The Big Idea

Tariff-related price hikes show up in June

This material is a Marketing Communication and does not constitute Independent Investment Research.

The transmission of tariff hikes to consumer prices has been slow in coming, and the delay has created some complacency in markets. Many participants began to question whether we would see any acceleration at all on the back of higher tariffs after surprisingly benign April and May inflation figures. However, the June price numbers clearly showed the first installment of inflation coming from imported goods. A deep dive into those data suggests the PCE deflator may be more impacted than the CPI.

Imported goods categories

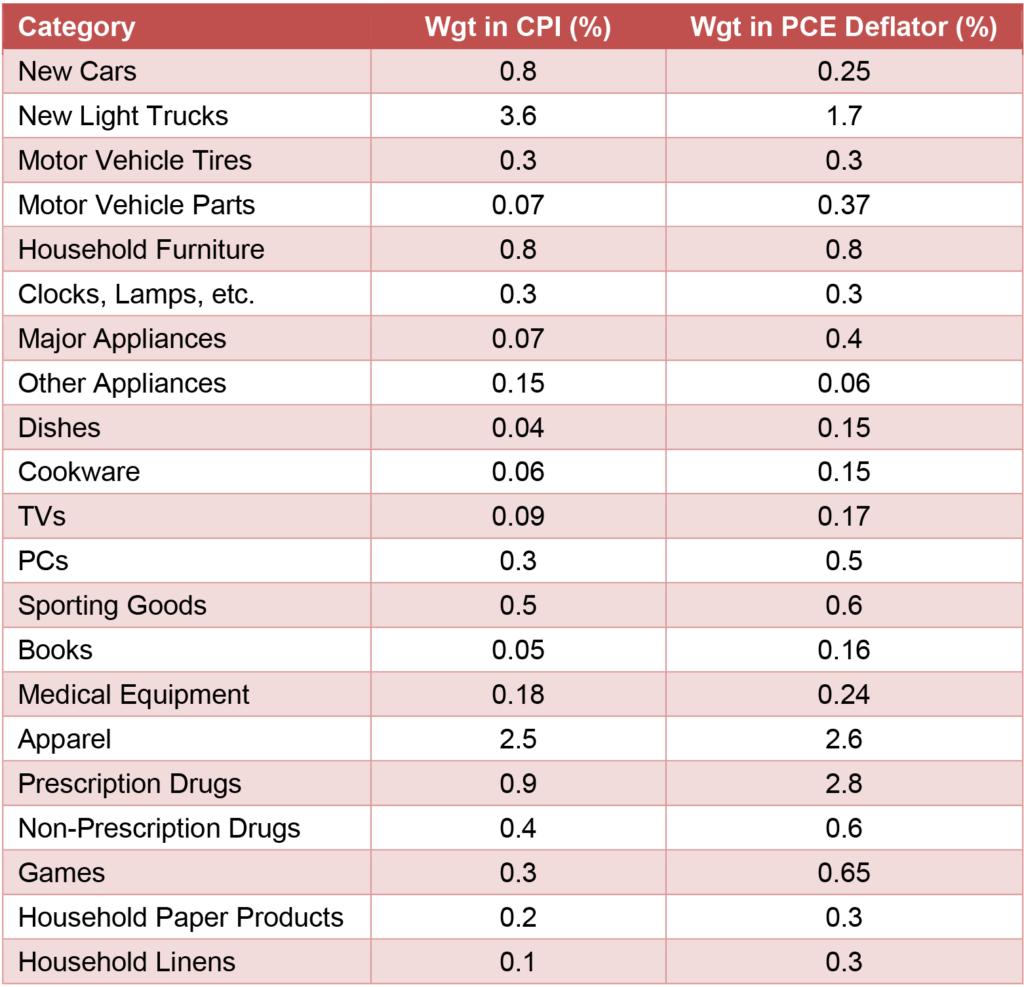

Admittedly, there is a certain amount of interpretation here, but I have singled out 21 items from the price aggregates that I believe include a significant amount of imported goods and are consequently likely to be affected by tariff hikes (Exhibit 1). If anything, an exhaustive list would likely be much longer. In any case, the highlights are motor vehicles and parts, apparel, and a variety of household goods. It is important to highlight each line item’s 2024 weight in the CPI and in the PCE deflator. For example, new cars represent 0.80% of the CPI and 0.25% of the PCE deflator.

Exhibit 1: Imported goods line items and weights in inflation aggregates

Source: BLS, BEA.

The first key insight from this exercise is that this subset of line items carries a larger weight in the PCE deflator than in the CPI. The sum of the 21 weights add up to 11.7% for the CPI and 13.4% for the PCE deflator. Moreover, if we excludes new cars and light trucks, which seem to be a special case, the corresponding weights are even more different, 7.3% for the CPI and 11.5% for the PCE deflator. This means that if the price changes for the line items are roughly equal between the two different inflation measures, the impact from tariffs on the PCE deflator will be larger than for the CPI.

June price changes

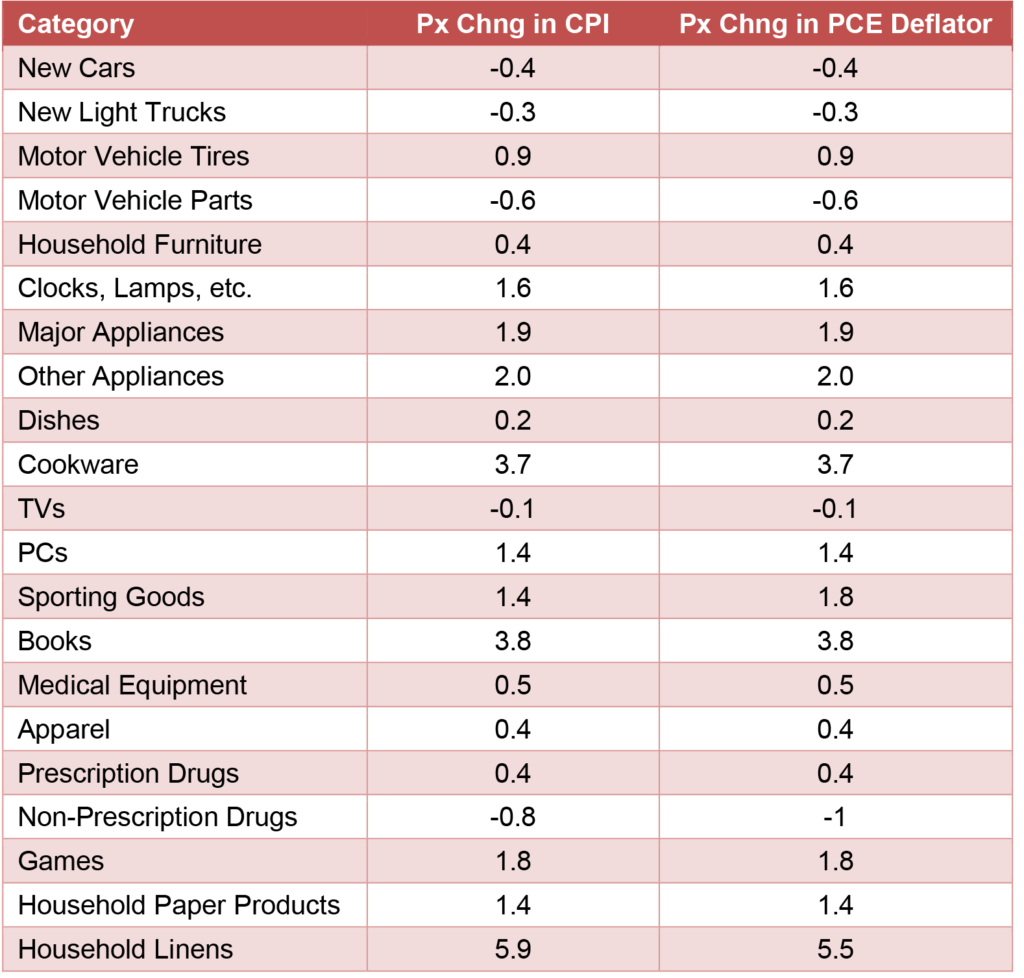

In fact, for most goods items, the CPI price changes in a given month translates directly to the PCE deflator (Exhibit 2). In a few cases, the readings are slightly different, mainly because the translation in some instances occurs at an even lower level of aggregation than I use. For example, I look at apparel as a whole, but the CPI price changes pass through to the PCE deflator at a more detailed level, such as men’s apparel, women’s apparel and so on.

Exhibit 2: June price changes for imported goods line items

Source: BLS, BEA.

June price changes should immediately refute the hypothesis that tariff hikes will have no impact on consumer prices. Ten of the 21 items posted price increases of more than 1% in June, including four that were up 2% or more. Note that these are mostly categories for which prices typically do not rise particularly fast. As Chair Powell has noted repeatedly, the bulk of inflation pressure in recent years has come from core services, not from goods. In fact, core goods prices in the CPI were on balance down slightly in 2023 and 2024.

The price changes should be particularly troubling given the flow of anecdotal information. Most firms have indicated that they have been holding the line on prices so far but are likely to attempt to pass through higher tariff costs going forward. Chair Powell referenced that exact dynamic in his post-FOMC press conference on Wednesday. June could prove to be just the tip of the iceberg, although that, of course, remains to be seen.

Motor vehicle prices bucked the trend in June, falling for both cars and light trucks. GM and Stellantis both reported in their second quarter earnings that they took a substantial profit hit in the quarter from tariffs, as they held off on raising sticker prices. Industry sources suggest that the automakers have decided to maintain pre-tariff pricing for most models through the end of the 2025 model year and to revisit their pricing strategies when they begin to roll out 2026 model year vehicles, typically in October. This is why I noted above that I consider motor vehicles to be a special case.

In any case, the broader point is that the price increases seen in June may represent just the beginning. I anticipate that tariff-related consumer price hikes are likely to intensify in July and August.

CPI versus the PCE Deflator

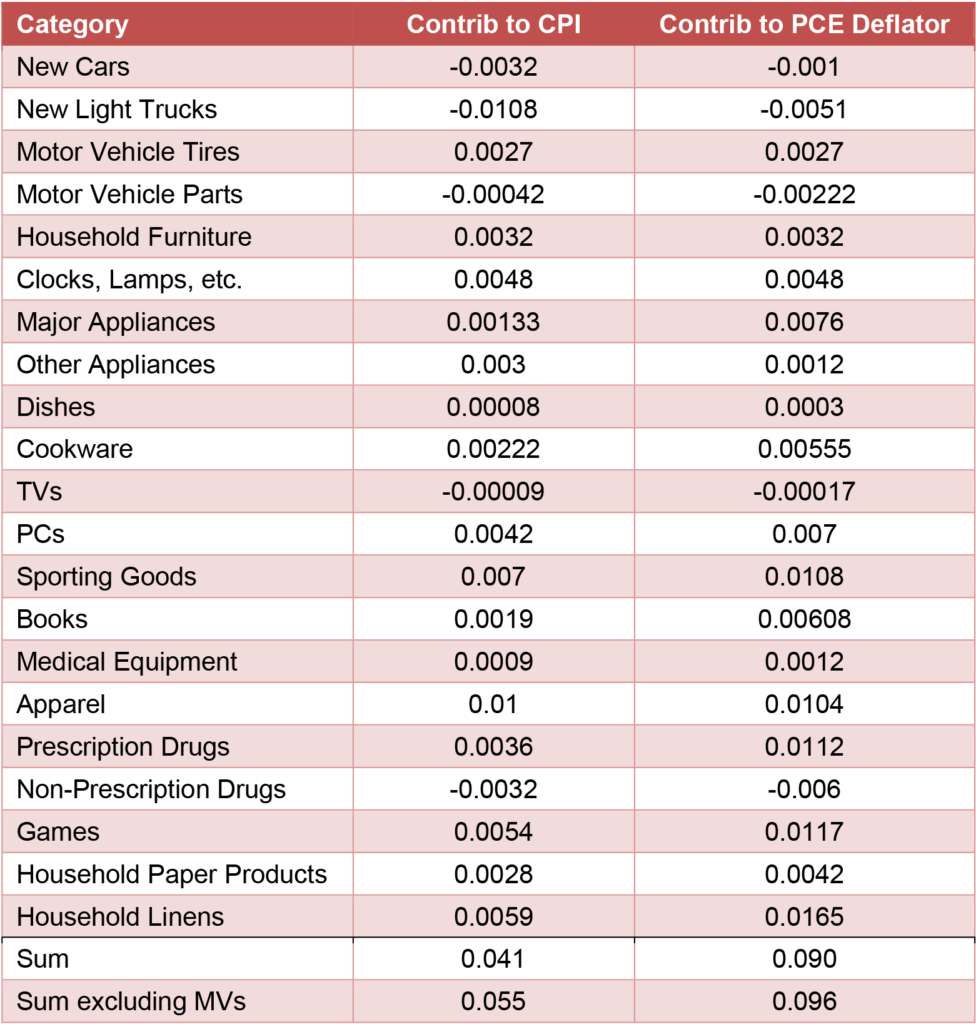

As already noted, the weight of the imported goods group is noticeably larger in the PCE deflator than in the CPI. As a result, the impact of tariffs-related price increases should be greater for the former, which is the Fed’s preferred price gauge. This shows up in the contribution of each line item to the aggregate in June, calculated as the product of the weight and the monthly percent change (Exhibit 3).

Exhibit 3: June Contributions for Imported Goods Line Items

Source: BLS, BEA.

Most of these line items carry tiny weights and thus individually do not move the needle for the aggregates. However, when taken together, given the incidence of outsized price increases seen in June, the magnitude of tariff-related inflation was becoming significant. The aggregate impact of these imported goods categories added up to roughly five basis points for the CPI and almost 10 basis points for the PCE deflator.

This helps to explain why the core CPI rose more slowly in June than the core PCE deflator when, in most months, the reverse is the case. In June, the core CPI increased by 0.23% while the core PCE deflator rose by 0.26%. Had the 21 line items all been flat, not a bad approximation in normal times, the core inflation gauges in June would both have been in the “low” +0.2% range that is roughly consistent with 2% annual inflation.

Moreover, if, as I have suggested, the tariff-related price hikes intensify, the gap should widen further. For example, if the tariff impacts double in July from June, the core PCE deflator would be pushed up by close to a full tenth more than the core CPI.

Clear impact from tariff hikes

The detailed breakdown of the June inflation numbers shows a clear impact from tariff hikes, as consumer prices for imported goods rose sharply in many cases. The headline and core inflation aggregates rose by almost half a tenth of a percentage point for the CPI and nearly a full tenth for the PCE deflator. If more firms pass through their tariff-related costs in July and August, the inflation figures are likely to accelerate further, particularly the PCE deflator, the measure on which the Fed focuses.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.