The Long and Short

Assessing the landscape for non-bank hybrids

Dan Bruzzo, CFA | October 3, 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

Issuance of non-bank junior subordinated hybrid securities has gained increased prominence over the past two years. Investor appetite for higher yields has fueled this trend, enabling a broader cross section of issuers to tap this segment of the market. As corporate bond spreads have tested historically tight levels, more investors have moved down in structure and to add commensurate spread and yield, creating opportunities for issuers looking to raise debt with partial equity credit. A detailed breakdown of these securities can lend visibility into how investors are assessing value and provide a roadmap to identifying relative value.

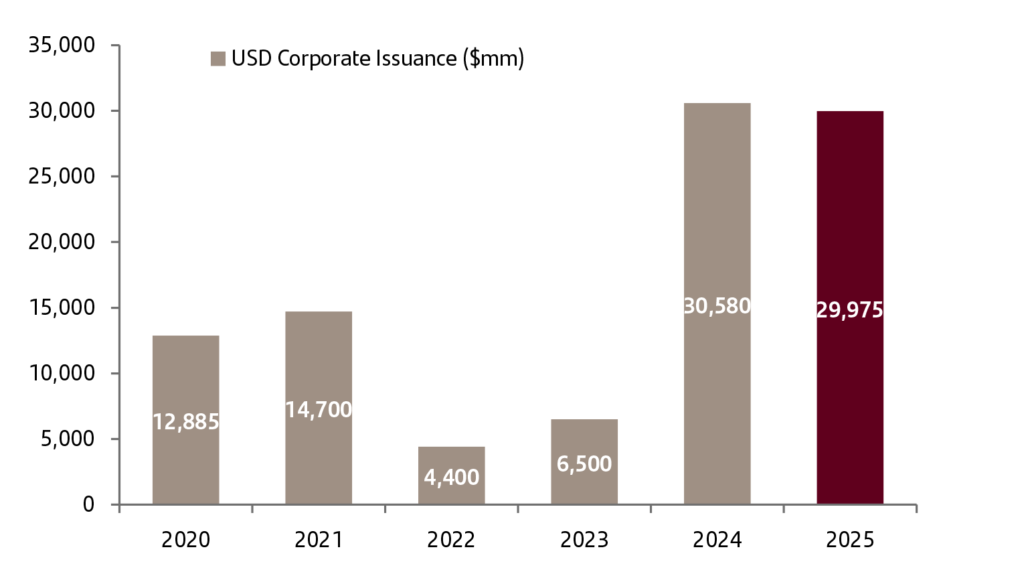

What was once a niche market with only a few issuers has become a more liquid and well-defined segment of the primary and secondary bond markets. Over the past two years, roughly 90 new issues have priced in the investment grade and ‘BB’ primary markets for non-bank hybrids, more than doubling the number of bonds trading in the overall universe. Volumes in 2025 are also on pace to surpass last year’s record (Exhibit 1).

Exhibit 1: Corporate hybrid issuance by year

Source: Santander US Capital Markets LLC, Bloomberg LP, Informa

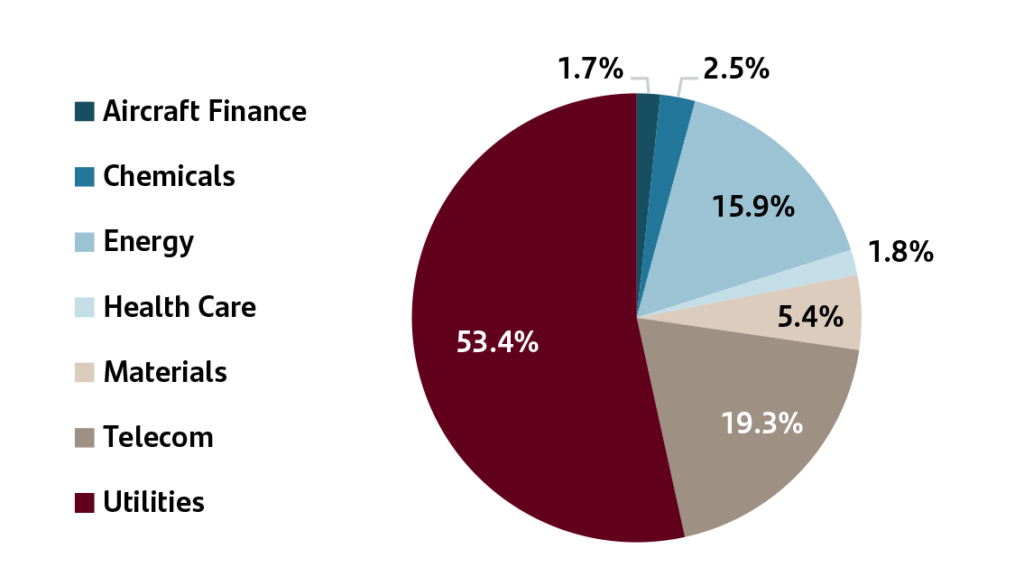

As recently as this week, the market saw multiple non-bank hybrids price in new issue: CenterPoint’s CNP 5.95% 30NC5s and Dominion’s tap of two existing deals, D 6.0% 30NC5s and D 6.2% 30NC10s. All three issues were well subscribed (3.5x covered orderbooks) with modest new issue concession (5-10 bp) to the secondary market. What was once a structure that was primarily exclusive to utility and natural gas companies (away from banks and financials) has expanded vastly to include much larger segments of the market, including energy, telecom, autos and various other industrial subgroups (Exhibit 2).

Exhibit 2: Corporate hybrid issuance by sector

Source: Santander US Capital Markets LLC, Bloomberg LP, Informa

Companies issue hybrids for a variety of reasons that are contributing to their rising popularity across newer sectors in capital intensive industries. The junior subordination helps preserve credit ratings for the issuer’s other senior unsecured debt securities. Partial equity credit also presents an opportunity to raise capital without as significant an impact to overall balance sheet leverage. Meanwhile, the tax treatment of interest payments still remains beneficial to the issuer. The call structures provide an opportunity for issuers to raise long-term capital while managing interest rate risk as well, while investors in the securities are compensated for that extension risk.

As the sector has seen broader acceptance and engagement from corporate bond investors, and spreads have moved tighter overall, there increasingly appears to be less credit differentiation among issuers when valuing securities. Senior/sub premiums have more recently pierced the mental barrier of 100 bp. For example, the Dominion tap on the NC10 structure was roughly 90 bp to seniors. As a result, even more of the perceived value of the securities has become of a function of structure versus credit quality. Since late 2024, coupon floors protecting investors from extension risk by guaranteeing minimum reset rates have become an increasingly popular feature among issuers to draw more interest from perhaps less traditional buyers of these securities. Those floors are a major component of valuation, as extension risk and back-end floating spread have historically been a critical element of pricing securities in the secondary market.

Comparing junior subordinated hybrid securities to comparable senior bullets of the same or similar issuers is one of the more effective ways of identifying relative value and comparing how the market perceives one hybrid relative to another. The following six exhibits break down the market by ratings (investment grade and ‘BB’) and call periods to identify how each security trades relative to its commensurate senior bullet security as close to the call date as possible. Not every security has a relevant comparable security, but the vast majority are shown. Moody’s and S&P typically rate junior subordinated hybrids one notch below seniors, while Fitch uses a two-notch differentiation.

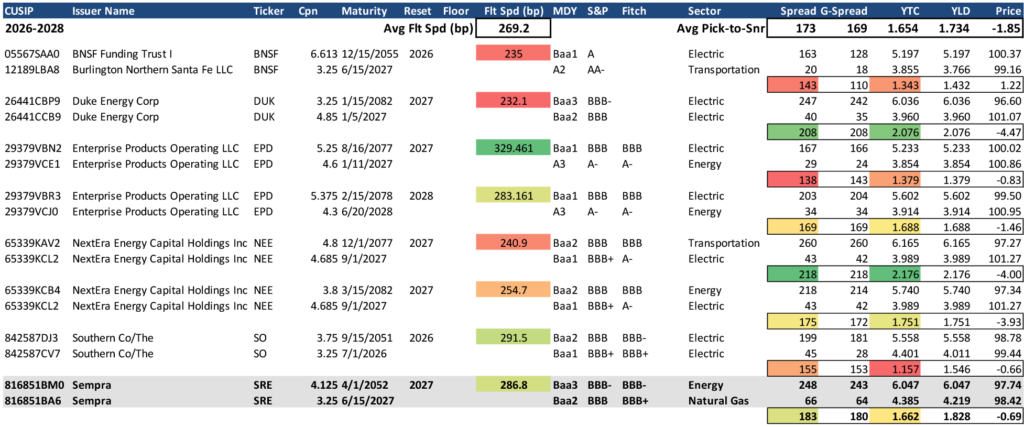

Exhibit 3 demonstrates investment grade issuers with aged-vintage outstanding hybrids with call dates between 2026 and 2028. The color scale in the middle indicates how the back-end floating rates compare to the other bonds in group, with the highest spread and most call protection depicted in green and the lowest in red. Similarly, on the right side of the study, there are another two color scales that depict the spread and yield-to-call picks available relative to senior bullet securities. The greater spread/yield picks are depicted in green with the lower in red. Not surprisingly, higher call protection generally translates to lower spread/yield picks relative to bullets. Ideal valuation appears to be where moderate call protection (light green to yellow) coincides with the most attractive spread and yield compensation. Among this group with approaching call dates, the SRE 2052s (callable 2027) with a 286.8 bp back-end spread are highlighted as offering attractive valuation relative the rest of the bonds presented.

Exhibit 3: Aged vintage investment grade non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

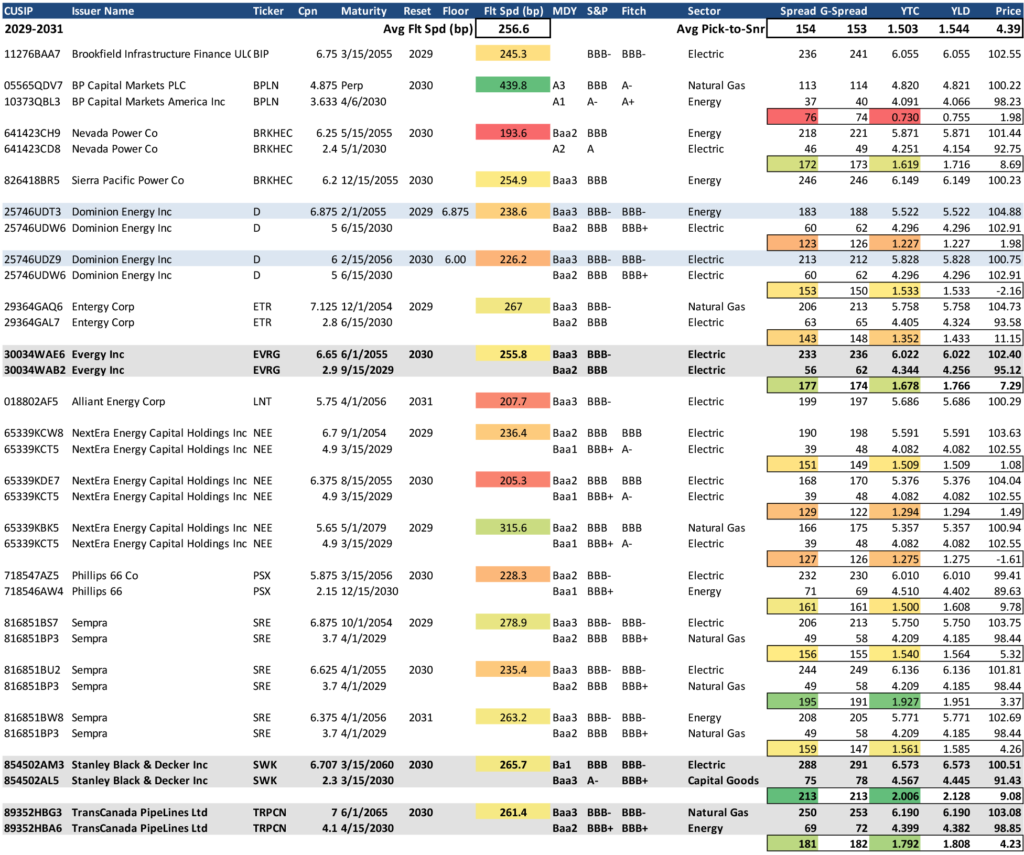

Exhibit 4 lists investment grade hybrids with roughly 5-year calls (2029-2031) relative to similar 5-year bullet senior securities. This represents the largest segment of the investment grade hybrid universe. The recent Dominion issues mentioned above are highlighted in blue to identify coupon floors on the back-end. Among this group, bonds highlighted that appear to offer good valuation versus seniors relative to call risk include:

- EVRG ‘55s (callable 2030) with a 255.8 bp back-end spread

- SWK ‘60s (callable 2030) with 265.7 bp back-end

- TRPCN ‘65s (callable 2030) with 261.4 bp back-end

Exhibit 4: Five-year call investment grade non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

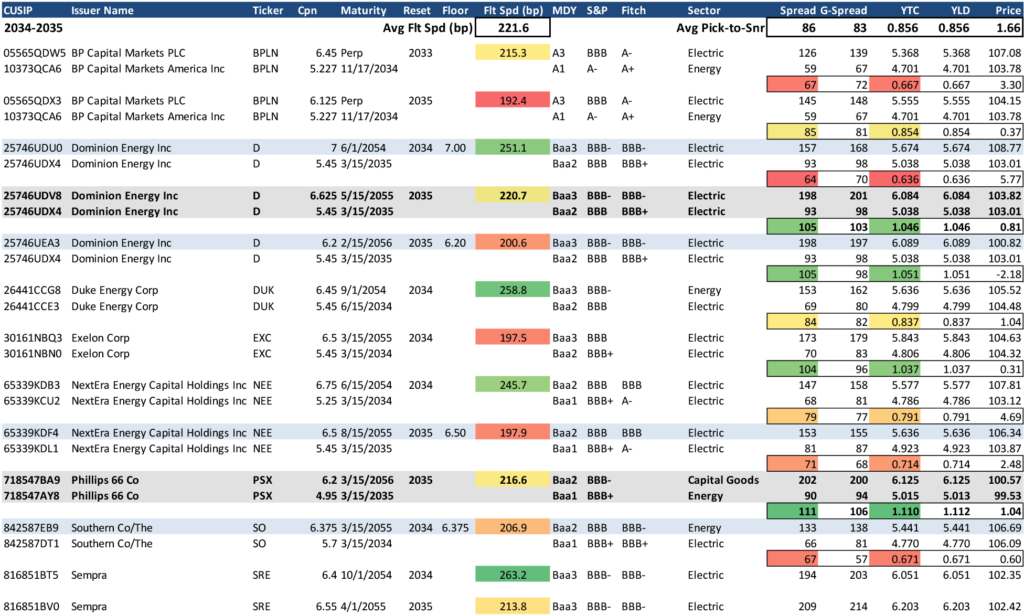

The last investment grade segment in Exhibit 5 lists securities with roughly 10-year calls (2034-2035) relative to similar 10-year bullet senior securities. Once again, the recent issues with coupon floors on the back-end are highlighted in blue. Among this group, bonds highlighted that appear to offer ideal valuation versus seniors relative to call risk include:

- D ‘55s (callable 2035) with 220.7 bp back-end

- PSX ‘56s (callable 2035) with 216.6 bp back-end

Exhibit 5: Ten-year call investment grade non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

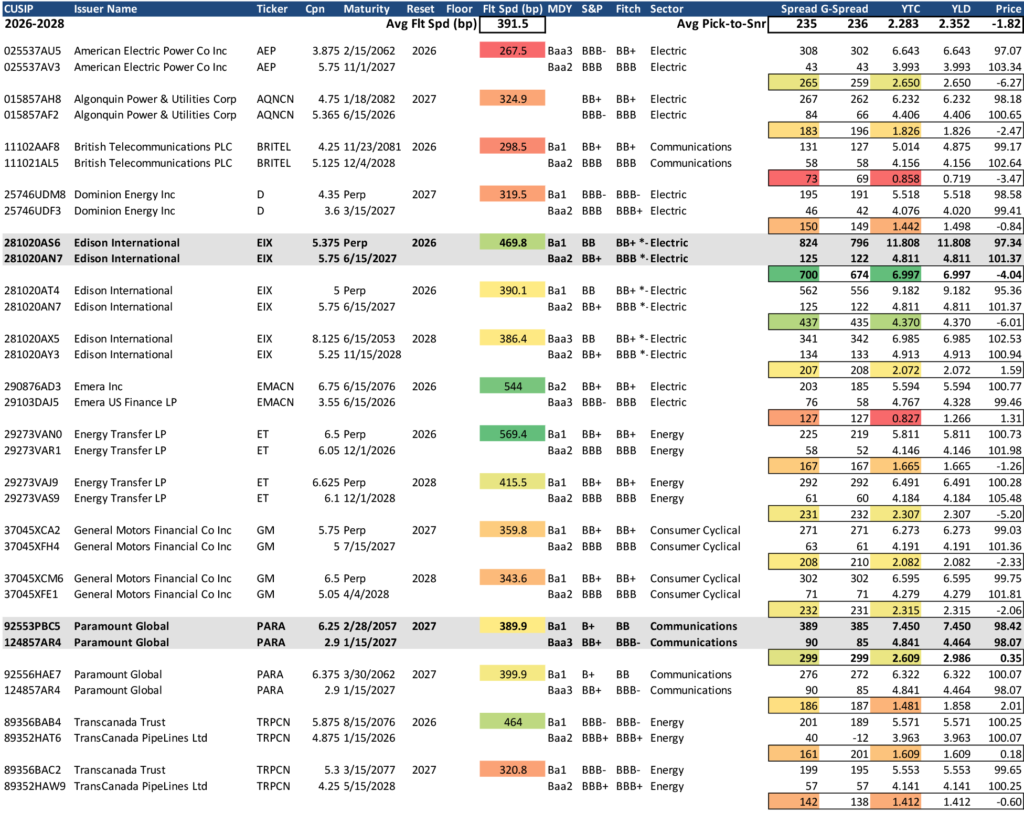

The next group of securities in Exhibit 6 illustrates ‘BB’ hybrids with earlier vintages and upcoming calls (2026-208) relative to similar bullet senior securities. Again, given Fitch’s two-notch differentiation, several securities that are rated low-‘BBB’ by Moody’s and S&P drop into this category. Among this group, bonds highlighted that appear to offer good valuation versus seniors relative to call risk include:

- EIX Perps (callable 2026) with +469.8 bp back-end

- PARA ‘57s (callable 2027) with +389.9 bp back-end

Exhibit 6: Aged vintage ‘BB’ non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

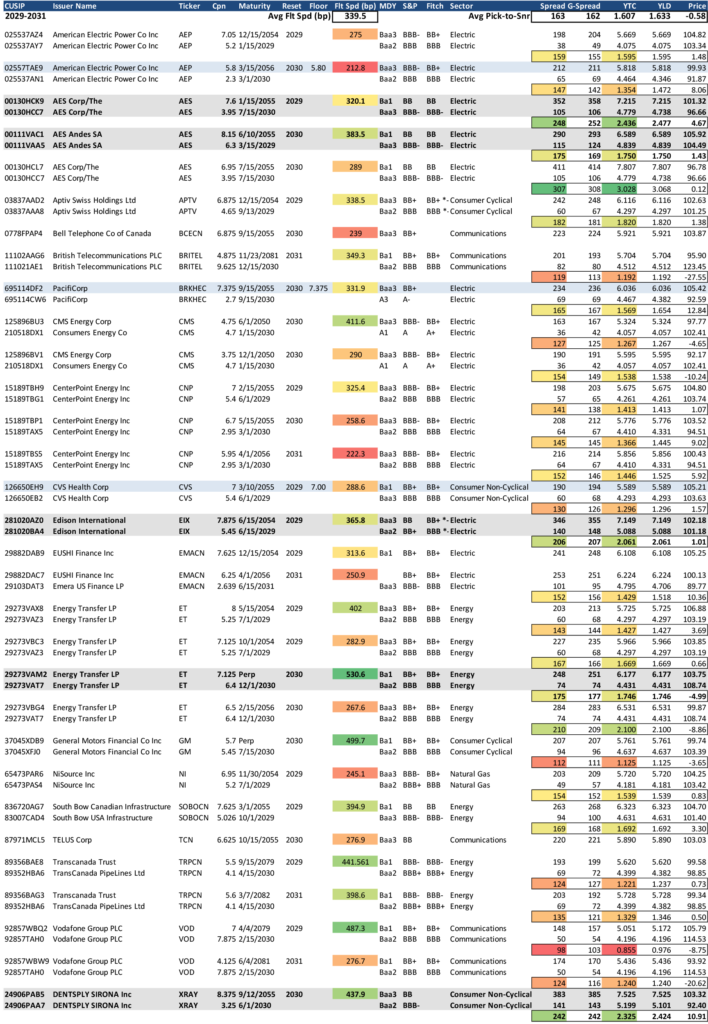

Exhibit 7 lists ‘BB’ hybrids with roughly 5-year calls (2029-2031) relative to similar 5-year bullet senior securities. This represents the largest segment of the of the entire non-bank hybrid universe. More recent issues with coupon floors on the back-end are highlighted in blue. Among this group, bonds highlighted that appear to offer good valuation versus seniors relative to call risk include:

- Both AES ‘55s (callable 2029 and 2030) with back-ends of 320.1 and 383.5 bp

- EIX ‘54s (callable 2030) with 365.8 bp back-end

- ET Perps (callable 2029) with 530.6 bp back-end

- XRAY ‘55s (callable 2030) with 437.9 bp back-end

Exhibit 7: Five-year call ‘BB’ non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

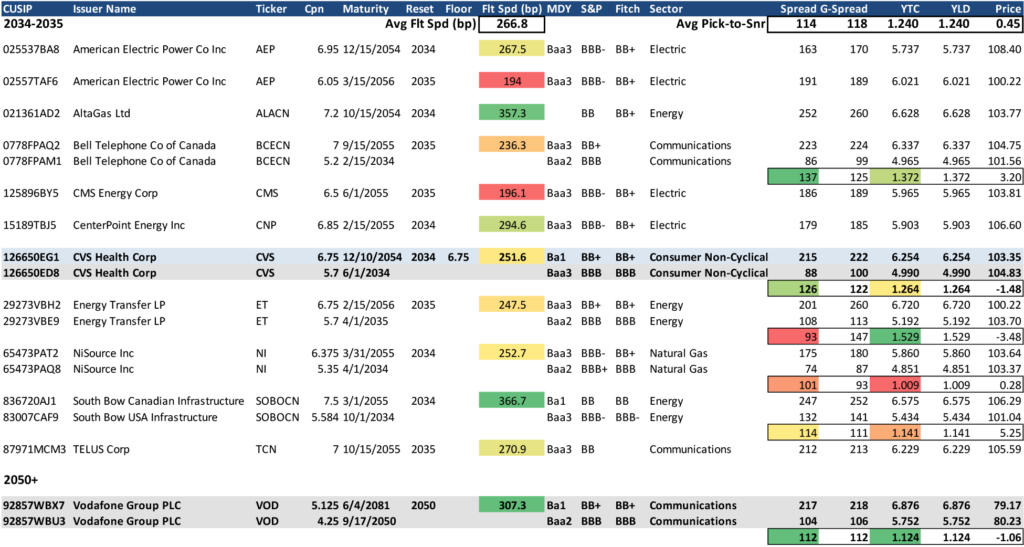

The last ‘BB’ segment in Exhibit 8 lists securities with roughly 10-year calls (2034-2035) as well as one roughly 25-year call relative to similar bullet senior securities. Once again, the recent issues with coupon floors on the back-end are highlighted in blue. Among this group, bonds highlighted that appear to offer good valuation versus seniors relative to call risk include:

- CVS ‘54s (callable 2054) with +251.6 bp back-end and 6.75% cpn floor

- VOD ‘81s (callable 2050) with +307.3 bp back-end

Exhibit 8: Ten-year and longer call ‘BB’ non-bank hybrids vs senior bullets

Source: Santander US Capital Markets LLC, Bloomberg/TRACE YAS price indications only

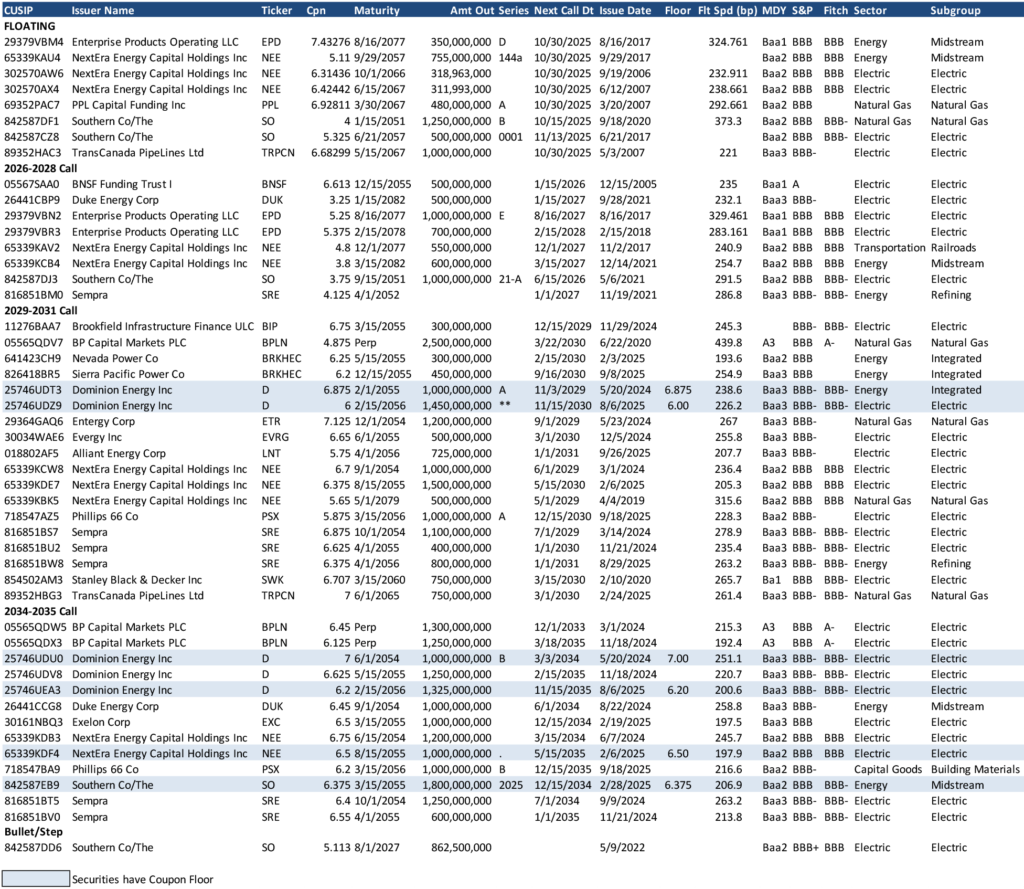

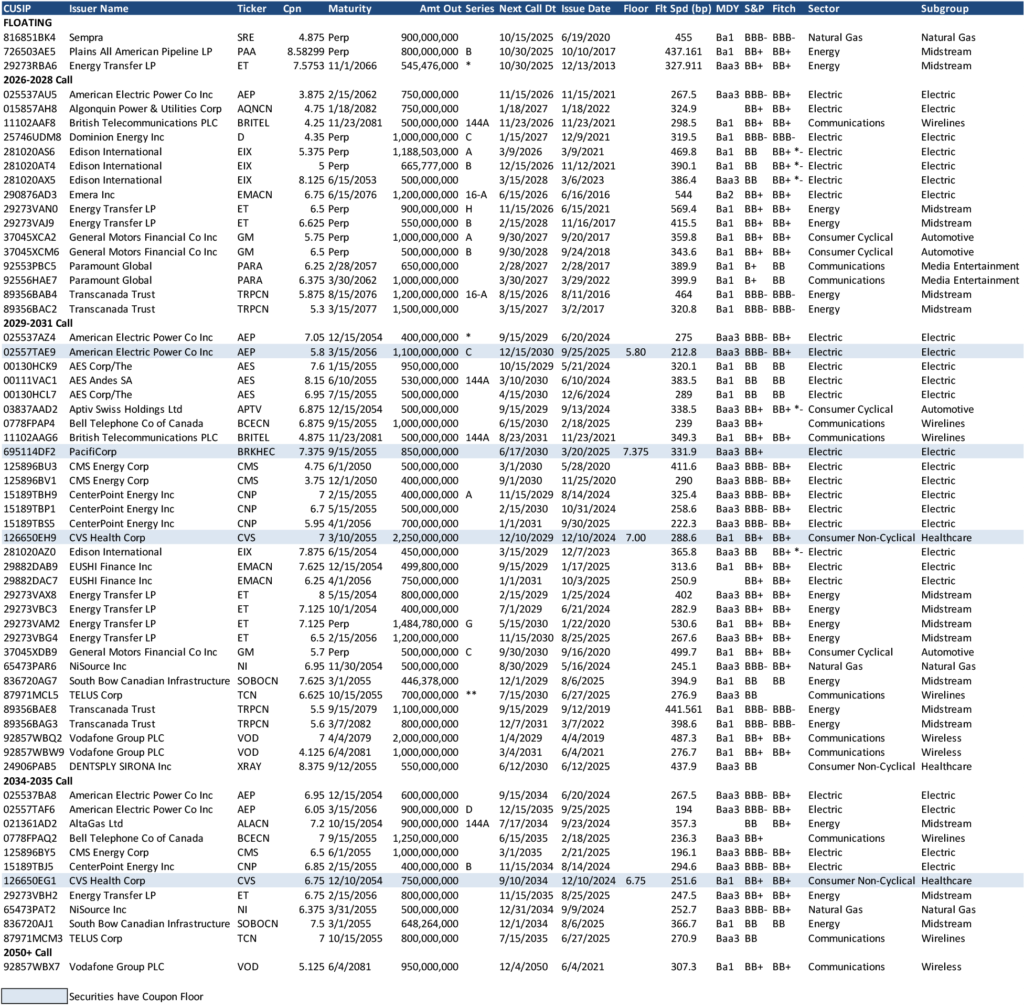

Appendix: Universe of IG and BB-rated Non-Bank Hybrids

Exhibits 9 and 10 below list the universes of non-bank hybrid securities separated into the investment grade and BB-rated markets. While not every hybrid security outstanding is presented, these represent the most likely tradeable group of bonds for investors targeting the segment. The bonds are organized by their call structures and listed in alphabetical and order of duration. Sectors and subgroups are included to enable investors to identify trends among similar issuers. The issues that include the more recently popularized floor features are highlighted in blue.

Exhibit 9: Universe of investment grade non-bank hybrid securities

Source: Santander US Capital Markets LLC, Bloomberg LP

Exhibit 10: Universe of ‘BB’ non-bank hybrid securities

Source: Santander US Capital Markets LLC, Bloomberg LP