The Long and Short

Buy opportunity for insurance brokers

This material is a Marketing Communication and does not constitute Independent Investment Research.

Insurance brokers recently have been drawn into the fray over AI disruption after the introduction of a new app, causing spreads to widen rapidly over the past several weeks. While AI innovation carries undeniable uncertainty, the response in risk markets for insurance brokers appears overdone and creates a rare buy opportunity in a highly stable segment of the broader insurance space.

The opportunity that AI presents to generate new operating efficiencies and improve profitability among the larger competitors appears to outweigh the potential loss of revenue in more basic transactional elements of the industry. On February 9, OpenAI approved the first AI app from an insurance provider on ChatGPT, which investors quickly considered a major step toward obsolescence of more traditional channels within the industry. But this innovation appears little more than an extension of ongoing retail level automation to generate quotes for individual and commercial insurance buyers, at least initially. Complex multiline policies that need to be negotiated across multiple carriers will likely continue to rely on brokers for the foreseeable future, just with more AI analytical assistance, at potentially lower costs to the operators. Meanwhile, higher value consulting and advisory services should continue to thrive as well.

While an overweight to insurance brokers was a relative win in 2025, at the end of last year the trade had looked increasingly crowded, stretching valuations and suggesting more of a marketweight allocation. With the recent backup in spreads, investors now appear well compensated for risk and should pursue an overweight position in the segment. Insurance brokerage credits have remained a favored niche within the broader insurance sector given their relative stability to traditional property and casualty names. As traditional P&C underwriters struggled in recent years to bear catastrophe costs, those market conditions have helped the profitability of global insurance brokers with upward pressure on pricing. Furthermore, ongoing interest rate volatility and uncertainty regarding the path of the Fed still creates investment portfolio risk that more directly impacts insurance underwriters. The biggest credit risk for the industry constituents continues to be the prospect of debt-funded M&A growth.

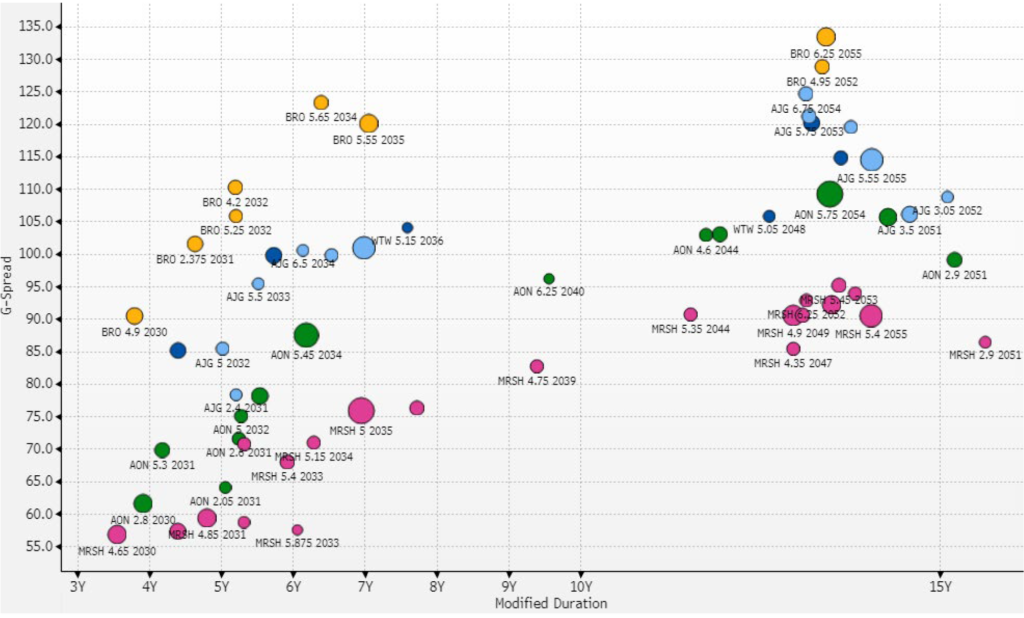

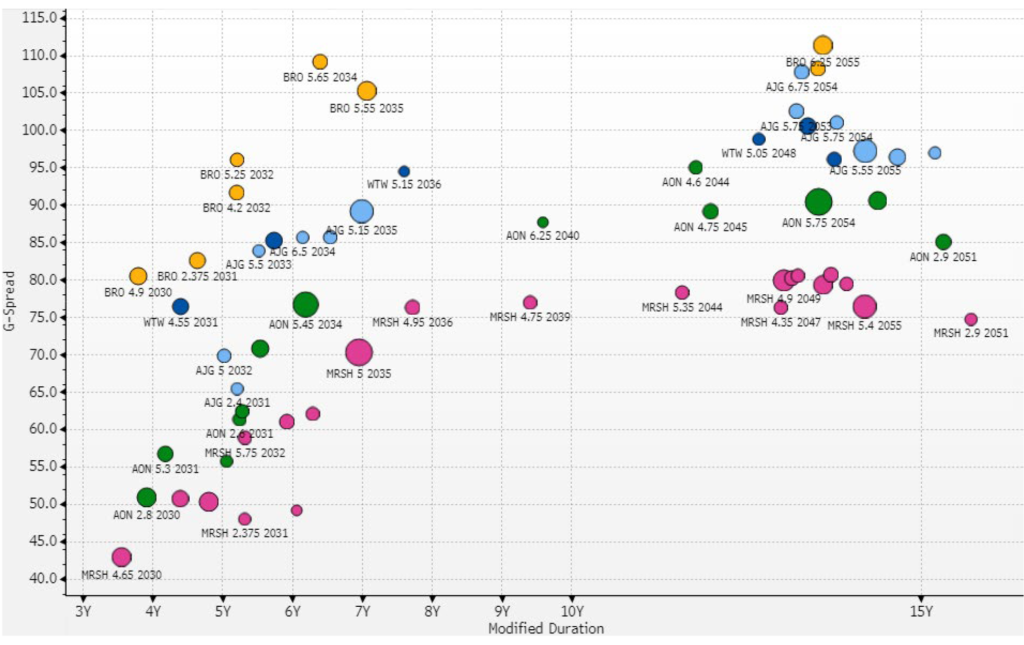

Month-to-date, investable debt within the investment grade insurance broker industry widened by an average of 13 bp across the credit curve (Exhibit 1 and Exhibit 2). Those issuers include Marsh (MRSH: A3/A-/A-), AON (AON: Baa2/A-/BBB+), Willis Towers Watson (WTW: Baa2/BBB+/BBB+), Arthur J Gallagher (AJG: Baa2/BBB/BBB+), and Brown & Brown (BRO: Baa3/BBB-/BBB). Spreads backed up as much as 20 bp to 25 bp in the long-end of the curve for the lower-rated competitors and anywhere from 10 bp to 20 bp for the largest issuers (MRSH, AON). In the early phase of the selloff, MRSH priced a new 10-year bond on February 11 at a spread of 78 bp versus initial price talk of 105 bp. This was the broker’s first debt launch since 2024, and generally performed well, currently indicated at a spread of around 75 bp.

Exhibit 1. Investment grade insurance brokers credit curve (current)

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

Exhibit 2. Investment grade insurance brokers credit curve (January month-end)

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

The bigger risks posed by AI to the insurance brokerage industry appear to lie with smaller, low-margin, transactional operators. Those are the same players that are already at risk of being edged out or assimilated by the larger investment grade players listed above. Firms like MRSH are already investing heavily in AI risk modeling and predictive analytics designed to enhance productivity and eventually improve margin performance. High volume, simple, personal home and auto policies represent an increasingly smaller and lower-margin piece of the business to the large operators. The most profitable lines of business for insurance brokers include employee benefits and health consulting, which generate tremendous recurring annual revenues and require bespoke, highly-specialized levels of service that appear far more likely to be enhanced by AI than replaced by it. Additionally, the development of complex, individualized policies that require tremendous amounts of expertise do not seem at any immediate risk as well.

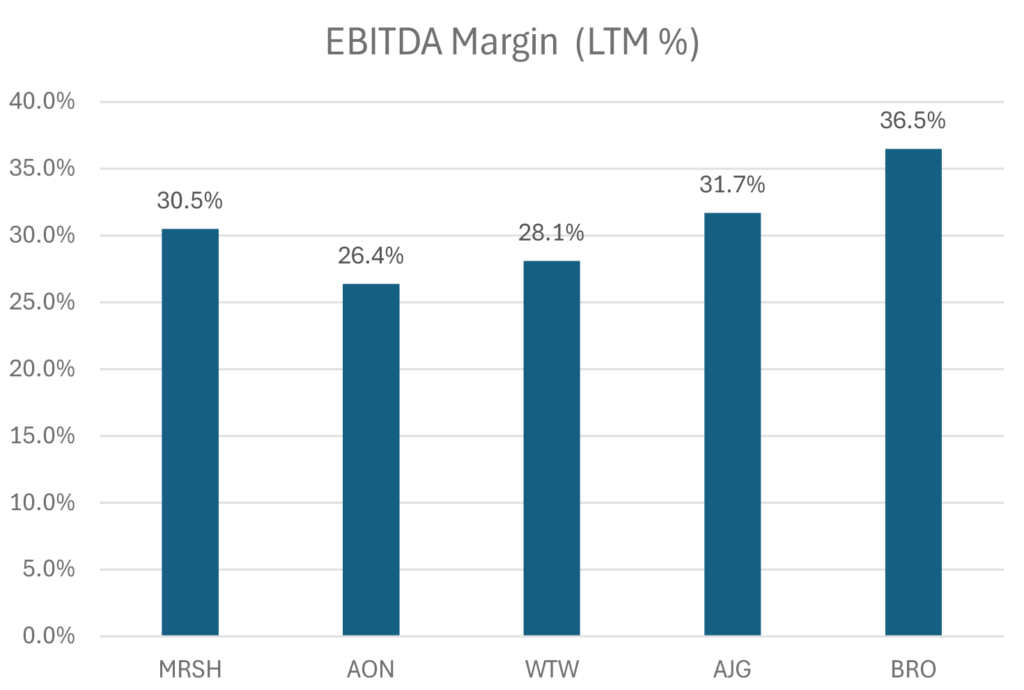

A benefit of industrywide consolidation over the past several years, as well as the efforts by the largest constituents to target the most value-added business lines, are the extraordinarily healthy profit margins sustained by the investment grade brokers year after year. Averaging over 30% EBITDA margins over the past several years across the Big Five issuers, profitability is arguably roughly double what is being generated by the major traditional P&C underwriters such as ALL, CB, PGR and so on. BRO has been a standout in this regard, as its growth strategy over the past few years has kept margins a priority over simply adding scale to match the larger players.

Exhibit 3. Insurance brokers LTM EBITDA margins (%)

Source: Bloomberg LP, Company Filings

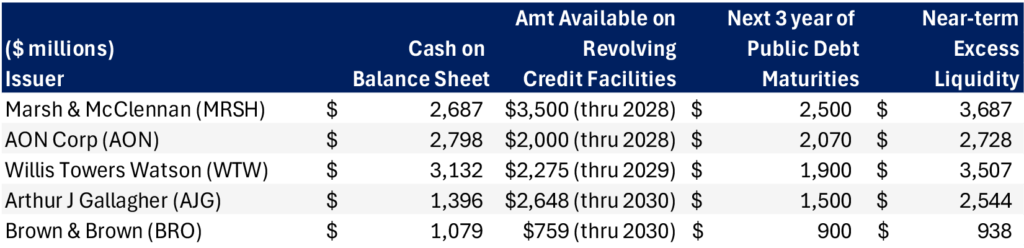

Helping backstop the credit quality of the insurance broker subgroup has always been very stable and well-funded liquidity profiles. While M&A remains a critical element of the industry, and issuers often take on additional leverage for growth opportunities, the management teams have remained committed to taking leverage down in relative short order and always maintaining adequate liquidity sources relative to their liquidity needs. BRO is a little stretched compared to the other players as the company remains in deleveraging mode following its recent acquisition of RSC/Accession for $9.825 billion, closed in August of last year funded in part with a $4.2 billion debt launch in the US dollar corporate bond market.

Exhibit 4. Insurance Brokers – Near-term Liquidity Profiles

Source: Bloomberg LP, Company Filings

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.