The Big Idea

Labor market steady

This material is a Marketing Communication and does not constitute Independent Investment Research.

In the absence of government economic data, it is more difficult than usual to get a precise read on the state of the labor market. Nevertheless, as Chair Powell has noted several times, there are a number of private data series that offer insight. Two of my favorites strongly suggest that the labor market is broadly in a similar place as it was before the federal government shut down at the beginning of October.

Hiring and firing

There are two halves to the churn in the labor market. At any given point in time, some firms are adding workers while others are trimming staff. In fact, the turnover in the labor market is typically massive, a fact that is made clear by the Labor Department’s JOLTS data. For example, in August, when payroll jobs increased by a miniscule 22,000, the JOLTS report revealed that there were 5.126 million hires and 5.111 million separations.

In any case, to understand the direction of the labor market, it is necessary to know what is going on with both new hires and separations. Typically, the two mirror each other (in opposite directions). When the labor market is robust, hiring accelerates and layoffs fall. When the labor market is softening, hiring slows and layoffs rise.

This year has brought an unusual situation. Hiring has been slowing, but layoffs remain historically low. Many have referred to the current environment as a “no hire, no fire” labor market. I see this as a reflection of temporary business caution brought on by policy-related uncertainty. Many firms have indicated that they are holding off on making investment and staffing decisions until they have a clearer read on tariffs and other policy parameters. This is a logical explanation for the relatively low churn on both sides of the labor market equation. The good news is that I would expect policy-related uncertainty to dissipate relatively soon, a key reason why I look for the labor market to firm as we move into 2026.

Hiring side

With the payroll employment numbers unavailable, my favorite private data on the hiring side is the Indeed Job Postings index. This gauge uses Indeed’s extensive job search site to track the number of available positions. Unlike the JOLTS jobs openings series, this measure does not gyrate wildly from month to month (Exhibit 1). After spiking during the post-Covid labor shortage, job postings have steadily declined and are currently running just marginally higher than immediately before the pandemic.

Exhibit 1: Indeed Job Postings Index

Source: Indeed.

After peaking in the spring of 2022 at around 160 (the index is set to 100 on February 1, 2020, the pre-Covid benchmark), the gauge declined sharply in late 2022 and 2023. The index level sank from 144 at the end of 2022 to 122 at the end of 2023. Over the course of 2024, the gauge slipped by another 10 points to 112.

Focusing on the series for this year through the end of October, the latest readings were just below 102 (Exhibit 2). This means that the index has fallen by about ten index points in ten months, a point per month. That is quite similar to the rate of decline in 2024 as well, suggesting a steady pace of moderation rather than an abrupt downturn in labor demand.

Exhibit 2: Indeed Job Postings Index in 2025

Source: Indeed.

There has been a slight deviation from that trend in recent months. Job postings actually inched up in July and August but have resumed their downtrend since then. The pace of decrease over the most recent two months is a modest acceleration from the well-established trajectory through mid-2025, dropping about 3.5 points in two months. This could be a reversal of the uptick in the summer, or it could be evidence of a small deterioration in labor market conditions. In either case, it does not reflect a sharp weakening in the demand for workers.

Separations side

While the weekly unemployment claims reports, which are released by the Department of Labor, are another victim of the federal government shutdown, along with the unemployment rate, we still have a makeshift version of the claims figures. The tallies are actually compiled by the various state Labor Department agencies and reported up to the federal government. During the shutdown, the federal agency has continued to offer weekly updates on the state-by-state figures, though later than the usual Thursday 8:30am weekly release. Economists can sum up the state figures, make assumptions for any missing observations, and develop estimates for the national readings.

These estimated numbers offer very positive news. Initial claims just prior to the shutdown had averaged 225,000 in the most recent two weeks. This pace was quite consistent with the year-to-date average of 228,000. For reference, initial unemployment claims averaged 223,000 in both 2023 and 2024. Thus, the story overall for quite some time has been stability.

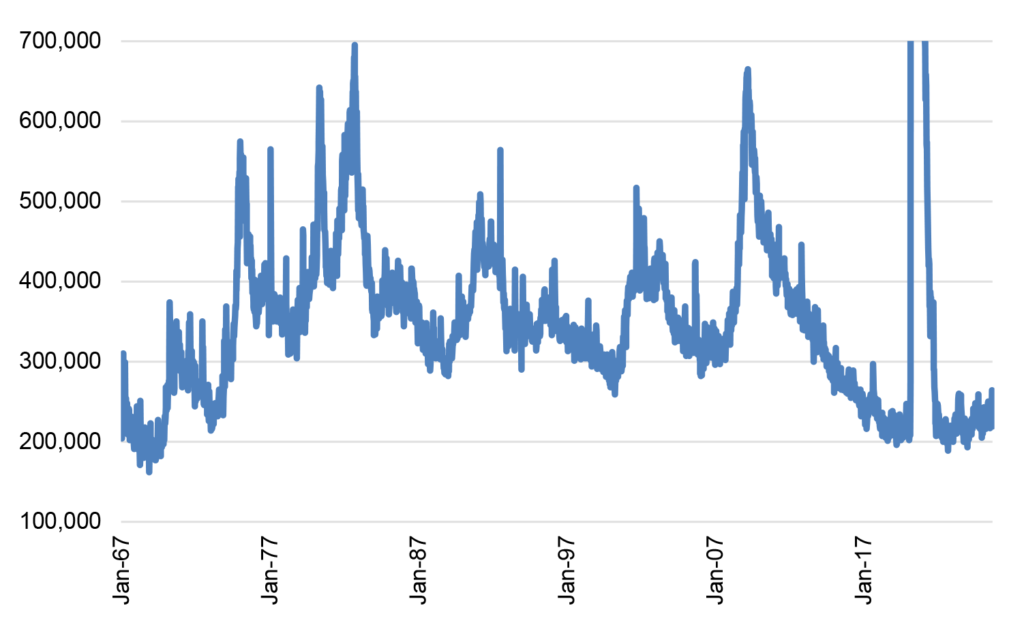

Given how long the number of new filers has been running in this range, it would be easy to lose sight of how unusually low that pace is. The long-term history of initial unemployment claims puts things in context (I cut off the top of the range during the pandemic, when jobless claims spiked to over six million) (Exhibit 3). The recent range is near the lowest level seen since the late 1960s, even more remarkable in light of how much the size of the workforce has expanded versus 60 years ago. Thus, the assessment would be that the pace of layoffs has been steady at a historically low rate.

Exhibit 3: Initial unemployment claims

Source: Labor Department.

Based on data through the week of October 25, my estimates for the six initial claims readings since the shutdowns are 224,000, 234,000, 220,000, 231,000, 218,000, and 224,000. The average of those six readings is a familiar 225,000. Despite all of the talk generated by corporate layoff announcements recently, the best and most timely data that we have suggest that actual layoffs have not ticked up in a meaningful way. This is all the more impressive considering that the shutdown itself could have been expected to produce a rise in private sector furloughs, as many government contractors and others dependent on federal funding are likely not getting paid and thus may have been forced to temporarily lay off some of their workers.

Conclusion

There are clearly downside risks in the labor market at the moment, as Chair Powell and most other Fed officials have emphasized. If policymakers were nervous before, their level of concern undoubtedly has ratcheted up given the dearth of information due to the federal government shutdown. While financial market participants are desperate for fresh data and have latched on to a variety of indicators that have a poor track record of accuracy, I would argue that the combination of the Indeed Job Postings index and the weekly initial unemployment claims figures are sufficient to give us at least a rough sense of how labor market conditions are evolving. These two measures suggest that not much has changed over the past six weeks. While this is not great news, as the labor market was tepid at best prior to the shutdown, it should help to allay the worst fears of policymakers and financial market participants alike.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.