The Big Idea

The slow run on the bank of private credit

This material is a Marketing Communication and does not constitute Independent Investment Research.

The debt markets are watching a slow run on the bank of private credit these days even as a host of measures show steady or even improving quality for now in high yield and leveraged loans. Liquidity has become a bigger problem than fundamentals. But liquidity can turn into fundamentals if the run persists, not so much for the private debt lenders but for their borrowers. This run almost surely will require time and creativity to stop.

The list of investors trying to get out of private debt funds and business development companies continues to grow. Among the biggest reported flows:

- Apollo Debt Solutions BDC (ADS) has seen record redemption requests reaching 11.2% of outstanding shares in early 2026. Apollo has capped payouts at 5% of outstanding shares per its quarterly liquidity policy, fulfilling roughly 45% of the total money requested by investors.

- Ares Strategic Income Fund (ASIF) has limited redemptions for its $22.7 billion fund after requests reached 11.6% of outstanding shares in the first quarter.

- BlackRock’s HPS Corporate Lending Fund (HLEND) has reported roughly $1.2 billion in redemption requests for the first quarter of this year, representing approximately 9.3% of its net asset value. The fund has restricted withdrawals to its stated 5% quarterly cap, returning approximately $620 million to investors.

- Blackstone Private Credit Fund (BCRED) has received $3.7 billion in repurchase requests during the first quarter, equivalent to 7.9% of its NAV. Unlike some peers, Blackstone has fulfilled all requests by increasing its repurchase limits, supported by a $400 million investment from the sponsor and employees.

- Blue Owl Credit Income Corp has also reported record redemption requests in its non-traded BDC vehicles in early 2026.

- Cliffwater Corporate Lending Fund has seen shareholders try to withdraw at least 7% of their stake in this $33 billion fund in early 2026.

- Morgan Stanley North Haven Private Income Fund has fielded repurchase requests for 10.9% of shares. The fund capped payouts at 5%.

- Oaktree Strategic Credit Fund has allowed 8.5% of net assets to leave the $7.7 billion fund, repurchasing 6.8% of the shares with Brookfield, Oaktree’s parent company, buying 1.7% from a single investor in “a show of support” for the strategy.

It is hard to link these outflows to fundamentals. In fact, part of the problem is that current fundamentals for private credit are hard to come by. Borrowers in those markets usually provide plenty of disclosure at initial underwriting—income and balance sheet statements, customer lists, growth strategies and so on—but that information in later years often gets filtered by private equity sponsors. And there is no price signal for gauging distress. That leaves the market relying on credit in adjacent markets for clues about conditions in private debt. Most of those clues lately are stable or improving. For example:

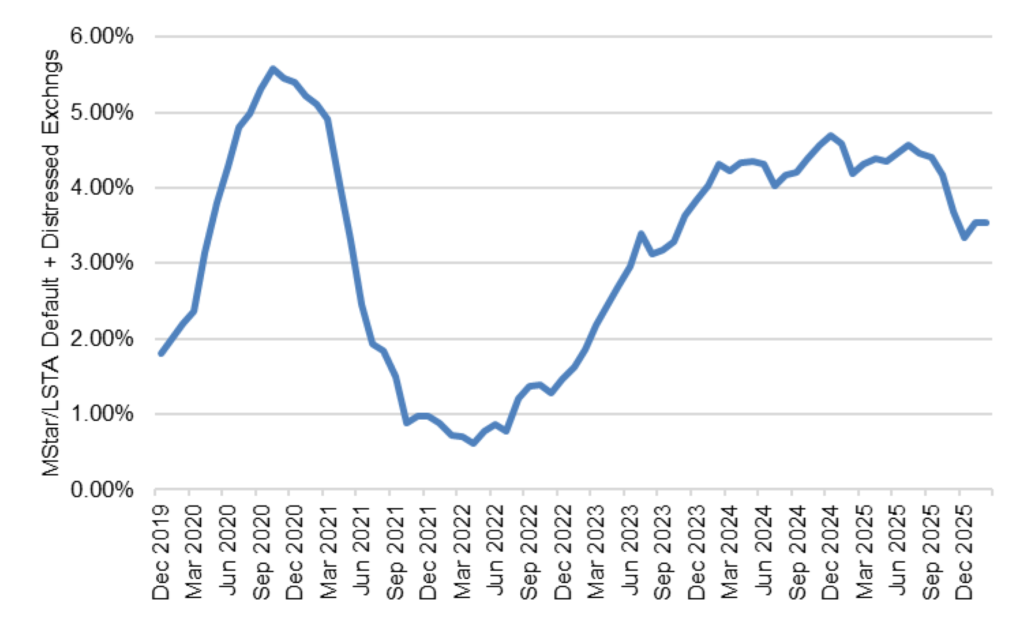

- Rates of default and distressed exchange in the Morningstar/LSTA leveraged loan index are near their lowest rates since the Fed moved into its hiking cycle in 2023 (Exhibit 1)

Exhibit 1: Leveraged loan default rates have generally declined since mid-2025

Source: Morningstar/LSTA, Santander US Capital Markets

- The Fitch US Private Credit Default Rate in January reached 5.8%, the highest mark since its August 2024 inception, but fell in February to 5.4%

- The rate of non-accruals in the Cliffwater Direct Lending Index finished December at 1.48% of cost value—up from 1.33% in September but still below the index’s average since 2005 of 2.13%

- S&P statistics only go through the third quarter of last year, but the median reported interest rate coverage for 969 speculative grade companies in the US and Canada came in either flat to coverage in the second quarter or better

The counterargument, of course, is that these credit measures are all backward looking and include benign credit conditions. The real problem may be the future impact of AI or, lately, persistently high interest rates, which are both legitimate concerns. Add to those concerns the competition to deploy private capital in recent years and the weakening of underwriting as a result. The combination of AI, high rates and weaker underwriting is new risk. But at least when it comes to AI, the impact is particularly hard to gauge. Presumably businesses that provide mission-critical services with high switching costs should survive even an AI revolution.

That leaves liquidity. The funds limiting quarterly redemptions to 5% of AUM may have enough cash to see multiple quarters of outflows. But runs tend to reinforce themselves. Investors that wait to leave during a run often end up secured by the worst loans, with all the good and more liquid ones sold long before. The incentive is for investors to rush the doors sooner rather than later. Funds running dry on cash over the next few quarters may be able to turn to banks for subscription lines or NAV lines or to other sources for liquidity. But cash eventually runs thin.

It turns out most private debt funds are probably well equipped to survive a run. Recent work led by Gregor Matvos at Northwestern University reviewed most of the private debt fund industry. It found that most funds have equity equivalent to 65% to 80% of total assets. Debt is moderate and mainly reflects bank credit lines. And portfolios are spread across industries and geography. That does not mean limited partners get out without bumps and bruises. But private funds themselves do not look like systemic risks. As for traditional banks now lending to BDCs and private debt funds, regulators find the loan quality higher than longstanding commercial and industrial lending. Any knock-on effects at commercial banks from stress at BDCs and private debt funds looks limited.

Liquidity becomes a fundamental if it forces private funds and BDCs to preserve cash and stop lending. Then the companies relying on lending from those funds may run out of cash themselves or be forced to restructure debt or end up taking on more expensive or more restrictive loans. The biggest risk is for the borrowers in the private debt markets.

A little sunshine and transparency about the status of current and future credit in the BDC and fund portfolios facing redemptions could go a long way to stabilizing the private debt market and the broader credit markets feeling the effects. The alternative will be a buyer of last resort. But prices probably have a way to go before that buyer or buyers emerge.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.