The Big Idea

Neutral policy and the Taylor Rule

Stephen Stanley | September 26, 2025

This material is a Marketing Communication and does not constitute Independent Investment Research.

I noted a few weeks ago the wide array of views within the FOMC on the level of the neutral rate. The September FOMC dot projections emphasized this point, and the most recent wave of public appearances underscores how central this has become in the current policy debate. It is time to add a more structured perspective on the stance of monetary policy using a few different specifications of the Taylor Rule. The bottom line is that there is no obvious objective way to adjudicate the disagreement over the level of the neutral rate, so opinions will continue to vary.

Scattered dot plot

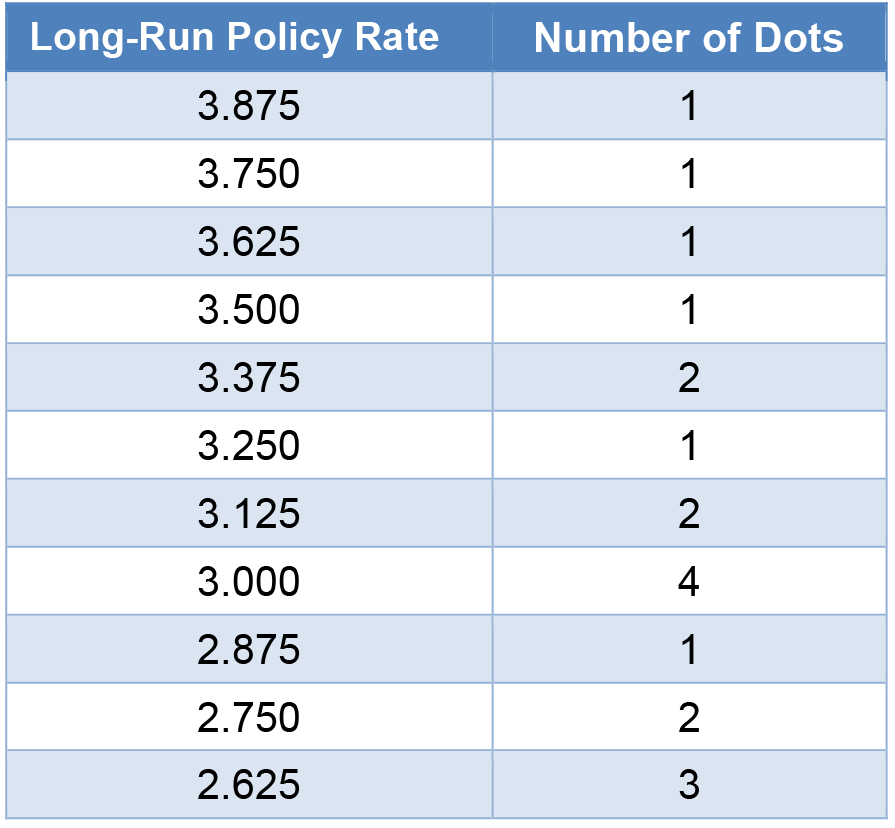

Once a quarter, FOMC participants submit economic and policy projections. The latest edition was published on September 17. In addition to predicting the path of the policy rate over the next few years, officials offer their view of the longer-run policy rate, which is essentially an estimate of the level of the long-run neutral rate.

From the 19 participants, there were 11 different answers submitted in September, spanning from 2.625% to 3.875% (Exhibit 1). The 125 bp range is historically large but not unprecedented. In fact, the range has been unusually wide since around the middle of last year. What makes this disagreement so critical now, as opposed to a year ago, is that the level of the federal funds rate target is approaching the top of the range of estimates of neutral. It made little difference whether a policymaker thought the neutral rate was 2.75% or 3.75% last year when the fed funds rate target was over 5.00%. Everyone at that time agreed that policy was substantially restrictive.

Exhibit 1: September 2025 FOMC longer-run funds rate projections

Source: Federal Reserve.

Now the situation is different. With the funds rate target just above 4.00%, there are some who believe that policy is still restrictive by a wide margin. Over the past week, Governors Bowman and Miran have argued that the current Fed stance is still “very restrictive” (Miran) and that the Fed should be in a rush to lower the funds rate target to return to neutrality.

At the same time, those who see the neutral rate as running in the mid-to-high 3.00%’s see the current policy stance as “only slightly restrictive,” such as Kansas City Fed President Schmid on September 25. Schmid noted that with the labor market still “largely in balance” while inflation “remains too high,” further cuts would not necessarily be wise.

One key distinction in this discussion is the difference between the long-run neutral rate and the appropriate current rate. First, it is important to note that what really matters for the economy is the level of real interest rates, not nominal rates. Policymakers typically plug in 2.00% for inflation in making any long-run calculation, so we can safely assume that the range of estimates for neutrality in nominal terms detailed above amounts to 2.00% inflation plus some assessment of the appropriate long-run real rate for the economy. We will come back to this later, but, for now, consider that if inflation is running well above or well below the Fed’s target, then the proper policy stance at any given point in time should be commensurately higher or lower than the long-run projection. St. Louis Fed President Musalem noted on September 22 that the current policy rate is now at about 4.10%, and he asserted that market pricing for inflation over the next 12 months, using a 12-month inflation swap rate, was 3.30%. This means that the “ex ante real policy rate is 0.80%. This is below the 1.00% median long-run real neutral rate of FOMC participants” as suggested by the 3.00% median longer-run dot minus the 2.00% inflation target.

Put simply, when inflation is running above target, the nominal policy rate has to also be higher to account for the gap (and vice versa). Alternatively, relative to whatever longer-run neutral concept one holds, policy should run more restrictive when inflation is higher and easier when inflation is lower.

Taylor Rule

This brings us to policy rules. Economists have made numerous efforts to offer a systematic framework for quantifying whether policy is too easy or too tight at a particular time. One of the most widely followed policy rules is the Taylor Rule, devised by economist John Taylor in the early 1990s. Taylor’s original goal was to describe how the Fed was setting policy, not to offer a prescriptive ideal, but economists, both inside and outside of the Fed, have for decades used the Taylor Rule as a check on whether monetary policy is being run appropriately.

Hopefully the basic contours of the Taylor Rule are familiar to most readers. In brief, the equation starts with an assumption for the neutral real rate and then adds terms for the unemployment gap (the current unemployment rate minus an estimate of the equilibrium full employment unemployment rate level) and the inflation gap (actual inflation, or, if preferred, expected inflation, minus the Fed’s inflation target). To take a step back, the original Taylor Rule specification (1992) used a GDP gap term rather than an unemployment gap term. Then, in 1993, Taylor offered an alternative framework with the unemployment gap. Subsequently, in 1999, Taylor offered yet another tweak, an equation that doubled the weight on the labor term. This version was favored in the 2010s by then-Fed Chair Yellen, likely because it resulted in a more dovish policy prescription at a time when the unemployment rate was still retreating from its Global Financial Crisis highs.

The Atlanta Fed web site offers a Taylor Rule Utility that shows what various specifications of the Taylor Rule prescribe for policy, allowing for users to tweak the key parameters. I highly recommend spending some time on the page, playing around with various specifications and plugging in different values for key parameters. For now, however, my aim is to offer a couple of straightforward Taylor Rule results as a basic check on the current stance of policy.

One approach is to test what the Taylor Rule says about policy using the FOMC’s own forecasts. In this framework, we use the FOMC’s median forecast for the unemployment rate at the end of the current year compared to the FOMC’s median view of the longer-run unemployment rate to populate the unemployment gap term. We use the FOMC’s median longer-run dot minus the 2.00% inflation target to tease out the real neutral interest rate (in the current instance, 1.00%). And then, the actual most recent 4-quarter change for the core PCE deflator as inflation to calculate the inflation gap.

Note that since we are taking the FOMC’s own median longer-dot as given, the nominal neutral policy rate is, by definition, what the FOMC median thinks it is – 3.00%. Then, policy adjusts over time depending on where the two gap terms are. As you might expect, with inflation running close to a full percentage point above the 2.00% target while the unemployment rate is projected to be only a few tenths above its long-run equilibrium, the Taylor Rule calls for policy to be well above the long-run neutral level.

According to the Atlanta Fed’s Taylor Rule Utility, the 1993 specification calls for a 4.29% funds rate for the current quarter, while the 1999 specification clocks in at 4.16%. So far, so good. This calculation suggests that the FOMC at the moment is operating more or less consistently with the recommendations of the Taylor Rule. The rule also suggests that aggressive rate cuts from here would not be warranted unless economic conditions shift.

We can take this framework forward in time. Using the FOMC median projections for the core PCE deflator at the end of this year (3.10%), the 1999 Taylor Rule would spit out a policy rate of 4.35% at year-end. The result is higher than the current level because inflation is projected to accelerate between now and the fourth quarter. Some Fed officials might argue that the pickup in price increases is being driven by tariffs and should therefore be downweighted or dismissed, which is a legitimate argument. But a mechanical calculation like the Taylor Rule makes no such judgments, which could be said to be a desirable feature or a drawback of the framework, depending on one’s perspective.

Moving further into the future, the median FOMC projections for unemployment and the core PCE deflator for end-2026 yield a Taylor Rule result of 3.80%. Then, by the end of 2027, when inflation is finally anticipated to return roughly to target, the Taylor Rule prescription converges to the FOMC’s perception of neutrality, sliding to 3.05%.

What does this exercise tell us? The median FOMC projection for the funds rate target for end-2025 is about 70 bp lower than the 1999 Taylor Rule result, while the end-2026 median dot is more than 40 bp below the Taylor Rule prescription. For 2027 and beyond, they are roughly equal. This would suggest that the committee is prepared to give only partial weight to the upside inflation misses in 2025 and 2026, presumably writing them off as partly reflecting an extraneous temporary factor, tariffs.

Nonetheless, the median policymaker is not willing to dismiss the high inflation figures entirely. Otherwise, the median dots for 2025 and 2026 would be close to the median neutral level of 3.00%. In essence, the consensus is splitting the difference between the hawks, who would prefer to take the inflation numbers seriously and wait until they recede before dropping rates, and the doves, who want to be at neutral now.

Begging the question

Circling back to the beginning of this Taylor Rule discussion, let me highlight a limit to this mechanical framework. Recall that the first term in the Taylor Rule is the real neutral interest rate. The problem, of course, as I laid out at the start of this piece, is that there is tremendous disagreement among Fed officials and economists generally regarding the true neutral setting. We finessed the question by using the FOMC median as a placeholder, but only four out of 19 FOMC participants actually wrote down 3.00% for neutral this month.

Now, look at the Taylor Rule from Governor Miran’s perspective. He delivered a speech on September 22 in which he made a number of arguments for why the neutral rate is actually moving lower as a result of Trump administration policies. He argued that lower population growth on the back of tighter immigration restrictions, tariff revenues that will lower federal budget deficits, tax cuts, and deregulation should push the neutral real rate down by 100 bp to 120 bp, putting it close to zero. He concluded that the funds rate should be somewhere in the 2.00% to 2.50% range, close to 200 bp below the current level.

Taking everything else as given in the above Taylor Rule calculations, if the neutral real rate is 0% instead of 1.00%, then all of the model results would be 100 bp lower.

In contrast, one FOMC participant at the other end of the spectrum thinks that the real neutral policy rate is 1.875%, implied by 3.875% minus the 2.00% inflation target. If we plug this figure into the Taylor Rule, leaving everything else the same, the prescriptions would all be 87.5 bp higher, pushing the end-2025 result above 5.00% and the end-2026 prescription to about 4.50%.

So, there you have it. The funds rate should be somewhere between 2.50% and 5.00%. I suppose that is not much help! This leads me to end the discussion where I ended my prior piece on this topic and where I started this one. The wide range of views regarding the location of the neutral policy stance is central to the emerging disagreements on the committee. Moreover, as the funds rate gets closer to the range of the longer-run dots, and perhaps soon moves into the upper part of that span, the level of discord within the FOMC may rise further. This could make for a very difficult situation for a new Fed chair to step into next year.