The Long and Short

South Bow attractive amidst oil price volatility

This material is a Marketing Communication and does not constitute Independent Investment Research.

Violent day-to-day swings in oil prices have made it extremely difficult to price operating risk for commodity-sensitive credits in the investment grade segment. Comparatively, midstream pipeline credits that are well insulated to changes in oil prices provide stability amid global uncertainty. South Bow Corp (SOBOCN: Baa3/BBB-/BBB-) bonds seem an attractive way to position against ongoing geopolitical risk and related volatility.

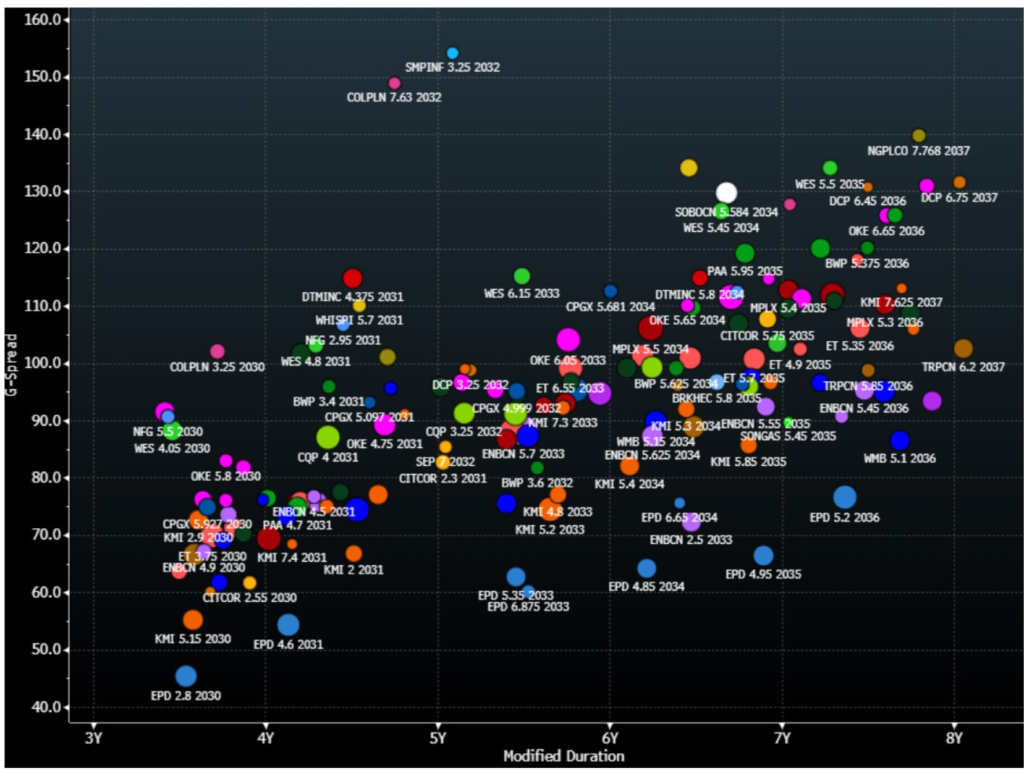

The low-‘BBB’ rated SOBOCN is among the bonds trading at the widest spreads in both the intermediate and long end of the credit curve among investment grade midstream operators (Exhibit 1). Brent and WTI prices are currently hovering around $96 per barrel as of this publication, with wild swings in day-to-day prices since early March. Though relatively small, the company exhibits many of the more stable fundamental aspects of the broader midstream segment that attract investors during periods of heightened oil price volatility.

Exhibit 1. Intermediate credit curve for investment grade midstream credits demonstrates attractive valuation for SOBOCN

Source: Santander US Capital Markets LLC, Bloomberg/TRACE BVAL G-spread indications only

SOBOCN trades wide to the rest of the sector as it remains a deleveraging story in progress since its initial spin-off from TC Energy (TRPCN: Baa2/BBB+/BBB+) in October 2024. SOBOCN exited the transaction as a 5x-levered entity with plans in place to reach 4.5x leverage by the end of next year. The company has a $700 million US dollar debt maturity coming due in late 2027, which coupled with new projects coming online in the current year, is expected to enable the company to reduce debt/EBITDA.

Importantly to debt investors, SOBOCN presents a solid liquidity profile to help execute its near-term deleveraging plans. After the $700 million due next year, the next public debt maturity is $1 billion due in 2029. The company has a $1.437 billion revolving credit facility in place through that year, in addition to about $400 million in cash on balance sheet. That means they have enough liquidity to fund debt maturities through 2029 without needing to access capital markets. Operating cash flows have been consistent in excess of $500 million over the past two years and is expected to rise moderately in the current year with the Blackrod project coming online and bringing CAD 40-45 million in EBITDA.

A criticism of SOBOCN credit quality is its commitment to a high dividend payout ratio ($0.50 per share), which is expected to be about $400 million of the $655 million in discretionary cash flows projected for the coming year. Still, it seems that policy offers cushion for management to protect investment grade ratings if operating cash flows slip and the company needs to bolster liquidity. As a smaller operator, SOBOCN has a modest debt footprint of just $4.7 billion in senior debt, as well as $1.1 billion in junior subordinated hybrid securities – which provide another layer of potential cushion to the senior debt holders if conditions rapidly worsen.

Stable cash flows among midstream credits that are not subject to oil price or volume volatility are underpinned by long-term take-or-pay contracts. For SOBOCN, these contracts represent about 85% of annual EBITDA and are seen potentially increasing to as much as 95% in the near term. The weighted average life of existing contracts is over 8 years, with a large percentage of 20-year contracts in place that do not begin expiring until 2030. Furthermore, while natural gas pipeline credits are typically preferred to purely crude operators (like SOBOCN), its customer base benefits as a result. Large, vertically-integrated refiners make up over 95% of customers, with over 90% classified as investment grade credits, vastly reducing counterparty risk.

SOBOCN operates over 3,000 miles of pipeline assets, the majority of which are its Keystone XL pipeline (95% of EBITDA). The company primarily transports crude from the Western Canada Sedimentary Basin (WCBS) to the Gulf states. While small, SOBOCN represents about 16% of all West Canada crude transported to the US. The Keystone XL alone, which ships about 620k bpd, is the third largest egress out of Canada and represents between10-15% of all crude exports. While it is a credit negative that the smaller SOBOCN ships from a single geological basin, the WCBS is an extremely stable output relative to its contract base with approximately 160 Bbbl of reserves.

Worth addressing is the risk of spills and related fines, penalties and litigation. This is a key credit factor for most pipeline credits. SOBOCN’s recent record is less than stellar with two noteworthy spills at Milepost 14 over the past few years – 13,000 barrels in December 2022 and 3,000 in April of last year. Nevertheless, related liabilities to those incidents have been absorbed, and the threat of future spills is mitigated by the company’s strong liquidity profile and other economic cushions to unplanned liabilities.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.