The Big Idea

Trade flows in 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

It is too early to draw conclusions about the long-term implications of US trade policies launched last year, but the final results for 2025 offer early impressions of the shifts that are occurring. The macroeconomic impacts so far have been limited, as merchandise imports continued to rise last year and the goods deficit was little changed from a year before. However, the geographical breakdown of imports suggests that differing tariff rates significantly shifted the sourcing of products from abroad.

Aggregate figures

The monthly trade figures gyrated in an unprecedented manner in 2025. The merchandise trade deficit, after averaging about $100 billion per month in 2024, ranged from a high of $162.1 billion in March, an all-time record, to a low of $58.6 billion in October, the smallest in a decade. Even so, the merchandise trade gap for all of 2025, at $1.241 trillion, was barely changed from the 2024 figure of $1.215 trillion.

Meanwhile, goods imports advanced in 2025 by 4.3% to $3.44 trillion, not dramatically different from the pace of advance in nominal GDP (5.1%). The composition of goods imports did shift notably. Purchases of overseas products by businesses picked up, as imports of industrial supplies and capital goods rose versus 2024. In particular, imports of tech goods jumped, as computers, computer accessories, and telecommunications equipment collectively surged by about $175 billion from 2024, more than accounting for the overall rise in merchandise imports. In contrast, imports of autos and consumer goods fell somewhat. This composition mirrors the performance of business fixed investment last year, as tech equipment increased sharply while the remainder of real business fixed investment declined substantially.

Geographical breakdown

While the pace of overall imports did not seem to be affected much by the dizzying array of tariff changes over the course of the last nine months of the year, the sourcing of imports did evolve substantially, likely reflecting at least in part the differing levels of tariffs levied from country to country. Exhibit 1 ranks the top ten countries (the EU is counted as a bloc) by their imports in 2024 and shows how each of them fared in 2025.

Exhibit 1: Merchandise Imports in 2024 and 2025

Source: Census Bureau.

A few themes stand out from these data. First, the US sharply lessened its imports from China. Going back to President Trump’s first term, it seems clear that one of his administration’s key objectives is to even the playing field beween the US and China. The administration believes that China engages in a variety of unfair trade practices as well as creating excess productive capacity and dumping goods into the global market in order to dominate the market for strategic products, and would like to use the heft of the US market to force China to change its behavior. In 2025, goods imports from China sank by close to 30%.

A significant portion of that diverted trade flow was rerouted through Vietnam. One key response from China to US tariffs in the first Trump term was to set up final assembly plants in third countries, export nearly finished goods to those countries, and then re-export them to the US (and elsewhere), in the process avoiding bilateral tariffs. Administration trade officials have sought to close off that loophole this time around. The trade deal struck with Vietnam in 2025 had roughly 20% tariffs for most Vietnamese products coming into the US but 40% tariffs for those deemed as “transsshipped” through Vietnam from China. Although it was outside of the top 10 in 2024, Thailand saw a similar surge in goods shipments to the US in 2025, increasing by more than 44% to $91 billion, pushing Thailand ahead of the UK and Italy.

The other major winner in 2025 was Taiwan. This most likely had more to do with a voracious appetite by US companies for advanced TSMC chips than tariffs.

Another country that fared poorly in 2025, not surprisingly, was Canada. Merchandise imports from Canada to the US fell by more than 7%. Canada and the US struggled to find common ground on trade policy all year in 2025, starting with fentanyl-related tariffs even before “Liberation Day” and continuing to the present. Imports of motor vehicles from Canada were down but surprisingly (at least to me) made up only a small part of the overall decline.

A final observation is that tariffs were not the only driver of trade flows in 2025. The UK struck the earliest and arguably the most favorable trade deal with the US in 2025 and yet imports from the UK to the US declined last year. Japan and South Korea, two other countries that ultimately struck deals with the US last year, also registered a fall in imports. In contrast, India struggled for most of the year to come to an agreement with the US, as its purchases of Russian oil created an irritant in the relationship. Nonetheless, goods imports from India surged in 2025.

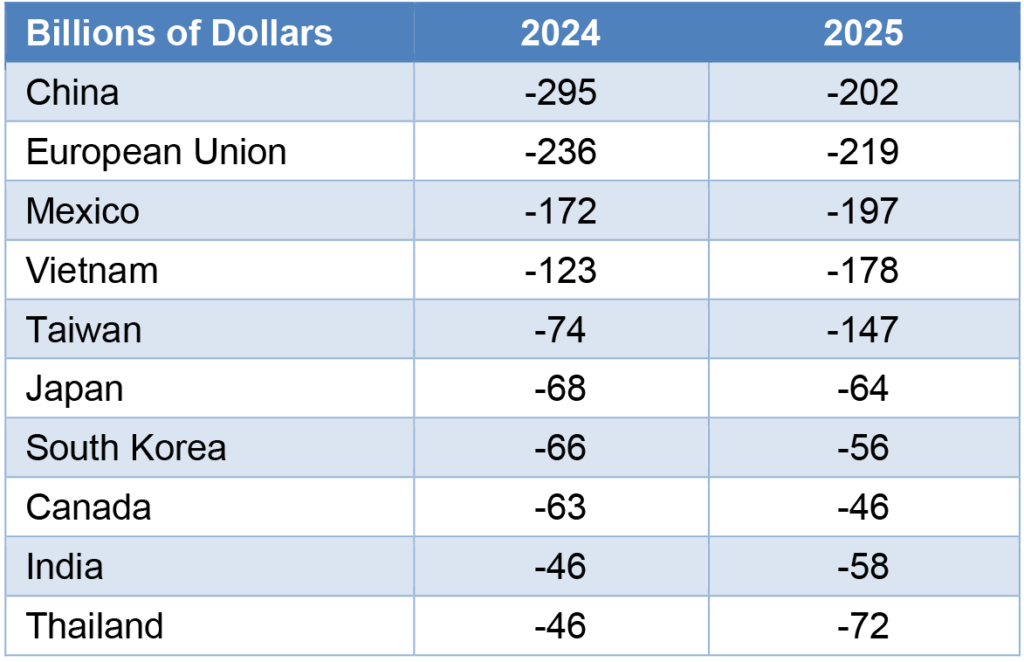

Exhibit 2 is similar to Exhibit 1 but uses bilateral trade balances rather than imports alone. So, the table ranks the countries with the ten largest merchandise trade deficits as of 2024 and then shows how they fared in 2025.

Exhibit 2: Bilateral Merchandise Trade Deficits

Source: Census Bureau.

The broad themes are similar to the import flows. The US managed to substantially reduce its deficits with China and Canada, while deficits with Vietnam, Taiwan, and Thailand widened sharply. As noted above, the deficit situation was essentially a zero-sum game, as the overall goods trade deficit was little changed in 2025 from 2024.

Conclusion

The Trump administration’s trade policy remains a work in progress, as the recent Supreme Court ruling has forced officials to pivot to a different authority and restructure its tariffs accordingly. Still, senior Administration players have clearly signaled that the goal is to essentially re-create what was in place before, so the general direction of policy is likely to remain much the same. It will be interesting to see if the Administration’s policies evolve in 2026, as there may need to be further adjustment going forward not only to the Supreme Court’s decision but also as trade data reveal how businesses are responding to the new landscape. It seems likely that the Administration may continue to seek to wean the US off of its dependence on Chinese imports over time, which, if the 2025 results are an indication, offers great opportunity for other countries in Asia to take up the baton. Another key variable for 2026 will be negotiations regarding the renewal of the USMCA, as Canada and Mexico seek to provide a stable framework for their respective exporters in what has been a volatile environment over the past year.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.