The Big Idea

Latin America | Lessons learned in 2022

Siobhan Morden | December 16, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

It is always a learning curve in emerging markets, and 2022 was no different. The biggest disappointment in Latin America was Ecuador while Costa Rica became the surprising outperformer, slowly building on two years of positive momentum. These two credits provide important takeaways for next year and represent opposite ends of the risk spectrum next year. Attractive valuations among ‘B’ credits, the performance of quasi-sovereigns relative to the sovereign and the performance of ‘BB’ credits all had useful lessons to teach.

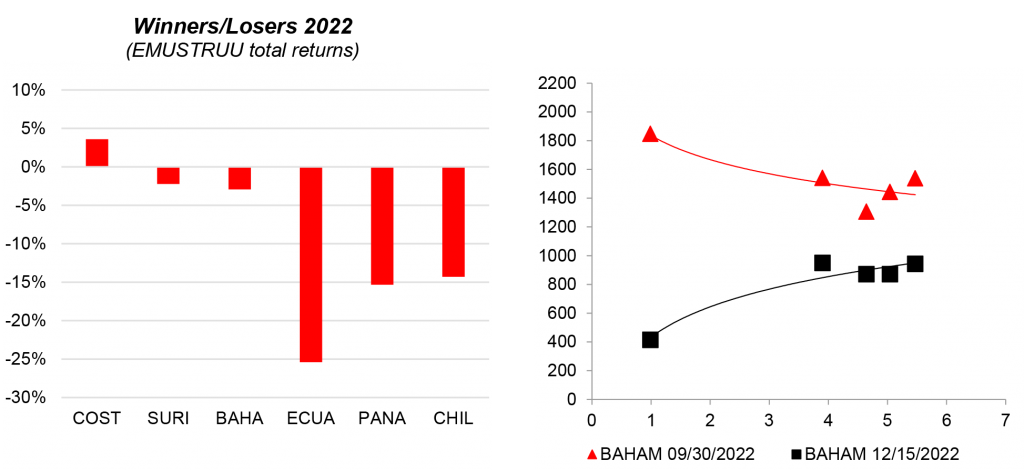

Exhibit 1: More losers versus winners for 2022 – Costa Rica and the Bahamas the exceptions

Source: Bloomberg

#1 No sovereign winners other than Costa Rica

Costa Rica has been impressive not only for its relative outperformance for two consecutive years but also for delivering positive sovereign debt returns in Latin America in 2022 (Exhibit 1). Our neutral recommendation shifted increasingly optimistic through the year as officials slowly established an impressive track record. This unique outperformance merits closer review.

Costa Rica first tackled its liquidity risks and relied on dependable local markets in 2020 and 2021 and then broadened financial support to the multilaterals in 2022. It also reduced solvency risks with an impressive back-to-back fiscal adjustment in 2021 and 2022. The country’s low stock of debt also offers valuable diversification and lower exposure to adverse external markets. Current tighter valuations may slow the pace of relative outperformance; however, the transformation of economic reform under a rule-based and highly democratic country creates a gradual path towards investment grade status and reaffirms its low beta status.

#2 Bahamas lands an impressive finish

When the index is off 14% and most credits are down more than 10%, the 2.9% total return losses in the Bahamas feels like a win. Bahamas, as one of our top picks, finished the year strong with admittedly high volatility. There were few if any stable carry trades through the double whammy of US equity and Treasury weakness. The knee-jerk recovery in the fourth quarter this year has been impressive with BAHAM’2024 bouncing 13 points from 10/17 to 12/14.

The Bahamas rally recognizes the country’s effective policy management including faster fiscal adjustment—it is the only country in Latin America with a real decline in spending—and proactive financial management to improve data transparency, investor relations and deepen local markets. The yield curve has fully normalized with bullish steepening and spreads now comfortably below 1,000 bp. The normalization on credit spreads (Exhibit 1) may open more financing opportunities and reduce rollover risk. The impressive year-end gains suggest a slower phase of spread tightening that should depend on a steady pace of fiscal adjustment (high revenues), strong tourism and effective financial management.

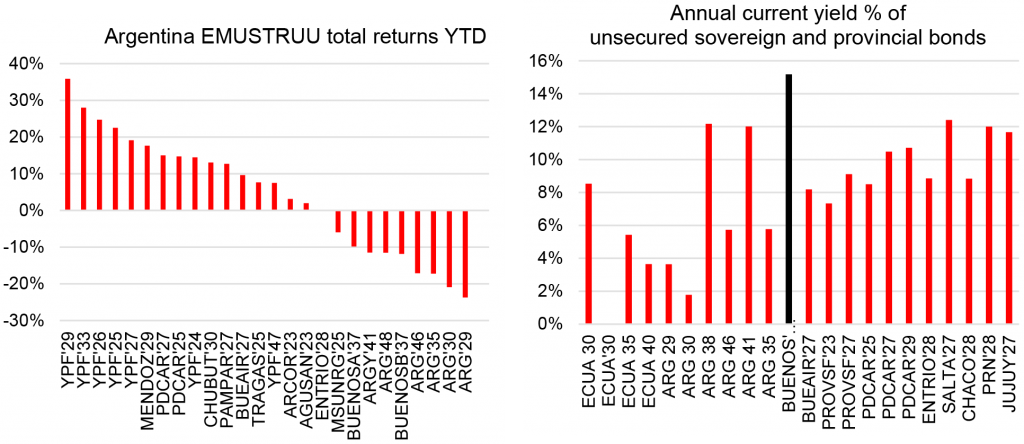

Exhibit 2: The divergence on performance and current yield between quasi-sovereigns and the sovereign

Source: Bloomberg

#3 The preference for Argentina quasi-sovereigns

Our core preference continues to favor the quasi-sovereigns over the sovereign for better relative fundamentals and higher current yield. The relative performance this year clearly validated that view but more so for the smaller provinces that benefited from their illiquidity and scarcity value (Exhibit 2).

The Province of Buenos Aires outperformed the sovereign but didn’t deliver the impressive positive returns of the other quasi-sovereigns. The benchmark liquidity increased the correlation to the sovereign irrespective to their relative fundamentals. There is a stark difference on cash flow and debt metrics. The quasi-sovereigns cannot deficit finance. Their inability to borrow restricts the ability to spend and prevents the accumulation of debt. The difficult macro conditions may complicate convertibility risks; however, $1 billion in annual debt service does not seem onerous compared to huge agrodollar inflows. Meanwhile, the moderate policy shift and strong IMF relations remains an anchor against crisis. The current prices at 34-35 not only imply a high probability of default but recovery below historical values (40-53). This seems overly pessimistic for a credit that does not need any solvency relief, and at worse may require only marginal liquidity relief. The 15% current yield on the BUENOS’37 (Exhibit 2) also provides a buffer with 15 FPV cumulative coupon and sinking fund payments in 2023-2024 against 34-35 current prices.

#4 Is Ecuador governable?

That remains the unresolved question. Ecuador started the year as the consensus favorite and then it all fell apart after a surge in political risks. The outperformance in the first half of 2022 reversed into the worst overall performance for 2022. There were high expectations of a successful reform agenda under the center-right management of the Lasso administration. However, governability quickly eroded after pushback from the obstructionist opposition and radical societal factions.

For portfolio managers, there is a tendency to favor countries with good managers. The positive intentions of a market-friendly manager may not easily translate into action for a minority government that cannot negotiate with an obstructionist legislature. There is no honest debate across society or the political establishment about what is necessary to strengthen dollarization, increase trend growth and broaden formal employment. There are also no checks and balances to reinforce responsible policies and no obvious leverage from the capital markets (under a dollarized economy) or the business community on the political establishment. Weak governability perpetuates structural macro imbalances that depend on high oil prices, weak budget flexibility and limited financing sources. This high medium-term uncertainty should weigh on the country’s backloaded coupon and sinking fund payments and remains an overarching constraint on credit risk. The low current yield also remains a disadvantage to other B rated credits (Exhibit 2).

#5 BB credits likely offer an ideal combination

The initiation of coverage of Guatemala and the Dominican Republic was opportune with strong fundamentals that insulate the countries against external risks. The ‘BB’ credit category offers unique defensive characteristics with financing flexibility, fiscal conservatism, and high trend growth. The low foreign exchange volatility also shows the relative isolation of domestic financial markets that would then minimize the contagion from global financial markets.

These countries have been immune to the cycle of rating downgrades with broader policy flexibility to manage external shocks. The higher yields also offer potential for carry returns, especially for the smaller credits with smaller stock of bonds outstanding (Costa Rica, Guatemala) or maybe even lower beta from benchmark credits (Dominican Republic) that diversify their funding program away from Eurobond markets. The higher quality credits should be less vulnerable at a mature phase of US Treasury weakness with higher overall yields relative to investment grade credits and lower beta relative to ‘B’ rated credits.

Siobhan Morden

Santander Investment Securities

1 (212) 692-2539

siobhan.morden@santander.us

U.S. Fixed Income Trading Commentary Disclaimer

This commentary has been prepared by the U.S. fixed income trading desk of Santander Investment Securities Inc. (together with its affiliates, “Santander”) for its institutional investor clients only, and may under no circumstances be redistributed beyond the recipient in whole or in part. The recipient is an “institutional account” as defined in FINRA Rule 4512(c) that (i) is capable of evaluating investment risks independently, both in general and with regard to particular transactions and investment strategies and (ii) will exercise independent judgment in evaluating any potential investments and any recommendations of any broker-dealers. For the avoidance of doubt, this commentary is not suitable for or intended for retail investors.

This commentary has not been produced or reviewed by, and does not otherwise reflect the views or input of, the Research Department of Santander (“Santander Research”). This commentary may conflict with the views of Santander Research, is not subject to all of the independence and disclosure standards applicable to research reports prepared for retail investors and is not independent from the interests of Santander. Santander may have positions (long or short) in, effect transactions in or make markets in the subject securities (or related derivatives) mentioned in this commentary, and such positions or trading may be inconsistent with this commentary. However, Santander is under no obligation to make a market in or otherwise provide liquidity in any security discussed herein. This material may have been previously communicated to Santander’s trading desk. Santander may have in the past or may in the future provide investment banking services (including underwriting activity and loans) or other services for the companies mentioned in this commentary.

This commentary has been provided for informational purposes only and is not a recommendation, offer or solicitation for the purchase or sale of any security or related instrument. This communication is intended to be short term and brief in nature, and therefore does not provide a full analysis of any issuer or security or a sufficient basis upon which to base an investment decision. The individual circumstances of the recipient’s investment objectives and needs have not been considered in this commentary, and nothing in this commentary constitutes investment, legal, accounting or tax advice or a representation that any investment strategy or service is suitable or appropriate to the recipient’s individual circumstances. Information contained herein has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made as to its accuracy or completeness. The recipient should not rely on this commentary for any investment decision or other action, and Santander expressly disclaims any liability for any losses arising from any reliance on or otherwise related to this commentary. This commentary reflects the personal views of the individual sender of such commentary, and no part of his or her individual compensation was, is or will be directly or indirectly related to its content. This commentary is provided as of the date and time thereof, and Santander does not undertake any responsibility to update or revise any of the information contained herein, which may change without notice. Past performance is not indicative of future results.

Fixed income securities, including those described herein, are subject to many risks, including, but not limited to, interest rate risk, the credit risk of the issuer, inflation risk, liquidity risk and risk of a downgrade by rating agencies. Emerging markets investments are additionally subject to political, economic, legal, regulatory, market, settlement, execution, currency and other risks. Fixed income, and specifically emerging markets, investments are not suitable for all investors.

Santander Investment Securities Inc. is an SEC registered broker-dealer, FINRA member and SIPC member. Santander Investment Securities Inc. is a direct, wholly-owned subsidiary of Santander Holdings USA Inc., which is a direct, wholly-owned subsidiary of Banco Santander, S.A