The Big Idea

Layoff watch

This material is a Marketing Communication and does not constitute Independent Investment Research.

The consensus view is that the labor market, along with output growth, is poised to soften noticeably in the months ahead, as the fallout from higher tariffs disseminates into the broader economy. At the moment, the macro data are not yet showing a dramatic impact. April payroll gains were actually better than expected. Nonetheless, there are ample anecdotal reports that companies are slowing the pace of new hires as they navigate the heightened uncertainties over tariffs. On the other side of the labor equation, thankfully, it appears that firms have so far held off from widespread layoffs. The weekly initial unemployment claims data are traditionally among the timeliest indicators of an impending acceleration in job cuts, and these data so far are largely steady.

Unemployment insurance

The federal government pays unemployment insurance (UI) to covered workers who are laid off. The program is administered by the states, so eligibility rules and payouts vary from state to state, but the bill is paid by the federal government and ultimately funded by taxes on employers. Most companies are required to participate in the unemployment insurance system, paying taxes so that any workers they let go can collect benefits. Payroll employment in April totaled just over 159 million, while the universe of covered employment in the UI system is about 152.5 million, about 96% of payrolls.

Incidentally, once a quarter, the federal government requires all companies included in the UI system to submit a roster of employment. These quarterly censuses of employment are used by the BLS to reconcile the survey-based monthly payroll estimates. Once a year, the BLS updates its payroll benchmark, replacing the preliminary survey estimates with a more concrete count of workers derived from this dataset.

Weekly initial claims

Every week on Thursdays at 8:30, the Employment and Training Administration of the US Labor Department releases a count of initial unemployment claims. The ETA tallies up the figures provided by various state labor offices of the number of people who filed an application for unemployment insurance. The other primary statistic in these weekly releases is continuing claims, which is the total number of people collecting benefits at the time.

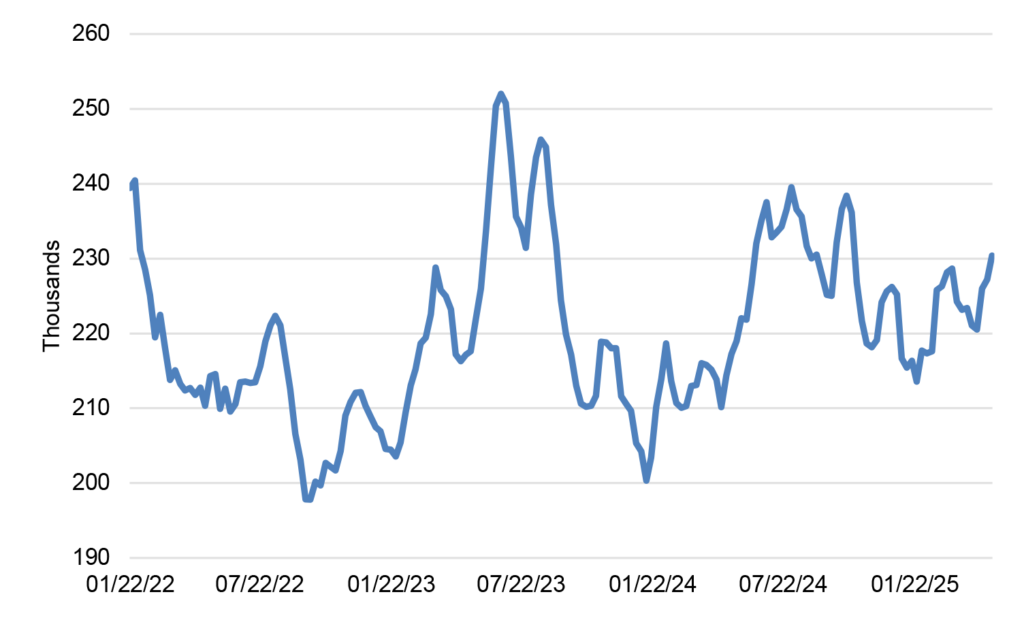

After unprecedented figures in the early days of the pandemic, when they spiked into the millions a week for several months, initial claims settled into a relatively narrow range as the economy fully reopened. Looking at the 4-week average of initial claims going back to early 2022, the scale is incredibly narrow (Exhibit 1). The series has spanned a range of barely more than 50,000 from top to bottom and has spent most of the past four years between 210,000 and 230,000.

Exhibit 1: A narrow range on the 4-week average of initial unemployment claims

Source: Labor Department, ETA.

In 2022, when the economy was enduring a historic labor shortage, initial claims averaged 214,000 for the year. As conditions began to normalize in 2023, the yearly average crept up to 223,000. As it happens, the yearly average in 2024 and the year-to-date figure for 2025 are also exactly 223,000. Despite considerable week-to-week volatility in the series, the underlying trend has been remarkably steady for over two years.

You may notice that the series has inched up over the past few months. In fact, the latest reading of the four-week average increased to 230,000, the highest since October. My first reaction is to note that the current 4-week average includes the 241,000 for the week of April 26 that was inflated by New York City schools spring break—evidently, non-salaried New York City school system employees are allowed to file for and collect unemployment checks during breaks, but the seasonal factors do a poor job of adjusting for this because the school holidays move around from year to year. Once this reading drops out of the 4-week window, the average is likely to fall, as it did earlier this year when there was an outlier 243,000 weekly reading in February that proved a one-off.

The extremely tight range on this measure may distort the perception of swings in the numbers. The historical rule of thumb that I learned in my early days in the business was that 300,000 (or lower) was consistent with a very strong economy, while 400,000 or higher signaled a recession. In that context, it is easy to understand why I am not excited about a backup from 215,000 or 220,000 up to 230,000. In reality, these numbers are still indicative of a historically low pace of layoffs.

Note that this perspective might have served the FOMC well last year. When Chair Powell and the committee were on the verge of panic last summer over the prospect of a weakening labor market—after a couple of sub-100,000 payroll advances and a backup in the unemployment rate—the fact that initial claims ran up from 210,000 to 240,000 seemed to offer confirmation of a decisive weakening in labor demand. However, the rate of new filers remained consistent with a historically low pace of layoffs.

In past episodes of tight labor markets, initial claims still ran well above the level of recent years. In 2005 to 2007, initial claims barely fell below 300,000 and in the 1999-2000 period, the number of new filers generally ran between 250,000 and 300,000. By the spring of 2001 and the summer of 2008, respectively, initial claims exceeded 400,000, the rule of thumb for a recession signal.

In any case, by the time the FOMC got around to its dramatic 50 bp rate cut in September of last year, initial claims had already slid back into the 220,000s, and then immediately after the Fed pulled the trigger on its easing, the September payroll gain ballooned to 240,00, an indication that officials’ labor market concerns had been overwrought.

The lesson here in my view is to maintain a broader context. Even if initial unemployment claims continue to creep higher, it would hard for me to worry much as long as the readings are below 250,000 or even 275,000. That said, there is a plausible case for a substantial pickup in layoffs over the next few months, associated with the economic fallout from tariffs, so it will be important to monitor the weekly UI data for signs that firms are beginning to shed workers at a noticeably faster clip. But the increase would need to be far steeper than anything seen over the last few years to be truly worrisome.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.