By the Numbers

Out-of-consensus calls in mortgage credit for 2026

Chris Helwig | November 21, 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

Prepayments on discount MBS could increase next year as reductions to LLPAs on purchase loans both improve housing affordability and lift turnover. Spreads on ‘AAA’ non-QM classes should tighten as a little structural innovation brings more buyers to the asset. And prepayments on second liens look likely to continue to surprise to the upside, potentially worsening the convexity of that emerging asset absent some policing of refinancing activity. These are a few areas where consensus hasn’t yet priced away likely excess return in MBS over the next year.

Fannie Mae and Freddie Mac wrestle with a dual mandate

Fannie Mae and Freddie Mac are currently tasked with what appears to be somewhat of a conflicted dual mandate; increase profitability at the companies while simultaneously improving affordability for homeowners. Straightforward ways to improve profitability such as increasing base guaranty fees and LLPAs or broadening the scope of loans that the enterprises can purchase are at odds with stated administration objectives to reduce financing costs for borrowers and increase the amount of private capital that supports the US housing and mortgage finance ecosystem. Ultimately this dual mandate may not be concurrently achievable, and the administration may have to decide whether Priority One is to lower costs to borrowers or reap the potential windfall associated with selling Treasury’s existing preferred stake and warrants.

The most straightforward potential win for the administration and FHFA looks to be on the affordability side, where rolling back certain increases to LLPAs enacted in 2023 could lower homeownership costs for higher FICO borrowers. Specifically targeting purchase loans could help more borrowers to get into homes while not materially worsening the convexity of the universe that would come with a reduction in LLPAs on refinance loans. Admittedly, the reduction in revenue would move the goalpost further away with respect to making the enterprises ‘IPO ready’ but there look to be far larger impediments to a public offering.

Changes to purchase LLPAs would likely center around rolling back controversial changes which dramatically reduced risk-based pricing for higher LTV, lower FICO borrowers while modestly increasing fees for better credits. For example, borrowers with FICO scores of less than 640 that put up just 3% of the home’s value saw LLPAs fall by 1.75%. Borrowers with credit scores ranging from 720 to 759 that put up slightly less than 20 points of equity, on the other hand, saw their LLPAs rise by 0.75% on purchase loans. Flattening the LLPA grid would make homeownership more affordable for better credits and ostensibly increase volumes as more borrowers would be able to afford the reduced payment. Of course, a flatter LLPA grid would reduce the enterprises’ ability to cross-subsidize weaker credits with better ones, potentially creating the need to either increase risk-based pricing on those loans or push more of those borrowers into FHA execution.

Other policy ‘trial balloons’ such the introduction of a 50-year mortgage and assumable or ‘portable’ mortgages appear better warehoused under enterprises in conservatorship rather than privatized ones looking to maximize profitability. And each one of these ideas to lower borrowing costs come with their own unique set of challenges.

The 50-year mortgage appears to be a fundamentally flawed instrument by which to improve affordability. The amortization extension pushes most of the principal deleveraging far out into the future, mitigating borrowers’ ability to build equity and nearly doubling the amount of interest paid by the borrower over the life of the loan relative to a 30-year mortgage. Furthermore, a 50-year mortgage is not a Qualified Mortgage under legislation enacted in 2014. That means the GSEs would be unable to purchase and wrap the credit risk on these loans without a ‘QM patch’ similar to the one afforded years ago to the enterprises that allowed them to buy loans with elevated debt-to-income ratios. With a patch, the 50-year loans would have to sit on the balance sheets of banks, insurance companies or be securitized in the private-label market. The duration profile of these loans appears ill fitting for bank balance sheets given the duration of their liabilities. And it’s unclear whether there is adequate appetite from insurance and pension buyers given the embedded negative convexity, as they may pair poorly against long-dated annuity and pension liabilities.

The broad-based adoption of assumable or portable mortgages come with their own unique set of challenges. The ability to ‘port’ a mortgage to a new home potentially offsets some of the lock-in effect that keeps homeowners tethered to houses with low cost financing but could have the unintended effect of pushing home prices higher as borrowers who locked in low rates will have more purchasing power and ostensibly a significant advantage over borrowers that have to finance all of the associated mortgage debt at prevailing rates.

Additionally, the ability to ‘take your mortgage to go’ would fundamentally change the risk paradigm of these loans. Depending on the value of the newly purchased property, investors in bonds backed by portable mortgages may bear more credit risk in the form of a higher LTV or being exposed to an MSA which may be more prone to home price depreciation. Portable mortgages would also introduce more extension risk to the market, increasing the duration of the mortgage universe and making it far less predictable absent substantial empirical observations of how and when these loans would ultimately abate. Finally, as evidenced with assumable mortgages, existing financing generally works best in areas where there hasn’t been material home price appreciation. If the value of the home or housing stock has grown appreciably in value, there may be large gaps between the existing debt financing and the amount of up-front cash equity available to borrowers. Ostensibly this equity gap could be closed with subordinate financing. But depending on the size of the subordinate lien, borrowers’ savings versus prevailing market rates may not be all that substantial.

Non-QM can go as far as growth in its investor base takes it

One of the largest impediments to growth in post-crisis private-label market has been the paring back of that investor base. A recent structural change to non-QM securitizations could help bring new buyers to the fore. Carving the existing ‘AAA’ class into a 75% front cash flow, 25% last cash flow both shortens the average life and tightens the principal window on the ‘AAA’ front sequential making it a more akin to short ‘AAA’ ABS. This change could attract more indexed ABS buyers looking for out-of-index exposure at wider spreads to generate alpha in their portfolios or non-indexed ABS buyers looking to avoid fundamental or headline risk in the subprime auto or home improvement sectors given recent, highly publicized of defaults or bankruptcies of companies like Tricolor, First Brands and Renovo.

Prior to the Global Financial Crisis, the private-label market, and more specifically ‘AAA’ classes of private-label deals, garnered broad-based support from domestic and European banks, the GSEs and overseas investors along with domestic asset managers, insurance companies, REITs and hedge funds.

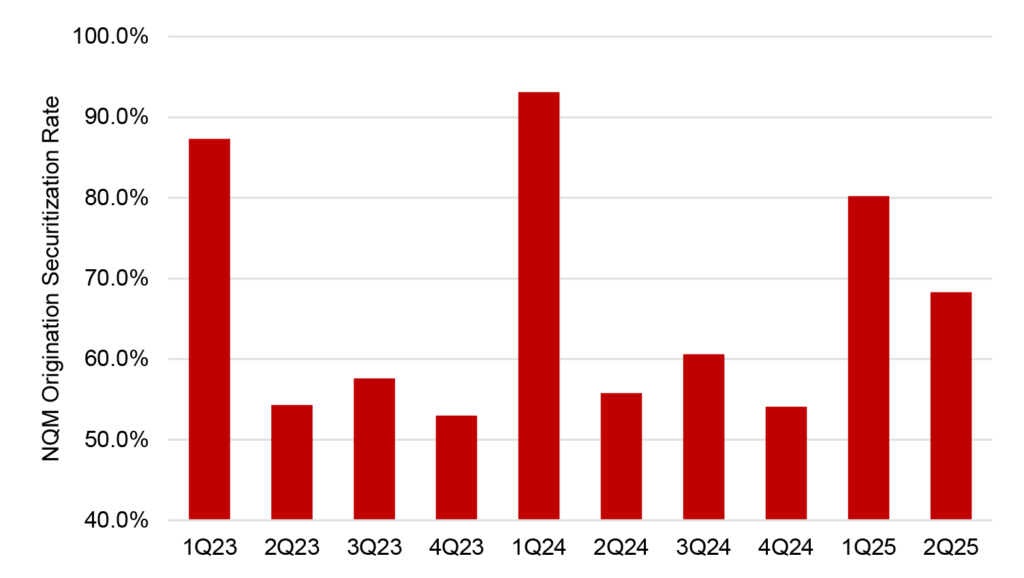

Insurance companies have stepped into the breach, providing significant ballast to growth in the non-QM market. Life companies have been the biggest driver of growth in the non-QM market through direct investments in both whole loans and securities as well as indirect investments in both whole loans and securities through Separately Managed Accounts (SMAs) managed by both traditional and alternative asset managers. Demand for non-QM whole loans from insurance balance sheets has proven to be somewhat of a governor on capital markets execution during bouts of volatility as their stickier, more stable liability structures have allowed them to be a more consistent and stable bid for loans in bouts of broader market risk-off sentiment. Balance sheet demand from life companies for non-QM whole loans can be seen in the draw down in securitization rates for the asset class over the past three years. Absent the first quarter of the past three years, securitization conduits have taken out slightly more than half of non-QM originations, with most of the additional production flowing to insurance balance sheets (Exhibit 1).

Exhibit 1: Securitization conduits compete with life company balance sheets for non-QM loans

Source: Santander US Capital Markets, Inside Mortgage Finance

Strong demand from life companies has been driven by the attractive levered returns they can offer. Residential whole loans garner favorable capital treatment, requiring just 68 bp of risk-based capital, although insurance companies generally hold multiples of the statutory minimum to be considered well capitalized. Life companies that are member of the Federal Home Loan Bank system can then lever these assets using a combination of FHLB advances and fixed annuities to term fund these assets at an attractive all-in cost of funds.

Since much of the demand for whole loans has been a byproduct of elevated levels of annuity sales, continued strong demand from life companies is likely tethered to continued consumer demand for the product. And there may be some risk to that if long rates fall meaningfully. Recent dramatic growth in annuity sales has been commensurate with the rise in long rates which started in 2022 (Exhibit 2). A protracted rally in the belly of the curve and beyond could dampen annuity growth and demand for non-QM whole loans along with it.

Exhibit 2: Annuity sales rise with higher rates

Source: Santander US Capital Markets, Bloomberg LP

If insurance demand wanes, domestic depositories could fill the void or even be a source of outright net demand even in the presence of a strong insurance bid. But that would only likely occur against the backdrop of a more lenient regulatory backdrop. Domestic banks have by and large been casual participants at best in the 2.0 market. Despite bonds at the top of the capital structure comparing favorably to agency MBS when looking at them on a risk-based-capital-adjusted return basis, many banks have shied away from investing in the private-label market due to more onerous treatment of those assets under Fed stress tests. Relaxation of regulatory requirements that have stymied bank demand could bring domestic depositories back as a meaningful source of demand given the shift in bank risk appetite towards shorter, more positively convex investments.

Second liens, they’re back and they’re fast

The securitized second lien market saw a meaningful resurgence this past year. Year-to-date securitization volumes have surged to over $22 billion after tallying $14 billion for the full year last year. While it took a long time for second lien lending and securitization to get off the mat, the recent pace of growth has been somewhat remarkable. What used to be a niche market marked by smaller fintech originators has morphed into a space dominated by the largest and most efficient non-bank originators, which has driven down both customer acquisition and other origination costs, pushing origination volumes higher. Concurrently, the asset has garnered strong institutional support, with the basis between ‘AAA’ classes of second liens and the far more established non-QM asset class collapsing to near zero.

The asset class has seen its share of growing pains though. Vastly improved efficiencies in origination have translated to less friction to refinancing these loans than many market participants have anticipated. A more captive borrower base coupled with lower origination costs have translated to the sector being marked by elevated prepayment speeds. Increased efficiency has not been the only culprit contributing to elevated prepayment speeds in the sector. Deleveraging via both home price appreciation and substantial amortization of seasoned, lower coupon first liens has combined to push newly originated, higher CLTV second liens down a steep LLPA pricing grid, creating refinancing opportunities for borrowers even in the absence of rate-related moneyness.

While a slower grind upward in HPA should stem refinancing opportunities to some degree, these loans will continue to de-lever through amortization. This sets up an interesting quandary for originators of second liens into 2026 and beyond. Namely, whether to proactively refinance existing second liens or not. Proactively soliciting ‘second-to-second’ refinancing opportunities drives gain-on-sale, reduces the blended rate to the borrower and ostensibly further protects the first lien MSR from being refinanced into a cash-out refinance consolidation loan at some point, all of which argue for creating significant incentives for originators to proactively pursue refinancing these loans. However, elevated second lien refinancing activity and the attendant pick up in prepayment speeds will cause investors to restrike valuations on residual classes of these deals lower, pulling premiums on whole loan sales lower as well. Ultimately, second liens look to be a permanent fixture in the private-label landscape going forward, whether they continue to fetch the lofty valuations they did this past year is arguably less certain.