The Big Idea

Background on tariffs

This material is a Marketing Communication and does not constitute Independent Investment Research.

The impact of tariffs on economic activity and inflation has been slow in coming this year, but it feels like crunch time is finally here. The US appears to be negotiating furiously ahead of the August 1 deadline, reaching several deals over the past week, and a template is beginning to become clear for many of the remaining dominoes to fall into place. This allows for some very rough calculations of the possible impact of tariffs on economic activity and prices.

Trade flows and deal progress

Merchandise imports in 2024 totaled $3.26 trillion, a little more than 11% of GDP. Meanwhile, goods exports totaled just above $2 trillion last year, a little over 7% of GDP.

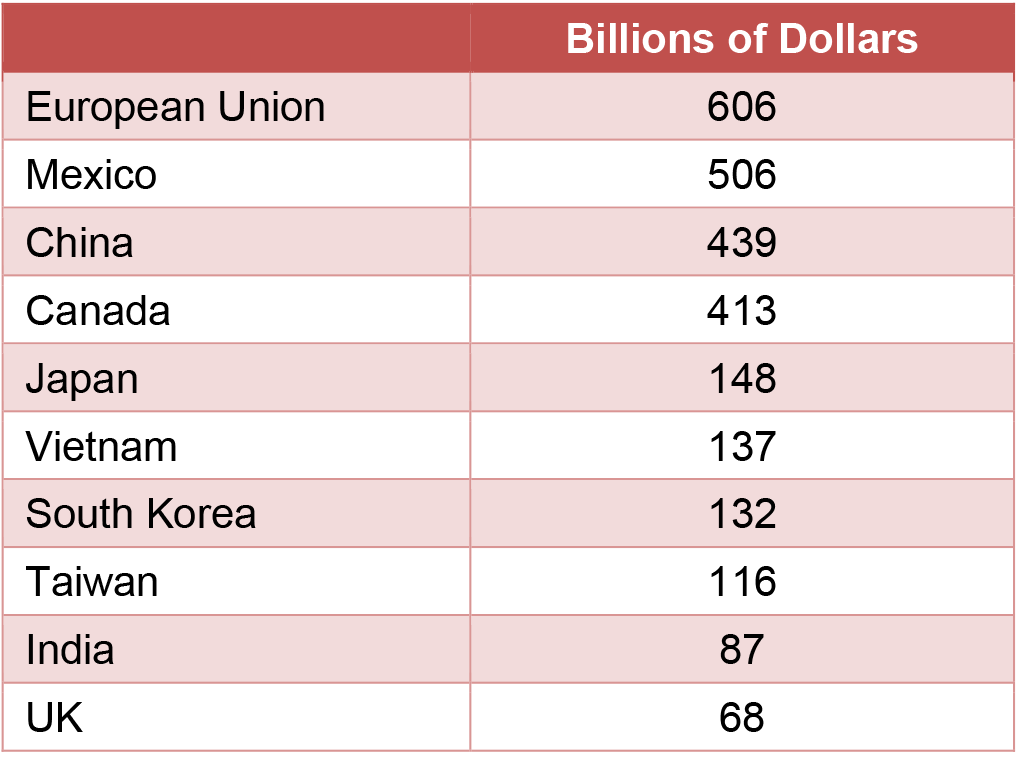

Among the top 10 countries importing into the US, the administration has already struck deals with the UK (#10) and Vietnam (#6) (Exhibit 1). On July 22, the US announced a tentative agreement with Japan (#5). On Wednesday, news reports indicated that the US and EU, the #1 trading partner when considered as a bloc, were close to a framework for a pact.

Exhibit 1: Merchandise imports in 2024

Source: Census Bureau.

China has always been on a separate track. The administration’s original plan was to keep China at arm’s length, craft deals with everyone else, and then gang up on China and force them to restructure their economy away from such a heavy export emphasis. That blueprint never got very far, and, after imposing massive tariffs on China in April, the US was forced to relent and cut a deal with China in May. Now, the China talks are entirely separate. Treasury Secretary Scott Bessent noted a few days ago that the US and China have reached a good understanding, and he thinks that another 90-day extension is likely after the current deal lapses on August 12.

With the Vietnam agreement and several smaller deals with Indonesia and the Philippines, a template seems to be forming for the Asia region. At various times of late, the US was said to be close to completing pacts with South Korea, Taiwan and India.

That would leave the US’s neighbors, Canada and Mexico. The latest news from up north is that Prime Minister Mark Carney has grown less optimistic that a deal can be achieved by August 1. Meanwhile, Mexico President Claudia Sheinbaum has been relentlessly optimistic that the US and Mexico would reach a deal. It is worth noting that most trade with Canada and Mexico is exempt from tariffs due to the USMCA, which needs to be renegotiated before it expires next year.

Deal Template

The April 9 pullback from Liberation Day set reciprocal tariffs at a default level of 10% for everyone but China. My expectation has been that the Administration would seek to maintain tariffs of at least 10%, even after reaching agreements with various trading partners. Recent news suggests that the magic number may be closer to 15%. Japan agreed to a 15% baseline, while the EU is said to have signed off on a 15% baseline tariff. Since tariffs on EU goods had been nearly 5% prior to this year and the April 9 reciprocal levies were on top of that, a new 15% tariff would essentially lock in the status quo since April.

The shift from 10% to 15% as a baseline is not as dramatic as it may appear at first glance. The reason is that the original 10% reciprocal tariffs were layered on top of existing tariffs, while the 15% tariff rate (or different levels for others) agreed upon in the Japan deal is an all-in figure.

Well over half of imports from Mexico and Canada get USMCA treatment. If we exclude that portion, perhaps worth about $600 billion in 2024, goods imports were around $2.7 trillion. If we assume that the average tariff on that $2.7 trillion will be 15%, up from less than 5% before this year, the overall price tag of the new tariffs would be on the order of $300 billion to $400 billion annually. Before this year, the US was collecting close to $50 billion per year in tariffs.

Tariff arithmetic

The magnitude of tariffs impacts several aspects of the economic outlook. First, tariff revenues for the federal government will at the margin improve the fiscal outlook. In May and in June, the federal government collected between $25 and $30 billion per month in customs receipts, up from less than $10 billion per month a year ago. Of course, and this is part of the rationale for tariffs in the first place, putting a 15% tax on imported goods will presumably result in fewer imports, which will, in turn, limit the revenue windfall. I am assuming that tariff hikes will bring in something like $150 billion to $200 billion per year over the next few fiscal years. That is a huge amount of money, but, sadly, in the context of annual deficits in the vicinity of $2 trillion, it will only be of limited benefit for the troubling fiscal outlook.

Of course, like any tax increase, someone will have to pay for it. Administration officials insist that foreign producers will pay the entire tab. While this is possible, and may be accurate in a few specific cases, it is doubtful that US consumers will escape any hit. Let’s assume arbitrarily that half of the tariff tab falls on the shoulders of consumers. Based on the arithmetic above, the result would be a loss of purchasing power of about $100 billion for US households, a small but noticeable hit. Nominal consumer spending in the US runs at about $20 trillion per year, so $100 billion represents one-half of one percentage point. Enough to be noticed, but not so large as to send the consumer into a tailspin.

Translating the arithmetic to inflation, $270 billion in goods imports represents about 1.3% of consumer spending. If tariffs go from between 2% and 3% on average to an average of 15% and consumers end up bearing half of the cost, then consumer prices would rise by about eight tenths of a percentage point (1.3% of consumer spending times a 6% price hike).

In reality, the hit to purchasing power and the bump to inflation would be less than the figures derived above, since the tariffs apply to the wholesale value of imports, not their retail sticker price. At the same time, based on empirical evidence of past instances of tariff increases, consumers would be fortunate if they only bear half of the burden. So, there are certainly risks on either side of these estimates, but they do at least provide a general sense of the magnitude of the looming impact on economic activity and prices.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.