The Big Idea

Public spending cools, slowing growth

This material is a Marketing Communication and does not constitute Independent Investment Research.

In the second half of 2022 and throughout 2023, government spending provided a substantial boost to the economy. That changed in the first quarter of this year, when public sector outlays added only two tenths to real GDP growth. Government expenditure gains may pick up somewhat in the second quarter, but this component of the economy is unlikely to return to the unusually steep gains seen last year, contributing to my expectation of a moderating trend in real GDP as the year progresses.

Government spending

Not all government spending counts in the GDP accounts as output. For example, transfer payments boost household income but do not directly show up in the government component of GDP. Of course, when services such as medical care are delivered or cash spent, the transfers may help to boost consumption. In contrast, when the government buys goods such as military equipment or directly provides services such as public school education, the output is classified in the government sector.

Overall government outlays account for roughly 17% or one sixth of overall GDP, but this sector is rarely discussed in the context of the broad economic outlook. Federal expenditures run at around $1.5 trillion annualized, or about 6.5% of real GDP, while state and local government outlays tally up to almost $2.4 trillion, or 10.5% of real GDP.

The measurement of government output is somewhat problematic. It is simple enough to measure the price tags of tanks and jet fighters bought by the Pentagon, but for the average government worker who is processing forms or developing the specific parameters of a program, quantifying the economic value stemming from that work is difficult. As a result, for large portions of nondefense government spending, the BEA calculates output based on the total hours worked by government employees. In other words, it approximates output by counting the inputs.

Public sector boom

As is the case for many components of the economy, government output has been on a roller coaster since Covid. Government activity leaped initially in the spring of 2020, as the federal government stepped in to support the economy in numerous ways. However, the public sector’s contribution to GDP was negative in seven of the next eight quarters, as the level of government outlays retreated.

Once the level of government output had returned to normal by mid-2022, the tide swung dramatically. Defense spending has generally picked up, reflecting in part the US support for Ukraine’s defense and more recently aid to Israel. Moreover, state and local governments have been on a spending spree. A stronger-than-expected rebound in tax receipts along with an unprecedented flow of federal support during and after the pandemic left these jurisdictions flush and looking to expand their provision of goods and services. Moreover, as we know from the payroll employment data, state and local governments have been hiring aggressively for some time, restoring the headcount that had been slashed during Covid. Given the calculation methods described above, the higher staffing numbers translate directly into higher output.

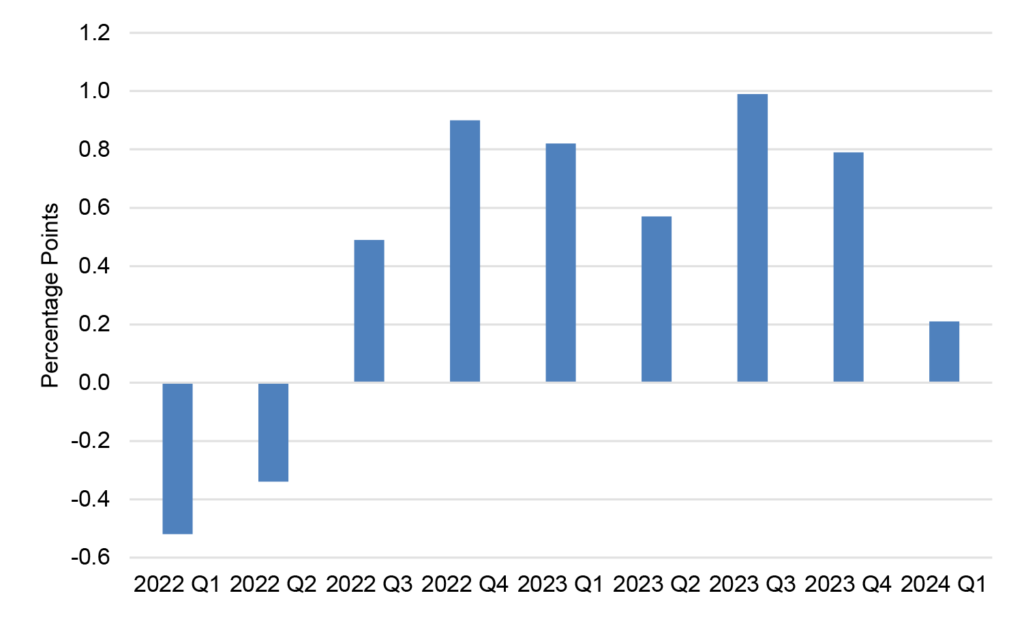

The public sector was a drag on real GDP growth in early 2022, but for six straight quarters beginning in the summer of 2022 added at least half a percentage point to growth (Exhibit 1). For all of 2023, the government component accounted for 0.7 percentage points, or nearly 30% of the 2.5% growth in real GDP, almost double its corresponding proportion of the economy.

Exhibit 1: Government Spending Contribution to Quarterly Real GDP

Source: BEA

First quarter breather

Several factors combined to produce a substantial slowdown in the increase in government outlays for the first quarter, as the public sector added only two tenths of a percentage point to real GDP growth. Federal expenditures were roughly flat in the quarter. Delays in the passage of the FY2024 budget, which finally was enacted at the end of March, undoubtedly restrained spending. When the federal government operates under a continuing resolution, agencies that rely on appropriations typically see close to a flat overall budget relative to the previous year. In addition, since a continuing resolution does not include new programs and priorities, agencies are unable to tackle new projects, likely dampening hiring and in turn output.

Similarly, the delay in passing the large foreign aid package that had been pending since the turn of the year (the legislation was finally signed into law on Wednesday) slowed defense expenditures. With both the overall budget and the foreign aid supplemental now in place, federal spending should resume growth in the spring and over the balance of the year.

On the state and local government level, consumption outlays continued to expand noticeably in the first quarter, exactly what we would expect in light of ongoing large monthly payroll increases. However, investment in structures, mainly spending on roads and bridges, paused in the first quarter after marked growth in 2023. I would attribute last year’s strength primarily to the federal infrastructure bill, which was enacted in 2021. The lags in getting public construction projects cranked up are well-chronicled—think back to the “shovel-ready” controversy in 2008—as the bidding process for contracts, environmental reviews and other approvals take time. It is not at all surprising that the money from the massive 2021 federal infrastructure package only began to flow in earnest last year.

In any case, state and local government construction expenditures were flat in real terms in the first quarter. I highly doubt that the impetus from the federal largesse has already begun to peter out. However, given the already-elevated pace of outlays by late last year, it is plausible that incremental growth will be noticeably slower going forward than in 2023.

Looking ahead to the current quarter, I expect that federal government outlays will rise, while the gains at the state and local level may be closer to the first quarter’s 2.0% rise than to last year’s surge. In all, I project that the government sector may add about three tenths to real GDP, and the positive impetus in the second half of this year may remain closer to the slim first quarter boost than to 2023’s hefty contributions. A more modest pace of growth in the public sector would play a part in the deceleration in the economy that I anticipate later this year.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.