By the Numbers

Weighing in on bank demand for MBS

This material is a Marketing Communication and does not constitute Independent Investment Research.

While steadily declining interest rate volatility has helped tighten MBS spreads recently, many market participants would argue that the next meaningful leg tighter needs more MBS demand from banks. The most likely scenario for that would be a tightening of credit availability, lower rates and a steepening of the yield curve against the backdrop of a weakening economy. Absent that, demand looks likely to be tethered to overall asset growth, as MBS holdings appear to be right-sized in the context of institutions’ balance sheets.

MBS investors have been forced to deal with a new normal over the past two or more years. For years before then, elevated demand for MBS from both the Fed and banks would routinely push spreads tighter, taking total return managers and hedge funds along for the ride. And in dislocated markets, that demand would provide a backstop, limiting how much MBS spreads could widen. Fast forward to the new normal and the Fed is slowly reducing their mortgage holdings by reinvesting pay downs in Treasuries, and depositories have been faced with the stark realization that outsized, negatively convex MBS exposures can be one factor that could force a bank into receivership.

Sizing bank demand historically

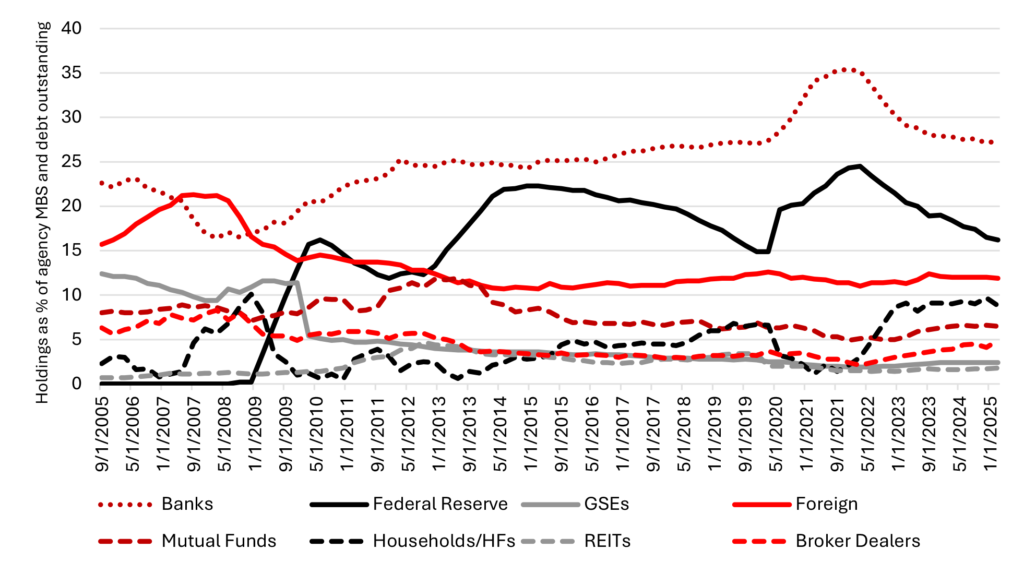

One way to evaluate the current size of banks’ MBS holdings is to look at the support that depository balance sheets have provided to the MBS market historically. At the end of the first quarter of this year, banks held just over 27% of outstanding agency MBS and debt. That reading is consistent with banks’ market share prior to Covid, before surging to a whopping 35% of the outstanding universe in the third quarter of 2021 and remaining there for three quarters (Exhibit 1).

Exhibit 1: Bank support of the MBS universe reverts to pre-Covid levels

Source: Santander US Capital Markets, Federal Reserve Z1 Report

The above suggests that the peak in depository holdings of MBS were an artifact of extremely elevated levels of monetary stimulus coupled with generationally tight levels of credit availability through 2020 and into 2021. Much of the roughly $7.7 trillion in monetary stimulus enacted by the Federal Reserve through the pandemic found its way to bank balance sheets in the form of deposits, as that excess liquidity remained uninvested against the backdrop of heightened economic uncertainty.

That same uncertainty precluded banks from making loans, leaving them in the unenviable position of facing a deluge of deposit inflows with scant few new assets to pair against them to maintain their net Interest margin. In response, banks’ investment portfolios ballooned under the weight of those deposit inflows, suggesting that these elevated levels of bank holdings were episodic and idiosyncratic in nature, and unlikely to be realized again in the near future.

Drivers of growth

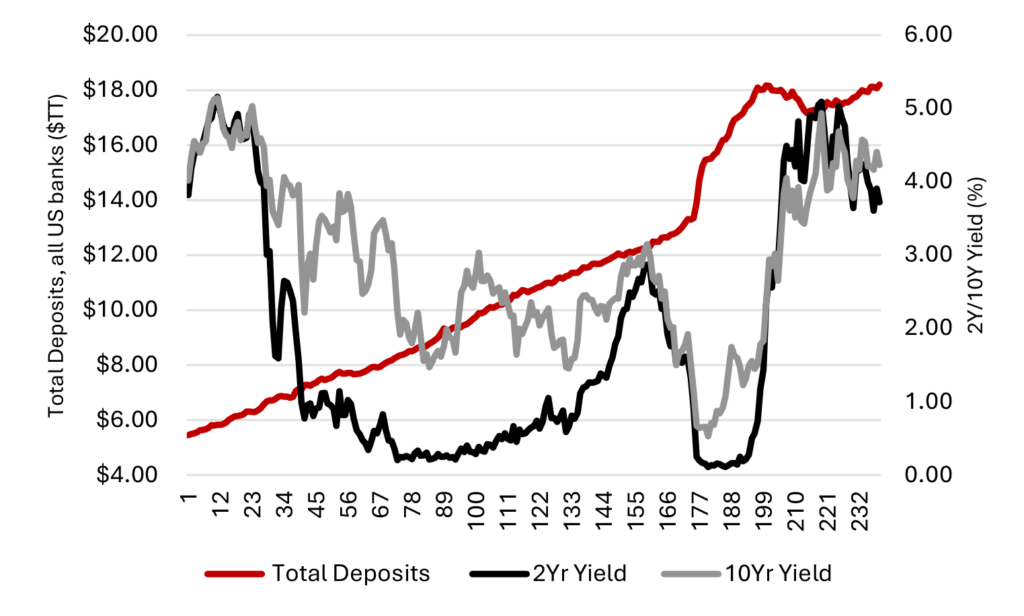

If history suggests that current bank MBS holdings are to some degree ‘right-sized,’ then growth in bank portfolios is likely to come from either net growth of the MBS market, growth in depository balance sheets or some combination thereof. As evident during 2020, balance sheet growth was driven more so by the liability side of the balance sheet. And the longest standing and most consistent predictor of deposit growth has been the negative correlation between the level of rates and the velocity of deposit growth. Said another way, bank deposits tend to grow faster as interest rates are falling and slower when they are rising (Exhibit 2).

Exhibit 2: Bank deposits grow as interest rates fall

Source: Santander US Capital Markets, Federal Reserve H.8

Bank deposits grow as rates fall for a couple of reasons. Most obviously, if benchmark rates are low, the opportunity cost of being uninvested is as well. And both individuals and institutions are more likely to leave funds on deposit at a bank rather than in a money market or mutual fund. Furthermore, low rates are generally consistent with a slowing economy and correlated underperformance in risk assets, another reason deposits both grow and remain sticky in lower rate environments. Given this, the most likely scenario that would drive substantially greater demand from banks for MBS would be a significant economic slowdown that would trigger an aggressive Fed cutting cycle.

Other considerations

There are certainly other factors that could skew bank demand. Lighter touch bank regulations could spur more investment in securities. While changes to leverage ratios and how certain banks account for unrealized losses may be a modest tailwind for bank demand, loosening of the current regulatory framework likely will not trigger a reversion to how banks invested prior to the failures of Silicon Valley Bank and other depositories in the spring of 2023. Those bank failures shed light on how negative convexity on both sides of the balance sheet can leave banks’ duration gaps woefully offsides as assets extend and deposit durations shorten. Those lessons appear to be instilled in banks’ risk culture and shorter duration, more convex exposures appear likely to continue to make up the majority of depository dollars invested in securities. In that vein, recent growth in securitizations of Ginnie Mae ARMs may help spur increased bank demand as ARMs have always been a good fit on bank balance sheets from an asset liability management perspective.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.