The Big Idea

Buying credit, selling liquidity

Steven Abrahams | November 14, 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

Among the managers of leveraged loan portfolios gathered for a conference in Tokyo last week, few if any had any real worries about credit. First Brands, Tricolor and other names in trouble lately all had unique problems. The broader state of credit otherwise is good. It was a bit like Tolstoy. “All happy families are alike,” he wrote, “each unhappy family is unhappy in its own way.”

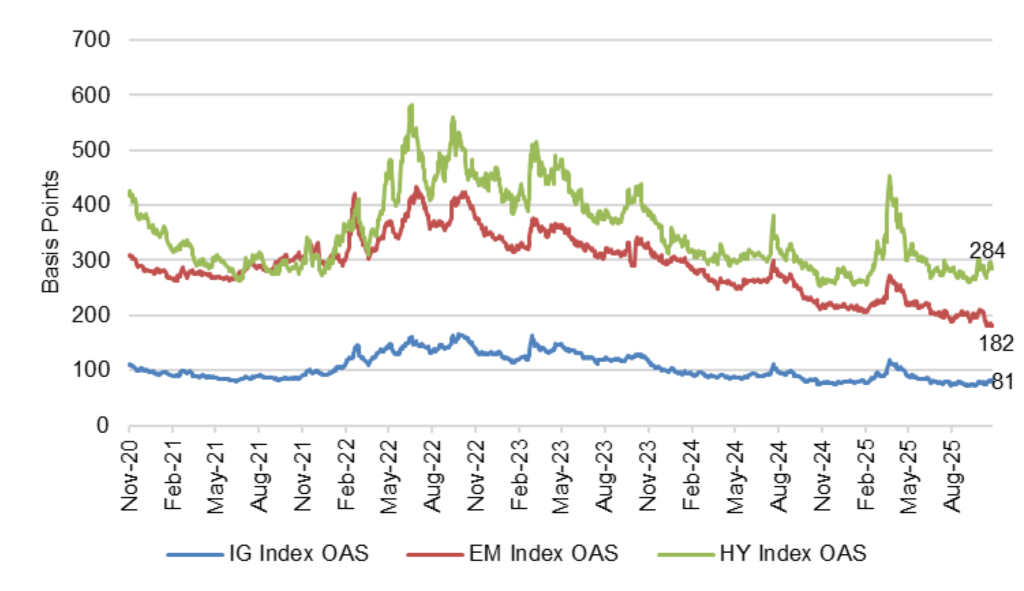

It is easy to see the sources of confidence. Spreads in most credit markets by almost any measure are tight (Exhibit 1). The investment grade market is at the 13th percentile of its 5-year range, emerging markets at the 1st percentile and high yield at the 16th percentile. These are not the kinds of spreads associated with systemic crisis including the 2008 financial crisis, the 2011 eurozone crisis, the energy crash of 2014-2016, the 2020 onset of pandemic or even Liberation Day. However, it is also true that credit spreads historically do a poor job of anticipating default and other of the worst outcomes of credit fundamentals. They do a better job reflecting risk premiums for credit and liquidity. Those premiums clearly are low.

Exhibit 1: Credit spreads show no obvious signs of concern about systematic risk

Source: Bloomberg, Santander US Capital Markets

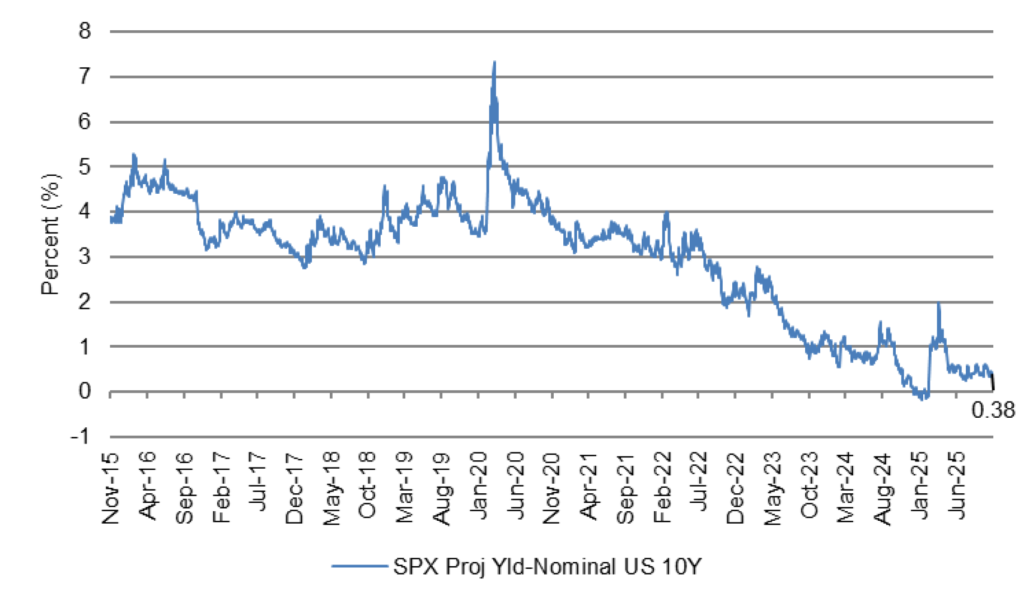

Equity markets, which do a better job of anticipating poor credit fundamentals, are exuberant. Analysts’ earning estimates for the S&P 500 over the next year are equivalent to a 4.53% yield, only 38 bp higher than the yield on the US 10-year Treasury (Exhibit 2). The spread for the Russell 2000, capturing prospects for much smaller companies, is only 46 bp. Those spreads imply expectations of significant earnings growth and equity price appreciation, both credit positives.

Exhibit 2: S&P 500 projected 1-year yield only top the 10-year Treasury by 38 bp

Source: Bloomberg, Santander US Capital Markets

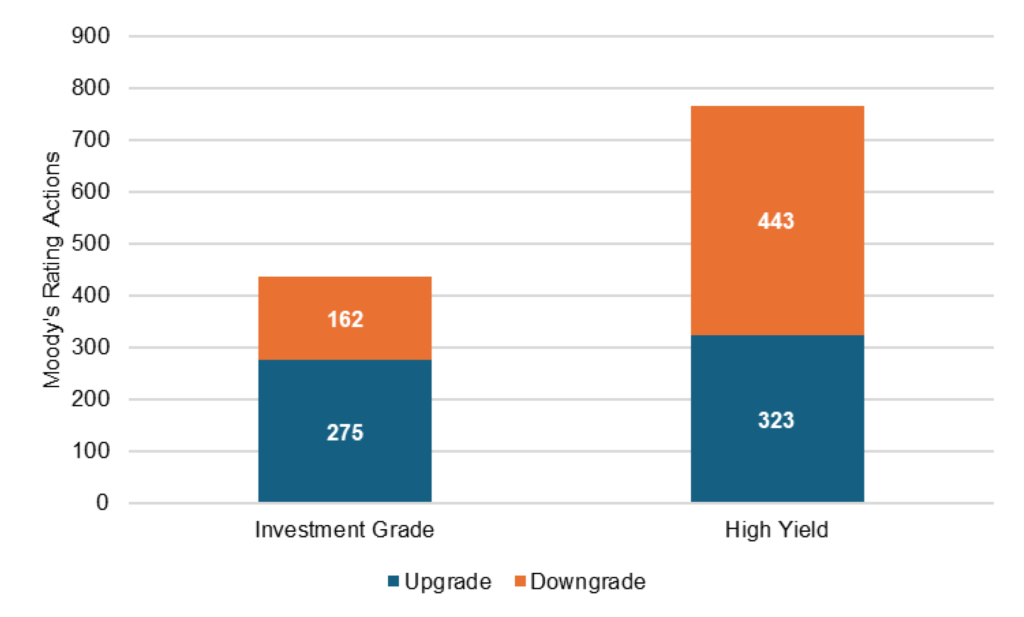

Direct measures of fundamental credit are less enthusiastic, more mixed. Things for larger, investment grade companies look relatively good. Moody’s has taken 437 rating actions on investment grade companies this year, with 63% upgrades and 37% downgrades. For smaller, more leveraged high yield companies, Moody’s is flashing more caution. Out of 766 rating actions, 42% involve upgrades and 58% downgrades (Exhibit 3).

Exhibit 3: More up than downgrades for investment grade but not high yield

Source: Bloomberg, Santander US Capital Markets

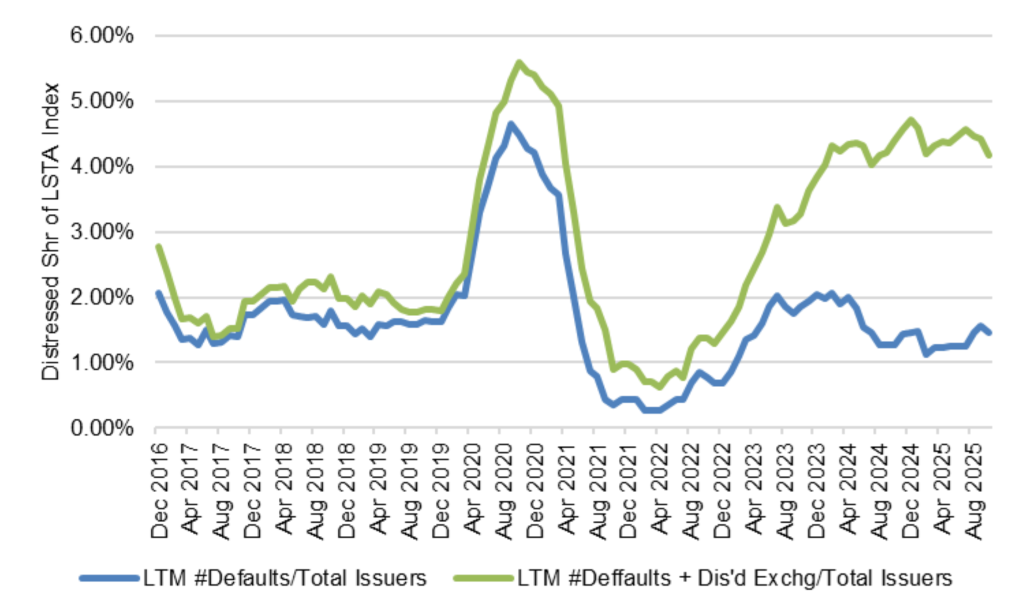

Weakness in smaller or more highly leveraged companies also shows up elsewhere. The LSTA publishes indices of both payment delinquencies in its index of leveraged loans and the incidence of distressed exchanges, transactions where the company in trouble restructures its debt to avoid default. The combined measure of delinquency and distressed exchange has run above 4% for nearly two years, slightly below the pace immediately following the 2020 onset of Covid (Exhibit 4). That corresponds roughly to the Fed’s path to higher rates, raising the interest expense on these leveraged balance sheets largely funded with floating-rate debt. That suggests steady credit stress.

Exhibit 4: The LSTA index distressed share has topped 4% for nearly two years

Source: PitchBook, Santander US Capital Markets

Tight spreads on credit and mixed fundamentals arguably fit together only one way: investors are getting paid little to take fundamental risk in smaller, more leveraged credits and paid mostly to sell liquidity. It would be wrong to interpret tight credit spreads as a sign that fundamentally all is good. It is broadly true for larger companies or wealthier households, but not for the rest.

While investors in Tokyo and elsewhere have had their eye on First Brands and other names, the better focus would be on liquidity. There have been some bumps there lately, with repo rates trading above the upper target range on fed funds. The Fed’s standing repo facility has helped relieve the pressure, but liquidity in US markets clearly has moved from abundant to ample. The Fed is monitoring liquidity closely and has plenty of incentives to keep the machinery well oiled. But there may still be bumps. That is probably the biggest foreseeable risk to current spreads in credit. If liquidity slips, there will be more unhappy families in the less liquid corners of credit, all possibly unhappy in the same way.

* * *

The view in rates

Fed funds futures for the end of 2025 now price less than a 50% chance of another cut. That lines up with my colleague Stephen Stanley, who has not cut as his base case. He also continues to expect no more cuts through the first half of 2026 and possibly through the full year. Inflation is still running above the Fed target and labor markets are soft but not recessionary, making it hard for the Fed to cut very much.

Swap spreads starting in September have widened significantly in longer maturities and continued widening through October. The best theories give credit to a surge in tariff revenue to reduce Treasury supply with some help from hedge fund buying to add to Treasury demand. The Supreme Court on November 5 heard arguments challenging the ability of the president to impose broad reciprocal tariffs under the International Emergency Economic Powers Act, the authority used in April. The Supreme Court seemed receptive to the challenge. A ruling later this year or early next against the president could tighten longer swap spreads and bear steepen the curve.

Key market levels:

- Fed RRP balances settled on Friday at $1.5 billion, down $3.5 billion from a week ago, reflecting better lending opportunities in other repo markets

- Setting on 3-month term SOFR traded Friday at 385 bp, up 1 bp in a week

- Further out the curve, the 2-year note traded Friday at 3.61%, up 5 bp in the last week. The 10-year note traded at 4.13%, up 3 bp in the last week

- The Treasury yield curve traded Friday with 2s10s at 54 bp, steeper by 1 bp in the last week. The 5s30s traded Friday at 102 bp, steeper by 1 bp

- Breakeven 10-year inflation traded Friday at 230 bp, up 1 bp in the last week. The 10-year real rate finished the week at 183 bp, up 3 bp in the last week

The view in spreads

Credit markets remain nervous. Surging private debt, surging bank financing of private debt and the complexities of managing and monitoring the risk have led investors in riskier names to start re-underwriting some of the risk. The case for investment grade risk remains good: Start with an easier Fed, add good fundamentals for bigger business and higher income households, lower volatility, continuing inflows to credit buyers and relatively heavy Treasury supply. Those tides continue to flow. The Bloomberg US investment grade corporate bond index OAS traded on Friday at 83 bp, wider by 1 bp in a week. Nominal par 30-year MBS spreads to the blend of 5- and 10-year Treasury yields traded Friday at 128 bp, wider by 5 bp in the last week. Par 30-year MBS TOAS closed Friday at 26 bp, wider by 2 bp.

The view in credit

Bank lending to non-bank financial institutions has expanded at an extraordinary pace in the last few years, raising the possibility that lending has outstripped experience and infrastructure for underwriting and monitoring. The risk may be coming home to roost. This follows the news around Tricolor Holdings, in the business of selling used cars to subprime borrowers and financing them, now accused of fraud against warehouse lenders. The firm filed bankruptcy on September 9. Serious delinquencies in FHA mortgages and in credit cards held by consumers with the lowest credit scores have been accelerating. Consumers in the lowest tier of income look vulnerable, and renewed student payments and cuts to government programs should keep the pressure on. The balance sheets of smaller companies show signs of rising leverage and lower operating margins. Leveraged loans also are showing signs of stress, with the combination of payment defaults and liability management exercises, or LMEs, often pursued instead of bankruptcy, back to 2020 post-Covid peaks. If persistent inflation keeps the Fed at higher rates, fewer leveraged companies will be able to outrun interest rates, and signs of stress should increase. LMEs are very opaque transactions, so a material increase could make important parts of the leveraged loan market hard to evaluate.