By the Numbers

A private-label MBS buyer’s guide for 2026

Chris Helwig | December 5, 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

Investors in non-agency MBS need to start thinking about positioning for next year. Faster prepayments and increasing issuer calls should make discount exposures across non-QM and second liens a straightforward way to add performance. Investors in prime MBS at the top of the capital structure should skew purchases toward par-priced agency-eligible investor pass-throughs and sequentials, which should continue to deliver relatively attractive carry. Faster jumbo speeds should point investors to discount pass-throughs or shifting interest subordinates that should benefit from faster speeds.

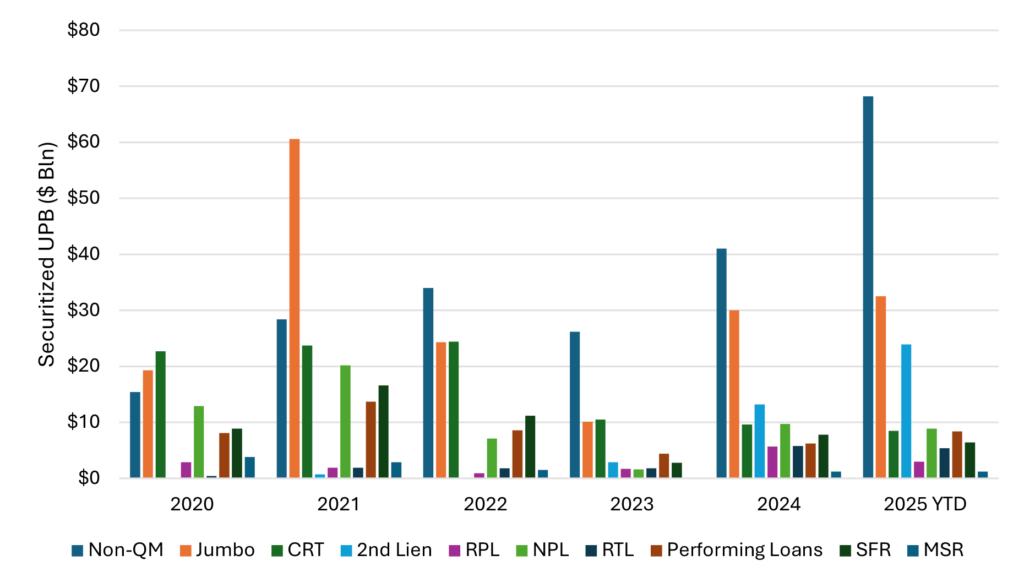

Non-QM and second liens likely to fuel continued growth of the PLS market

The private-label market grew by nearly 30% this year. Securitizations of non-QM and second lien collateral fueled much of that growth, increasing by 66% and 81% respectively (Exhibit 1). With these two exposures poised to continue to grow next year, investors should remain focused on these asset classes along with securitizations backed by prime loans.

Exhibit 1: Non-QM and second liens drive PLS growth

Source: Santander US Capital Markets, CreditFlow

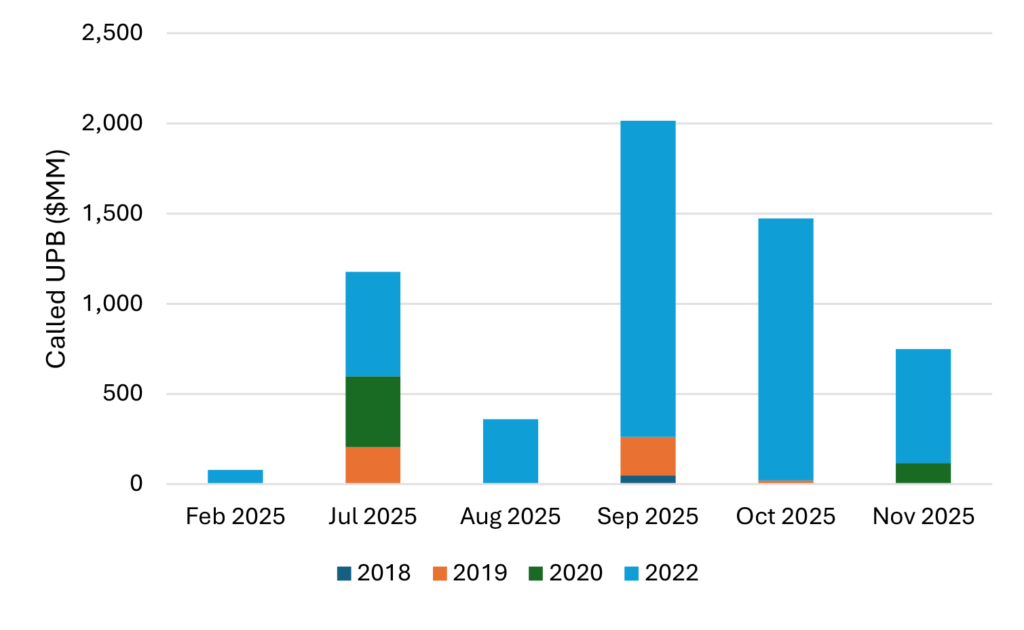

Call activity likely to rise in non-QM

The latter half of this year has seen somewhat elevated call activity among sponsors of non-QM securitizations. Invictus and Lone Star Funds have been the most active, but permanent capital sponsors including Annaly, Rithm and Angel Oak have called deals as well. The majority of call activity has been localized to 2022 vintage transactions as they have rolled into the three-year call window. Some 2020 vintage deals have been called as well (Exhibit 2).

Exhibit 2: Call activity increases in 2020 and 2022 vintage non-QM deals

Source: Santander US Capital Markets, Intex Solutions, Bloomberg LP

Deals from 2022 were issued against the backdrop of aggressively increasing front-end rates and widening spreads, which squeezed levels of excess spread and reduced securitization advance rates, hampering securitization economics. As a result, sponsors of these deals have substantial incentive to call and re-lever these deals, especially if rates in the front end of the yield curve continue to drop with a potentially more dovish Fed next year.

Deals from 2020 and to some extent 2021 may get called more often as well next year. De-levered transactions that have seen a material increase in sponsors’ cost-of-funds as lower cost, pro-rata pay debt at the top of the capital structure has paid down or in some instances paid off almost entirely. From the asset side of the transaction, these calls look modestly uneconomic, but not materially so. With 7.0% gross WAC new originations trading at roughly $103, most 2020 vintage deals are roughly 150 bp out-of-the money relative to current production. Assuming a roughly 3-year duration on the lower gross WAC ‘tails’ of these 2020 vintage deals would imply that these pools should be trading a roughly a one-point discount to par when multiplying the coupon differential times the duration to estimate the discount.

Given the relatively small discount, it could be offset by hedges that the sponsor put in place, although payer swaptions would likely be struck to the first call date given the lack of step-up in most 2020 vintage transactions and would have long since expired. Alternatively, the discrepancy between the market price of the loans and par could be offset via sponsors reducing their call basis through ownership of discount subordinate bonds. Additionally, sponsors may be incentivized to call these transactions simply given the nature and duration of the funds in which the equity resides. The sponsor may have to return capital after five years assuming a two-year invest, three-year harvest structure for limited partners in the funds, facilitating the need to call the deal and either sell the loans or re- lever them through securitization to raise cash to return to investors.

These trends collectively create opportunity for investors to capitalize on elevated call activity to the extent that they can source discount bonds that will pull to par at call. The best opportunity may be in investment grade subs 2020 and 2021 vintage where the majority of the lower cost, senior debt stack has been paid down or senior 2022 and 2023 vintage seniors that were issued during periods of relatively lower benchmark rates and tighter spreads. To date, it appears the market has put some weight on sponsors calling lower WAC deals. 2020 and 2021 vintage deals price to 10 CPR despite empirical speeds generally being much slower. Implicit in that assumption is some probability that these deals will pay 100 CPR at call and the 10 CPR assumption is a ‘blend’ of empirical speeds and call probability. It seems likely that bets placed on those calls may hit with increasing frequency next year.

Prime speeds spiked in recent months, look likely to remain fast

Speeds on 2023 and later vintage prime jumbo deals surged in the October remittance cycle and remained fast last month. Investors in higher loan balance collateral have always been exposed to elevated prepayment risk as smaller amounts of incentive translate to larger nominal savings for larger loan borrowers. This risk may be more acute now than in years past as certain conforming balances have pushed well north of $1 million, dragging securitized non-conforming balances higher. In addition to higher balances, persistently elevated mortgage rates have likely made higher balance borrowers increasingly sensitive to any ability to reduce existing debt burdens as evidenced by fast speeds in 2025 vintage deals.

Absent a material bear steepening of the yield curve that would push the majority of recent jumbo originations out-of-the-money, speeds on jumbo collateral look likely to remain fast. This should push investors at the top of the capital structure in jumbo deals into discount pass-throughs. And credit investors should favor discounted shifting interest subordinate classes over other exposures as fast prepayments will both de-lever the senior portion of the capital structure, increasing credit support and tightening spreads on longer spread duration shifting interest subs, and shorten the bonds, generating excess returns through a pull to par.

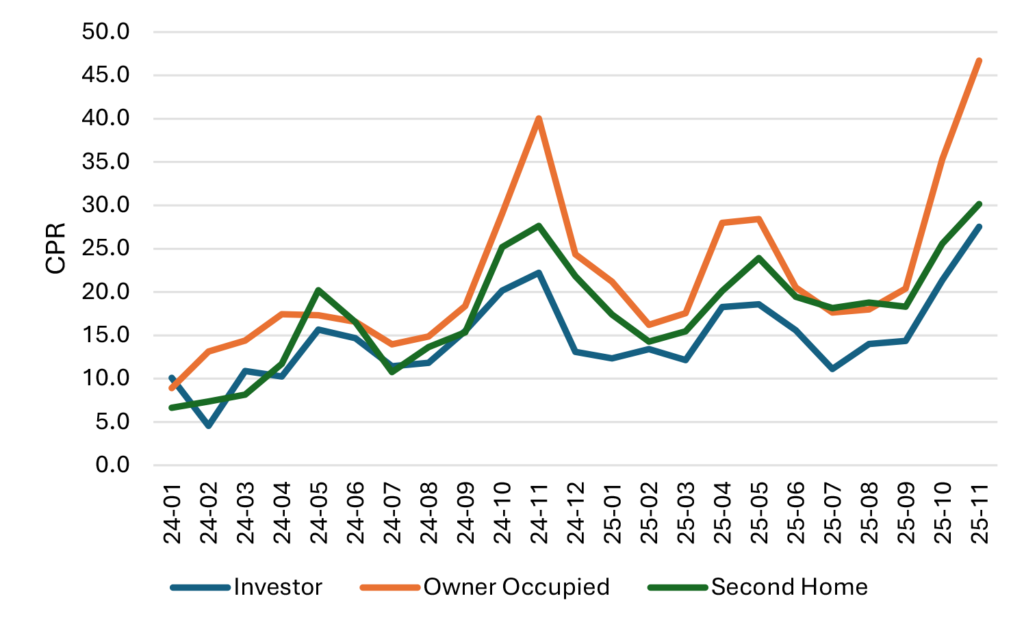

Prime investors at the top of the capital structure seeking refuge from fast jumbo speeds could also skew private-label allocations to agency-eligible investor collateral as those loans have paid significantly slower than recent vintage prime jumbo (Exhibit 3.) While differences in new issue spreads between jumbo and investor pass-throughs have widened to some degree, the convexity in investor collateral still appears to be mispriced. At an absolute minimum, bond investors are offered significant prepayment protection from the fact that the average balances of loans securitized in prime investor trusts are a fraction of jumbo balances. Furthermore, there may be a more muted refinancing response to higher LTV, higher SATO agency-eligible loans securitized in private-label trusts than lower LTV ones more commonly purchased by the GSEs as originators will likely look to refinance lower LTV loans with less friction to refinancing than higher LTV ones.

Exhibit 3: Investor speeds have remained relatively muted compared to prime jumbo

Source: Santander US Capital Markets, Core Logic Loan Performance

Agency-eligible investor pass-throughs also compare favorably to agency specified pools. With 5.5% pass-throughs trading at a 12/32 concession to TBA and 5.5% specified investor pools trading at an 11/32 pay-up in the most recent GSE cash window auction, that price differential translates to a 30 bp pickup in OAS in the private-label pass-through (Exhibit 4). Admittedly, investors should demand some concession for lower liquidity in private-label bonds, but the cost of liquidity is notoriously difficult to value, and 30 bp may be more than fair compensation for buy-and-hold investors with stickier funding and capital.

Exhibit 4: Investor pass-throughs offer a substantial OAS pickup versus specified pools

Source: Santander US Capital Markets, YieldBook

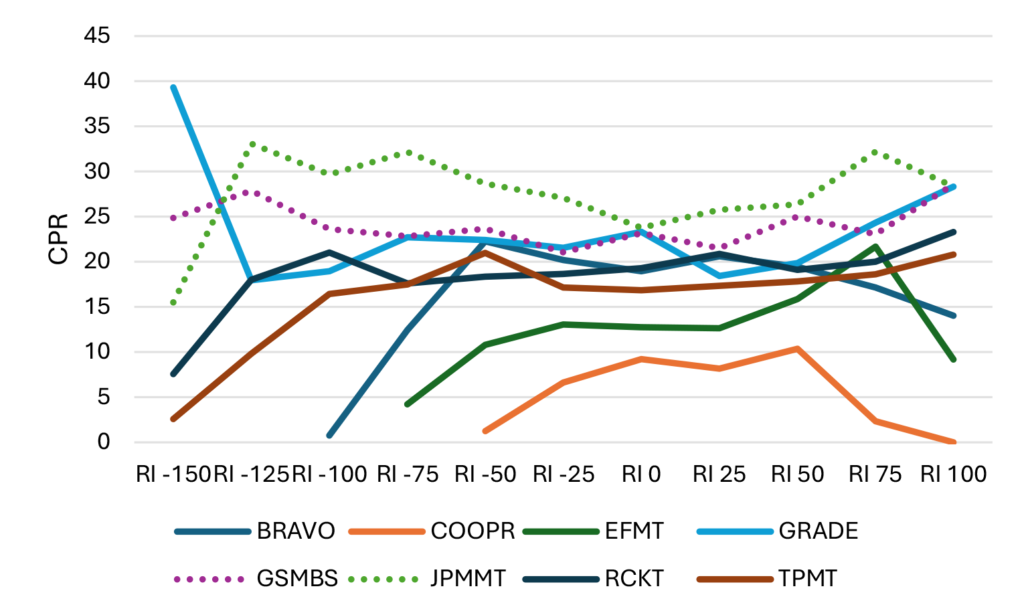

Screening for convexity in second liens

Capitalizing on elevated speeds in second liens is somewhat more challenging as the majority of the capital stack is par-priced at issue. Investors may find select discount bonds that were issued against the backdrop of higher rates or wider spreads but a further rally in the front end of the yield curve may push these bonds above par. Given this, investors may be relegated to shelf selection to protect against elevated speeds. To date, dealer shelves including JPPMT and GSMBS along with the Saluda Grade shelves have been faster at-the-money than originator and other sponsor shelves as originators may be less inclined to solicit second to second refinances to keep speeds contained and protect elevated premiums on future whole loan sales (Exhibit 5).

Exhibit 5: Dealer shelves prepay faster in second liens

Source: Santander US Capital Markets, CoreLogic LP

Prepayment speeds on second liens may decelerate somewhat organically as home price appreciation slows as many refinancing opportunities have been borne of incentive created via borrower deleveraging through a combination of amortization on lower coupon seasoned first liens coupled and substantial home price appreciation. Until then, investors will be well served to opportunistically buy bonds at a discount and allocate capital to shelves that have exhibited slower speeds across varying rates of refinancing incentive.