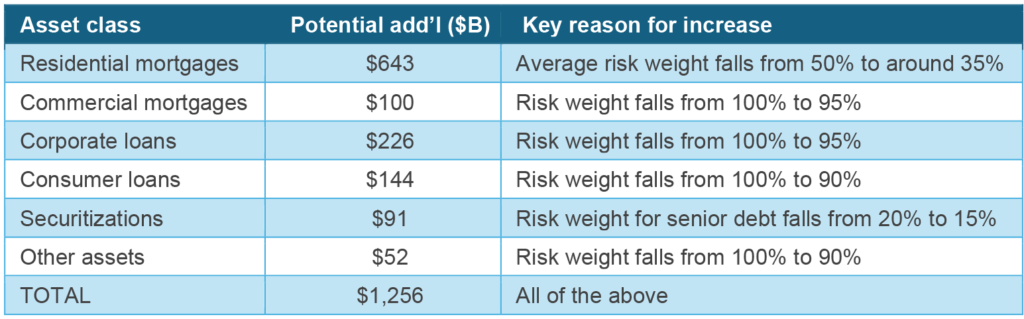

If banks use the newly available core capital to increase loans, securities and other earning assets to the capital-to-asset ratios of mid-2025, regulators’ estimate lending would rise by $1.256 trillion across areas including residential and commercial real estate, corporate and consumer loans, securitizations and other assets (Exhibit 2).

Exhibit 2: Potential for new lending and investment

Source: Federal Reserve https://www.federalregister.gov/documents/2026/03/27/2026-05960/regulatory-capital-rules-regulatory-capital-and-standardized-approach-for-risk-weighted-assets

Although the proposed rules would have different effects across bank asset classes, the broad impact should be to increase the size of bank balance sheets and consequently generate new demand for loans, securities and various forms of funding to finance those assets.

The specifics of some of the main proposals follow.

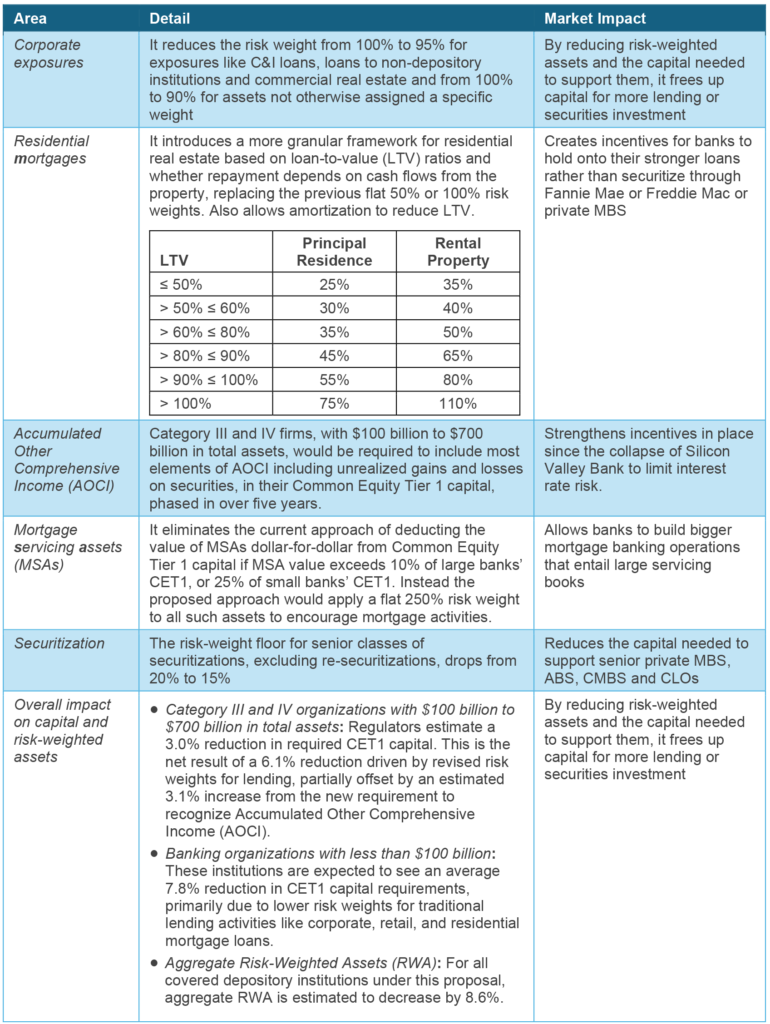

The standardized approach proposal

This first proposal generally applies to banking organizations with less than $700 billion in total assets, which covers all but the very largest. This looks to have a handful of market impacts:

- Reducing core capital and total risk-weighted assets and creating room for more lending and investing

- Keeping in place incentives that followed the collapse of Silicon Valley Bank to limit mark-to-market interest rate risk

- Creating new incentives for banks to keep their stronger mortgage loans and possibly refrain from securitizing them through Fannie Mae, Freddie Mac or private securitization

- Improving treatment of mortgage servicing assets to encourage more banks to get back in the mortgage origination business

- Marginally lowering the capital required for private securitizations

- Marginally reducing the current incentives to invest in US Treasury debt and other assets with 0% risk weights, such as Ginnie Mae MBS, by reducing the risk weights of competing loans and securities

The details are below (Exhibit 3):

Exhibit 3: Key details of the Fed’s new standardized approach proposal

Source: Santander US Capital Markets

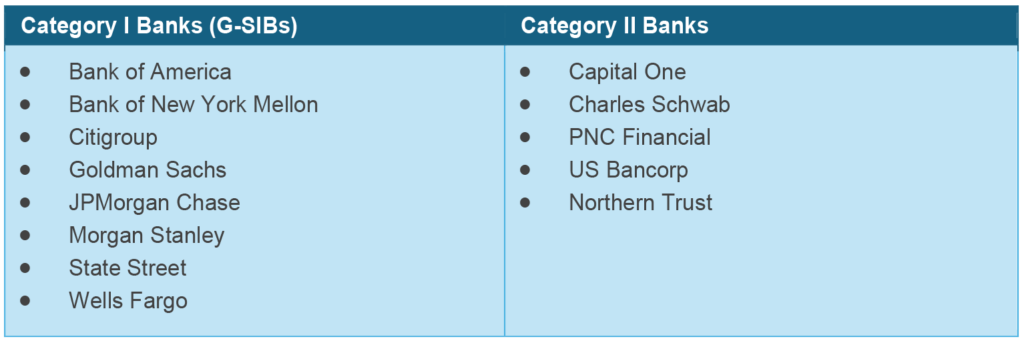

The Basel III Endgame proposal

This second joint proposal revises risk-based capital requirements primarily for Category I and II firms and firms with significant trading activity (Exhibit 4). The key elements of this proposal deal with methods of calculating risk-based capital, measuring risk in trading activities and calculating the creditworthiness of derivative counterparties. It does not have direct implications for debt capital markets, but it does in isolation increase CET1 capital by an estimated 1.4%. This is largely offset by other proposals made by regulators.

Exhibit 4: Banks addressed by the Basel III Endgame proposal

Source: Santander US Capital Markets

The GSIB surcharge proposal

This third proposal issued only by the Federal Reserve makes a series of technical adjustments to formulas for calculating system risk. It changes formula parameters, indexes some things to nominal GDP growth, changes the treatment of short-term wholesale funding, looks at average daily or monthly values of risk variables rather than quarterly window dressing, and charges capital in finer increments. This also does not have direct implications for debt capital, but it does reduce CET1 capital requirements by an estimated 3.8%. By reducing core capital, it creates more room for lending, securities investment or both.

Bigger, more competitive banks

Although the bank regulators will take comments on their proposals through June 18, these have already reflect feedback on earlier proposals for the Basel III Endgame and for the GSIB surcharge made in 2023. The latest proposals likely reflect strong consensus across regulators, banks, business and other constituencies that they are reasonable.

The proposals likely will result in bigger, more competitive banks. They should end up holding more loans and securities, competing more effectively against private debt in some cases, playing a bigger role in mortgage lending especially and tapping the usual channels for more funds to finance the growth.

* * *

The view in rates

Oil. Tariffs. Rising capital expenditure. Rising disposable income. Add to all of these the strong March payrolls and a decline in the unemployment rate, suggesting a steady if not strong labor market. The Fed has little if any room to move rates lower this year. The front end of the curve is probably stuck around 3.65% or higher for now. Fair value for the 10-year note looks like it is 4.25%, although it is likely to spend more time above that mark than below it for the balance of the year.

The 2s10s Treasury slope traded Friday at 54 bp, steeper by 3 bp over the last week, with 5s30s at 104 bp, steeper by 7 bp.

Key market levels:

- Setting on 3-month term SOFR traded Friday at 367 bp, unchanged in the last six weeks

- Further out the curve, the 2-year note traded Friday at 3.71, lower by 7 bp over a week. The 10-year note traded at 4.25%, down by 7 bp.

- The Treasury yield curve traded Friday with 2s10s at 54 bp with 5s30s at 104 bp

- Breakeven 10-year inflation traded Friday at 236 bp, down by 1 bp over the last week, with 5-year forward 5-year breakeven at 220 bp, unchanged over the last week and signaling that confidence in the Fed target still holds. The 10-year real rate finished the week at 189 bp, down 5 bp on the week.

The view in spreads

The US-Iran volatility has affected all risk assets with corporate debt also wrestling with concerns around private credit and AI. But the US ultimatums, invariably resolved, have encouraged investors to pull out the Liberation Day playbook. That playbook would anticipate slowly tighter spreads as the confrontation de-escalates. And that is how spreads have played out.

Technicals are constructive for both MBS and corporate debt. Fannie Mae and Freddie Mac continue to add to their mortgage portfolios, and insurers continue to issue annuities and buy corporate and structured credit. Supply in MBS is relatively low, although gross and net issuance in corporate debt is likely to contribute to softer spreads in that asset as that market tries to accommodate debt to finance AI buildout.

The Bloomberg US investment grade corporate bond index OAS traded on Friday at 79 bp, tighter by 1 bp on the week. Nominal par 30-year MBS spreads to the blend of 5- and 10-year Treasury yields traded Friday at 107 bp, tighter by 6 bp. Par 30-year MBS TOAS closed Friday at 13 bp, also tighter by 7 bp on the week.

The view in credit

Haves and have nots. Big companies have healthier balance sheets than smaller companies. Consumers at the middle-to-higher end of the income distribution also have liquidity and wealth. Bank lending to non-bank financial institutions, including private debt funds and business development companies continues to expand. Bank regulators continue to focus on that category of lending, which could eventually tighten the private credit markets. But for now, credit metrics for NBFI lending are strong relative to traditional bank lending such as C&I.