The Big Idea

FOMC’s surprising optimism

This material is a Marketing Communication and does not constitute Independent Investment Research.

When the FOMC publishes new economic projections, most economists and financial market participants compare them to the prior 3-month-old estimates. While it helps to watch how Fed forecasts evolve, a more informative point of reference is the evolving differences between FOMC projections and the private sector consensus. Ironically, despite frequent protestations from administration officials that the Fed is factoring in too much of a growth drag and excessive inflation associated with tariffs, in reality the FOMC is more optimistic than private forecasters on GDP growth, the labor market and inflation in 2025.

FOMC projections

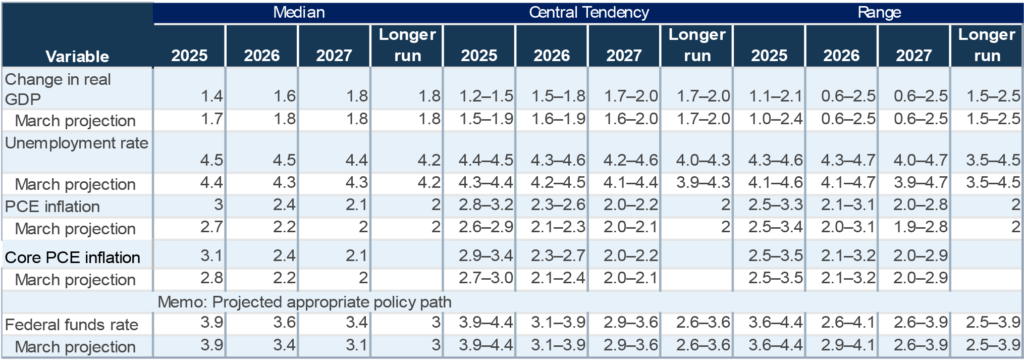

The FOMC releases economic projections on a quarterly basis along with the more closely followed policy projections, the so-called “dot plot”. The usual analysis of these figures entails comparing the latest forecasts with those of the prior quarter, a practice that is consistent with the way the FOMC displays the estimates (Exhibit 1).

Exhibit 1: FOMC June Economic Projections

Source: Federal Reserve.

The main narrative coming out of the recent FOMC meeting was that the Fed had lowered its 2025 growth projections (the median fell from 1.7% to 1.4%), raised the unemployment rate estimate (from 4.4% to 4.5%), and bumped up inflation forecast considerably (by three tenths for both the headline and core PCE deflator). The natural conclusion, which is broadly true, is that Fed officials have downgraded their economic projections due to the news on tariffs since mid-March, when the previous forecasts were released.

This naturally created friction between the FOMC and the White House, as President Trump and administration officials pushed a narrative that tariff hikes would not have any adverse impact on the economy or push up inflation, even temporarily.

FOMC versus private sector consensus

In my view, a better way to assess FOMC projections are to compare them to contemporaneous private sector forecasts. Presumably Fed officials and private sector forecasters are adjusting their estimates based on broadly the same information. So, differences between the two offer insight on what the FOMC may see differently from everyone else.

Looking through that prism, Fed officials are actually more upbeat about the near-term economic outlook than other forecasters. The median FOMC forecast in June for real GDP growth this year was 1.4%, which is double the consensus from the June Blue Chip Economic survey (+0.7%). This means that Fed officials are presumably penciling in a substantially smaller economic drag from tariffs for 2025 than private sector forecasters. Similarly, the FOMC projection for the unemployment rate in the fourth quarter of this year was 4.5%, slightly lower than the Blue Chip consensus of 4.6%.

In other words, despite all of the political flak that Chair Powell is taking from the Trump administration and others in Washington for pinning too much significance to the fallout from tariffs, Fed officials are actually offering an outlier upbeat view on economic growth for this year and a somewhat brighter forecast for the labor market.

The story is consistent regarding inflation. Chair Powell has been criticized by administration officials and by a number of Republicans on Capitol Hill during his recent semi-annual testimony for suggesting that tariffs are likely to generate higher inflation in the coming months. However, the FOMC’s median forecast for headline and core inflation as measured by the PCE deflator in 2025 were 3.0% and 3.1%, respectively, lower than the corresponding June Blue Chip estimates of 3.2% and 3.4%.

The temporary inflation burst that the FOMC projects is noticeably smaller than what is forecast by private sector economists. Chair Powell might have saved himself a certain degree of political grief if he had emphasized this gap between FOMC projections and those of private sector economists during the FOMC press conference and his recent Congressional testimony.

Aligning with the FOMC

For what it is worth, my own 2025 economic projections align more closely with the FOMC’s than the private sector Blue Chip consensus even though I participate in that survey. In fact, if anything, I have even more upbeat estimates than the FOMC, though only marginally. I expect real GDP growth of 1.5% on a Q4/Q4 basis in 2025 and for the unemployment rate to average 4.4% in the fourth quarter of this year. On inflation, my Q4/Q4 forecasts are 2.9% for the headline PCE deflator and 3.0% for the core PCE deflator, a tenth lower than the FOMC median and well below the Blue Chip consensus.

I cannot speak to exactly what assumptions are driving the FOMC or the private sector consensus figures, but my guess is that my relative optimism stems from a view that the administration will ultimately settle on a relatively benign tariff menu, similar to what is currently in place, and will largely resolve the issue before the end of this year, limiting the drag to the economy created by policy-related uncertainty.

Translating economic projections to monetary policy

As always, getting the economic projections right certainly would give forecasters a leg up on predicting the Fed’s rate decisions for this year and next. However, in the current circumstances, the differences in projections between Fed officials and private forecasters will likely prove to be of secondary importance. In a more normal economic landscape, the Fed would make their rate decisions based in part on their projections for the economy and inflation. However, policymakers have made clear that, in light of elevated uncertainty, they are currently unwilling to proceed based primarily on their forecasts. Instead, they are patiently waiting for clarity, a luxury that the FOMC is afforded by the fact that the economy and the labor market, at least for now, remain solid.

As the economy evolves, and, in particular, as inflation figures for the next few months establish once and for all how much tariff hikes will pass through to consumer goods prices, the policy leanings of the FOMC will evolve accordingly. I expect the economy to muddle through to the point that the FOMC will not be forced to slash rates to avert a recession. This will allow policymakers to maintain their focus on inflation. Assuming that tariffs generate a significant temporary boost to prices over the next few months, Fed officials will be eagerly waiting to see when and whether that burst upward in inflation abates. I suspect that as soon as evidence of a return to normal in the monthly inflation figures emerges, the FOMC will look to cut rates modestly further. Based on this outlook, I continue to pencil in two quarter-point rate cuts from the Fed before the end of 2025, though, if the tariff-related jump in inflation emerges later than I expect or takes longer to dissipate, then the timing of the easing could be pushed back by a few months.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.