The Big Idea

Energy price arithmetic

This material is a Marketing Communication and does not constitute Independent Investment Research.

With oil prices more or less stable in recent days and with a clearer view of how US energy prices have reacted to the disruption in the Middle East, it is an opportune time to walk through some of the basics of how the energy price shock is evolving and what impact it will have on the economy. In particular, at current prices, headline inflation is likely to accelerate by up to a percentage point in response to the conflict.

Identifying the magnitudes

Just before the beginning of the conflict, US consumers spent around $420 billion at an annualized pace for gasoline and another $32 billion for heating oil. That compares to overall consumer spending of $21.6 trillion. Gasoline consequently has a weight of just under 2% in the PCE deflator while heating oil accounts for another 0.1%.

As of this writing, retail gasoline prices have risen since the end of February by between 35% and 40%. Applying that change to the dollar amounts above, the higher prices, over the course of a year, would cost consumers somewhere in the neighborhood of $150 to $180 billion, or $12 to $15 billion a month. This amounts to roughly half a percentage point of GDP.

As an aside, as economists have been discussing for months, federal individual income tax refunds this year are running well above year-ago levels, as households benefit from the tax changes implemented in last year’s fiscal package. Withholding tables did not change until January 1, so many households had lower than projected 2025 tax liabilities and consequently received unusually large tax refunds. Through the week of April 10, federal individual tax refunds were running almost $32 billion above the corresponding year-ago total. By comparison, last year at this time, the year-over-year advance was just under $10 billion.

In what might be considered a fortuitous coincidence, the windfall in the form of tax refunds in the aggregate may be large enough to offset the first couple of months of the energy price shock for households.

Inflation impacts

The weights of gasoline and heating oil in the CPI are somewhat larger than the above-mentioned PCE deflator weights. As of February, gasoline accounted for almost 3% of the CPI while heating oil accounted for 0.1%. In round numbers, gasoline and heating oil account for about 2% of the PCE deflator and 3% of the CPI.

Another key point is that gasoline prices typically rise this time of the year anyway. The seasonal factors assume a cumulative 10% increase in gasoline prices in March, April, and May, so the seasonally adjusted rise due to the Middle East conflict will be less than the raw gain. For example, gasoline prices rose by 24.9% in the March CPI, but the seasonally adjusted increase was “only” 21.2%. In any case, if gasoline prices surge by 40% over the three months, the seasonally adjusted jump will only be about 30%. This may limit the impact of the drag in dollar terms to somewhat less than the figures noted above.

In any case, the March surge in gasoline prices added roughly 0.75 percentage points to headline CPI. While the level of gasoline prices has leveled off and actually come down slightly over the past week, the monthly average for March ($3.70 a gallon for regular) was sharply lower than the month-end level ($4.06). As a result, the April average is likely to post an increase somewhere in the neighborhood of 10% if prices stay near the current level for the rest of the month, which would be about a 5% seasonal adjusted advance. Such a result would add another 17 bp or so to headline inflation.

We are on pace for the surge in gasoline prices to add just under a full percentage point to the CPI over the March-April period, or about six tenths of a percentage point for the PCE deflator.

In contrast to oil prices, which are essentially global (there are regional grades, such as WTI and Brent, but prices around the world move mostly in tandem), natural gas markets are local. While natural gas prices have surged in Europe and Asia (because those regions tend to import significant amounts of LNG from the Persian Gulf), natural gas prices in the US have actually fallen since the end of February, down by around 10%. The impact of gasoline and heating oil represents a full accounting of the direct impact of the energy price shock on consumer prices. Note I am not focusing here on secondary effects, like higher airfares, heightened shipping costs that feed through into good prices generally. This contrasts sharply with most economies in Europe and Asia that are dealing with sharp price increases for both petroleum products and natural gas.

Where next?

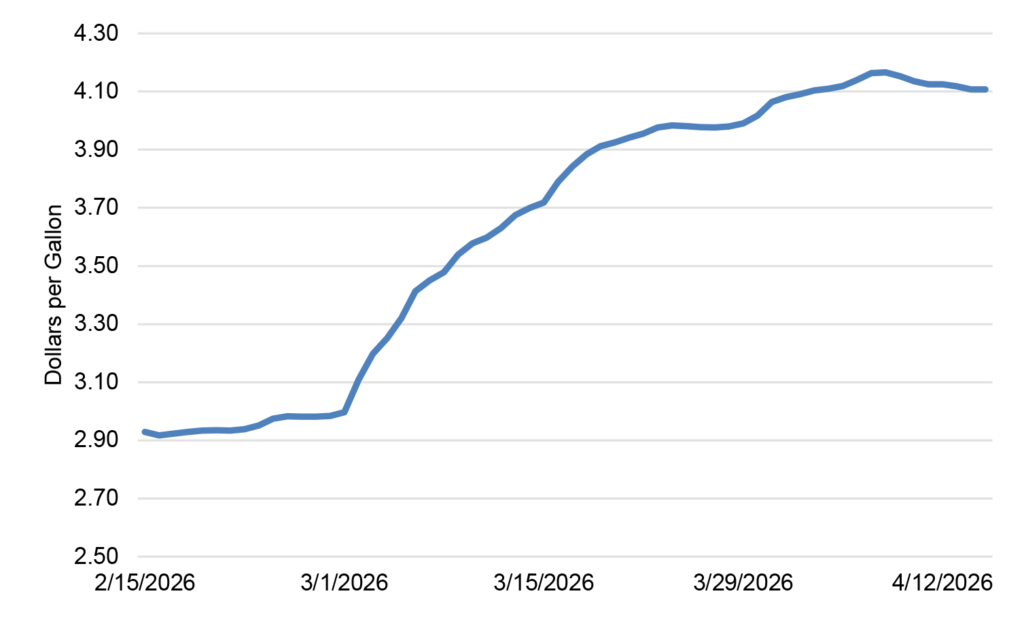

Retail gasoline prices surged quickly in March and have plateaued since late last month (Exhibit 1). Based on this trajectory, the near-term projection is solely a function of what happens from here. That is, the monthly average for April and the current level are close, so that a roughly flat performance from here would yield little change in the unadjusted figure for May, which would mean a slight negative contribution in seasonally adjusted terms.

Exhibit 1: Regular unleaded retail gasoline prices

Source: AAA.

Having said that, the situation is clearly fluid. Prices could move drastically higher or dramatically lower, depending on developments in the Middle East.

Broader view

These figures offer a limited window of the aggregate impact of the energy price shock on the US economy. In addition to the consumer spending implications for the economy, businesses will be impacted as well. Most businesses will see their input costs rise, while domestic energy producers will enjoy a massive windfall. Perhaps these effects will offset, but it is difficult to say with precision.

More importantly, heightened uncertainty could lead businesses and households to delay decisions, perhaps postponing investment projects, hiring, or, in the case of consumers, major purchases. As long as the energy supply disruptions prove temporary, this should not be a major problem for the economy, a shuffling of the timing of transactions but not a sizable drag over time. However, if the outcome of the conflict creates persistent constraints on global oil flows or if there is not a sufficiently clear resolution to restore confidence in the outlook, then the fallout could prove larger or more lasting. For now, my baseline expectation is that the downside growth implications and upside inflation risks will be predominantly temporary and short-lived, but that obviously remains to be seen.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.