The Big Idea

Focus on what they do, not what they say

This material is a Marketing Communication and does not constitute Independent Investment Research.

Measures of consumer confidence have been surprisingly poor proxies over the years for actual consumer spending. Some in the media and financial markets and even some economists seem to think that negative consumer attitudes must translate into weak spending. But the correlation between opinion polls and spending has always been relatively tenuous. And rarely more so than in recent months, as historically sour consumer sentiment readings have been accompanied by solid spending results.

Grumpy households

It is well-established that households are unhappy with the current economic and financial environment. Dissatisfaction with high prices played a significant role in the 2024 election and, repackaged as “affordability,” in the November 2025 off-cycle vote. In both cases, voters punished the incumbent party in the White House for not adequately addressing their concerns.

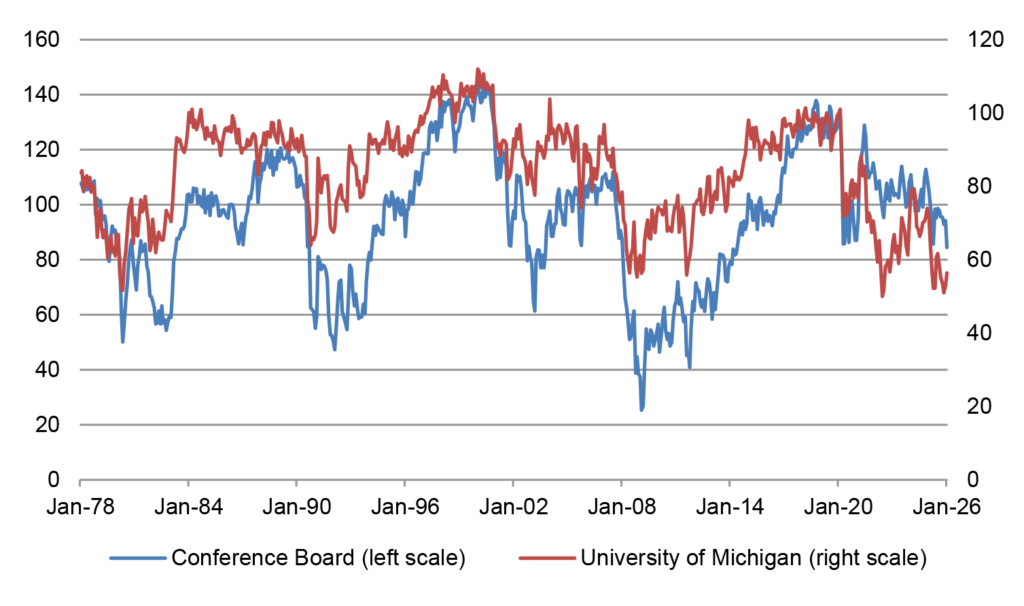

Similarly, the traditional measures of consumer attitudes spent 2025 in the doldrums (Exhibit 1). The University of Michigan consumer sentiment gauge, the red line in the chart, sank by over 20 points from the end of 2024 to the spring of 2025 and eventually declined to as low as 51.0 in November. That marked the second-worst reading on record going back to 1978, behind only June 2022 when year-over-year CPI inflation peaked for the cycle at 9%. So, attitudes by this measure were worse last year than in 1980, when CPI inflation was above 10%, worse than in the severe 1982 recession, and weaker even than in the depths of the 2008 Global Financial Crisis and the early days of COVID in 2020.

Exhibit 1: Consumer confidence measures

Source: Conference Board, University of Michigan.

The Conference Board gauge has also been soft though not quite to the same degree, falling sharply but remaining well above its all-time lows. Nonetheless, this measure posted a surprising 10-point slide in January, dropping to 84.5, the worst reading in over a decade.

It is worth noting that the two confidence surveys are somewhat different in focus. The University of Michigan survey asks about respondents’ financial situations and the broad economic outlook. It has tended, over the years, to be heavily influenced by inflation, gasoline prices in particular, as well as general news and financial market developments. In contrast, the Conference Board questionnaire also canvases households specifically on labor market conditions and thus tends to be more closely correlated with the employment situation. This may help to explain why this gauge has held up somewhat better than the University of Michigan index, since notwithstanding all of the concerns regarding the jobs landscape, the unemployment rate is still historically low.

Consumer spending

One might imagine given these household attitude readings that consumer spending has been in the doldrums. However, that is far from the case. Real consumer outlays were extraordinarily robust in 2023 and 2024, rising by 3.6% in both years. It looks like the 2025 gain will be more restrained, with the annual advance perhaps in the 2% to 2.5% range. Still, this is a far cry from what the confidence indices would suggest. Indeed, most economists would peg the economy’s long-run potential growth rate at or just below 2%, a pace of advance that consumers have exceeded for three years running.

The media are full of stories detailing the woes of American households, highlighting high prices, a weakening job market, and the struggles of lower-income households to maintain their living standards and pay their bills.

However, consumer-facing corporations consistently report that household behavior in the aggregate remains solid. JP Morgan and Bank of America executives both noted in their recent fourth quarter earnings announcements that consumers remain resilient. Mastercard and Visa also both exceeded earnings expectations in the fourth quarter on the back of strong consumer outlays.

Reconciling the diverging signals

There is no simple answer to why households feel so gloomy but continue to spend. My best guess is that households remain sour over the surge in inflation during and just after COVID. Most households fell behind in terms of purchasing power when inflation jumped in 2021, 2022, and 2023, as prices rose more quickly than nominal wages. There was a little bit of catch-up as inflation ebbed in 2023 and 2024, but for the most part households have not been made whole on a real basis. Thus, while Fed officials are determined to bring the inflation rate back to the 2% target—a goal that the FOMC has yet to come close to attaining—most households are focused on the level of prices, which is up by over 20% since just before the pandemic began. That is, even if the Fed is successful in getting the inflation rate back to 2%, households will still be angry because the level of prices is so much higher than before COVID.

To keep up, households have been forced to stretch. The savings rate was running at close to 7% in the years leading up to the pandemic. It has since trended down, ending 2023 at 5.6%, 2024 at 4.3% and the latest reading (November) was 3.5%. So, households have maintained their spending patterns by saving less. At first glance, this is unsustainable, but households may have an eye on their asset holdings. Household net worth has exploded since 2019, rising by nearly $70 trillion in less than six years. However, due at least in part to the level of interest rates, which has cut off the option for most of cash-out refinancings, households are not borrowing aggressively. Household debt as a percentage of GDP and as a percentage of disposable income has been on a steady downtrend since the Global Financial Crisis and, aside from a few distorted readings during the pandemic, both measures are at their lowest levels since the 1990s.

Consumers in the aggregate may feel comfortable running down their savings rate because they are not tapping into their growing asset values (mainly equity portfolios and their homes). This may also help to explain the diverging fortunes of upper- and lower-income households, since the bulk of the asset holdings are held by wealthier families. Those at the low end of the income spectrum do not have large nest eggs to backstop their spending patterns and thus are at risk of running into financial problems if they increase their outlays faster than their incomes are growing.

This pattern may explain why the aggregate consumer spending numbers continue to be healthy while stores report that their lower-income customers are showing signs of financial stress. Those in the upper half of the income scale, who hold a disproportionate amount of income and assets and thus account for the bulk of overall spending, are propelling the overall figures, while those without access to fallback resources are struggling to stay above water.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.