The Long and Short

Private credit concerns dominate headlines

Dan Bruzzo, CFA | March 13, 2026

This material is a Marketing Communication and does not constitute Independent Investment Research.

The rising risk of private credit defaults is currently the number one driver of volatility in the investment grade corporate bond market. Much of the concern is centered around the impact of AI on the large concentration of software borrowers in private credit markets. This story is not going away. There has been a flurry of negative headlines in the market this week, all of which have been weighing on valuation in the market. Summarizing and assessing the impact of these recent developments can be important in determining the trajectory of further selling in credit markets.

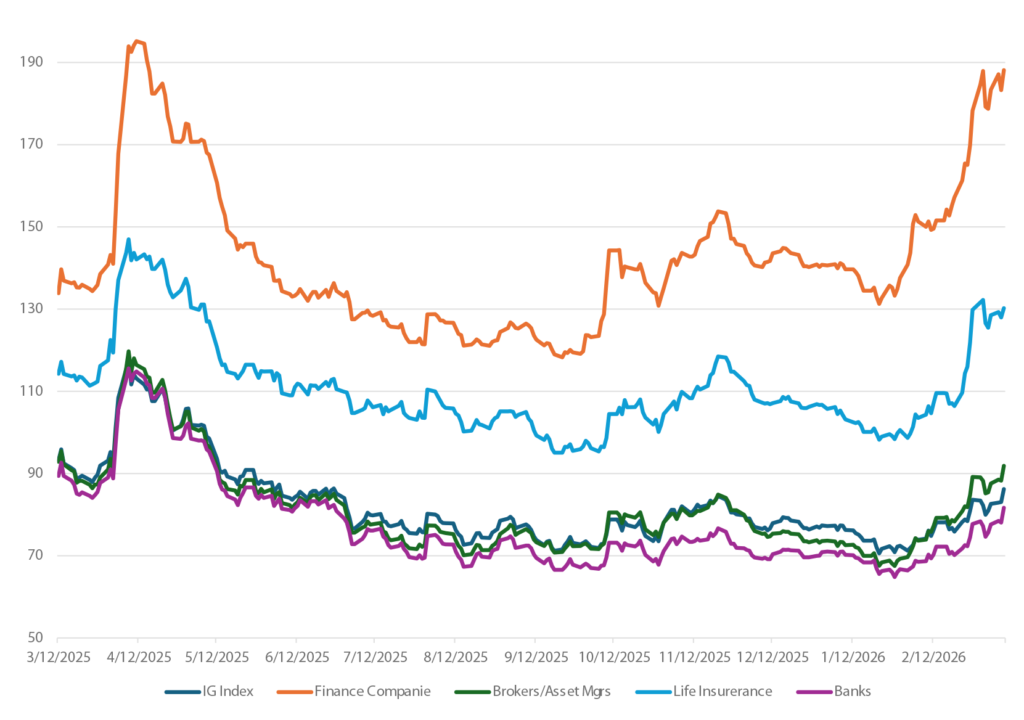

While the investment grade index has only widened by about 15 bp from the all-time tights in January—currently at a spread of 86 bp over the Treasury curve—the selling in individual sectors with direct and indirect private credit exposure has been far more significant since earlier in the year (Exhibit 1):

- BDCs: 50-150 bp wider

- Broker-Dealers/Private Equity: 25-50 bp wider

- Life Insurance: 20-40 bp wider and as much as 70-100 bp or more wider in names such as ATH and GBLATL, with double exposure through ownership by APO and KKR, respectively

- Domestic Banks: 10-20 bp wider

Exhibit 1: Corporate sector index spread performance (LTM)

Source: Santander US Capital Markets LLC, Bloomberg Corporate Bond Sector Indices

The prospect of elevated credit losses appears very real for issuers with exposure. The re-pricing of risk in the market appears mostly warranted so far. However, increases in actual default rates among investment grade issuers appear less likely to be as material, outside of maybe a few highly exposed BDCs or much smaller private equity/broker dealer credits (that probably fall outside the scope of investment grade) there does not currently appear to be significant risk of investment grade names defaulting. In high yield markets, the trend will likely be much more material. The risk of investor lawsuits also appears likely to remain a major distraction for many of the credits exposed to this trend.

For sectors such as investment grade life insurance and banks, private credit deterioration presents more of an earnings concern than catastrophic risk to credit. Life insurers, for example, are well regulated and extremely well capitalized to weather potential losses in their private credit holdings over the near-to-intermediate term. Meanwhile, the big money center banks already appear to be tightening standards and writing down exposures that may be at risk. Previous studies demonstrate instances where various sectors of the market have been selling off on private credit concerns, including the Life Insurance industry, as well as the rising tide of NBFI lending at the US money center and large regional banks.

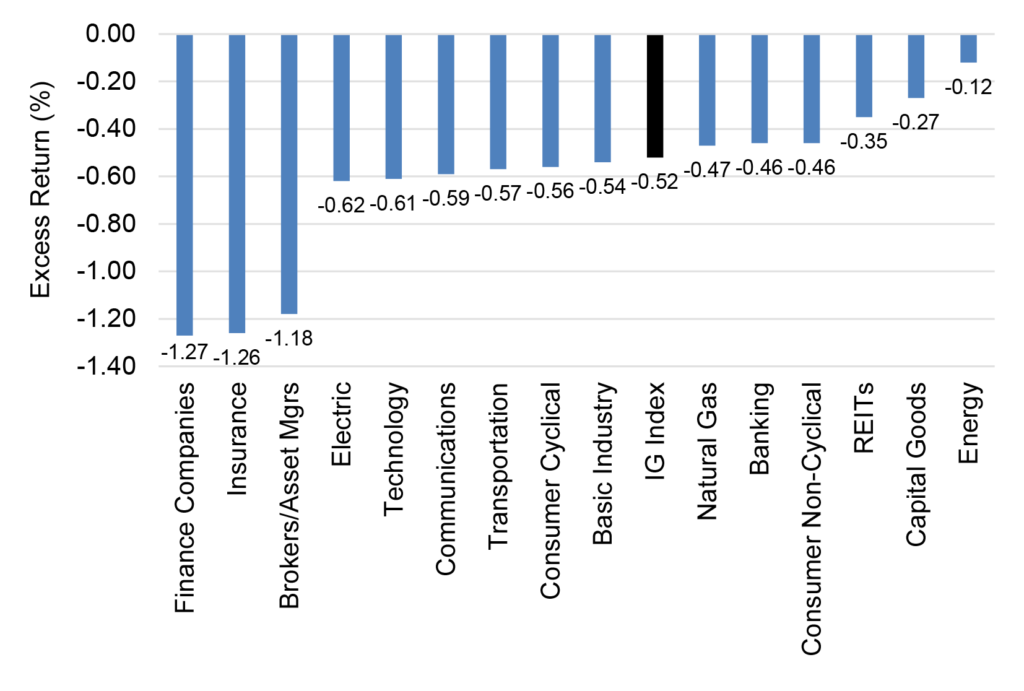

Exhibit 2 below demonstrates the excess return (credit return net of US treasury return) for the sectors of the IG index since the local tights in spreads. While fincos, insurance and brokers bore the brunt of the selloff, REITs, capital goods and (perhaps surprisingly) energy offered the safest hiding spots away from private credit. Energy’s inclusion among those sectors speaks to market’s focus on private credit concerns versus the potential fallout of ongoing geopolitical risks.

Exhibit 2. Corporate sector index excess returns (since 01/22/26 tights)

Source: Santander US Capital Markets LLC, Bloomberg Corporate Bond Sector Indices

Summary of key private credit headlines over the past week:

- JP Morgan Chase (JPM: A1/A/AA-) announced that they took significant write-downs of certain loans tied to software companies and would be restricting lending to private credit funds after the markdowns. This was probably among the most noteworthy events of the past week, as the acknowledgement on the part of the US’s largest lender elevated market concerns. It was CEO Jamie Dimon’s infamous comment regarding “cockroaches” in credit that first drew investor focus on this burgeoning issue in October of last year. The statement, alongside actual loan losses by Zions Bancorporation and Western Alliance in the third quarter of last year, brought about the first real injection of volatility to potentially affected credits in late 2025. While actual credit impact for JPM appears extremely limited at this point, the implications for the broader market are significant.

- Jefferies Financial Group (JEF: Baa2/BBB/BBB+) is facing several lawsuits, most notably from Western Alliance Bancorp (WAL: Baa3/BBB-) and a $55 billion Indiana pension fund related to the losses tied to the First Brands collapse in 2025. The Western Alliance lawsuit stems from a $337 million loan that was made to Point Bonita, a finance vehicle managed by Leucadia. The suits allege that Jefferies forced WAL into financing an agreement backed by fraudulent First Brands receivables just before the auto supplier filed for Bankruptcy. JEF had already been under pressure alongside other broker/dealer credits on suspicion that AI will deteriorate large portions of their business in the near future. While a bit of an isolated incident, the First Brands collapse alongside Tricolor serve as the first real test cases for a potential meltdown in private credit. The potential culpability of JEF in the process sets a potential precedent for highly costly and distracting investor suits, that could result in more damage for broker-dealers beyond the initial credit losses.

- Apollo Global Management (APO: A2/A/A) announced they will begin reporting the NAV of credit funds on a monthly basis, with plans to start marking private credit positions daily using third party valuations over time. These measures reflect the concerns in the market and could easily pressure more participants to ramp up transparency. Efforts on the part of asset managers and private equity concerns to be more up front regarding potential losses, particularly for credit extended to software companies, could conceivably alleviate some market pressures if investors can be convinced that they better understand potential risk.

- Numerous BDCs have been restricting withdrawals from “gate crashers,” most notably late last week BlackRock (BLK: Aa2/AA-) said it was curbing withdrawals from its $26 billion HPS Corporate Lending Fund (HLEND: Baa2/BBB-) – precipitating a further selloff in HLEND and other BDCs, as well as noteworthy selling in the AA-rated sponsor BLK itself, demonstrating the extent of investor credit concerns. Higher beta BDCs such as FS KKR Capital (FSK: Baa3/BBB-) have been hammered in credit markets. BDCs have been center stage in the selloff so far, with spread movement directly reflecting private credit concerns in the market. These types of stories are popping up more and more frequently, as the industry attempts to prevent an exodus of withdrawals. This is somewhat reminiscent of the “deposit flight” that quickly escalated the regional bank crisis of Spring 2023 after problems at Silicon Valley Bank initially surfaced.

- Pimco stated that there is a “crisis” of bad underwriting in private credit. Acknowledgement from one of the world’s largest asset managers that there is an endemic problem in credit was significant enough to draw headline interest and furthers the case that the reach of this potential market risk could be material.

- Morgan Stanley’s (MS: A1/A-/A+) investment management arm capped withdrawals from a private credit fund (North Haven Private Income Fund – $7.6 billion) after receiving requests to buy back nearly 11% of the fund. This is one of many similar stories to the BlackRock decision to curb withdrawals as well. The fact that involves a privately held fund of a US money center bank serves as a warning that risk exposure for the Big Six could extend beyond their own balance sheet.

- One of the later headlines to hit, Deutsche Bank (DB: Baa1/BBB/A-) flagged a $30 billion exposure to private credit and warned that it is also grappling with fund redemptions. The story was relevant as it drew the Yankee banks closer into the fray. To date, European bank credit has been slightly less sensitive to these developments than the domestic names. DB’s disclosure almost certainly will be joined by other banks outside the US as the issue likely evolves into a more global concern.