The Big Idea

Equipment check

This material is a Marketing Communication and does not constitute Independent Investment Research.

While consumer spending is by far the largest component of the economy and well supported by a strong household balance sheet, the second-largest component of domestic private final demand is business investment in equipment. Businesses are similarly well positioned to continue spending, at least in the short term. If gains continue in both sectors, it would be difficult for the economy to slide into recession, which appears to be a consensus call for 2023.

Pandemic balance sheet boost

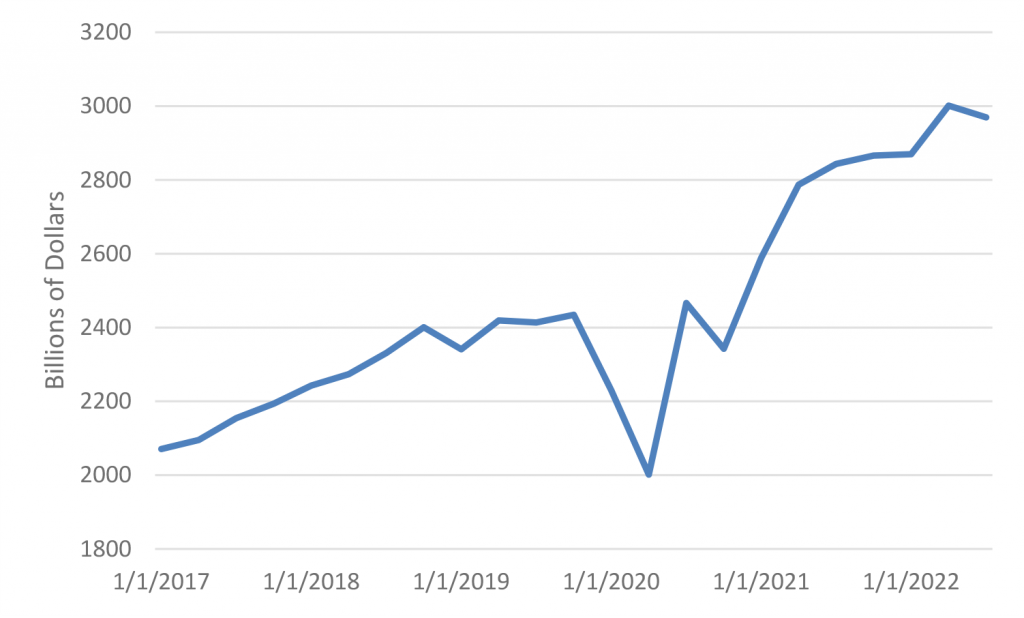

Just as consumers benefited from trillions of dollars of fiscal support during the pandemic, businesses generally weathered the Covid period well. Despite massive input cost increases during the pandemic, firms managed to not only preserve but to expand their profit margins in the aggregate. Corporate profits, as measured by the Bureau of Economic Analysis, soared in 2021 and have generally held at an elevated level so far this year (Exhibit 1).

Exhibit 1: Corporate profits remain high

Source: BEA.

According to the Federal Reserve, the net worth of nonfinancial businesses, both corporate and noncorporate, surged in 2021 by over $6.5 trillion, or nearly 17%, in 2021 and advanced slightly further in the first half of 2022.

Equipment spending outlook

Businesses therefore have the wherewithal to invest. The next question is whether the economic landscape is favorable for such spending. There are a mixed set of influences currently on businesses’ appetite to invest. On the plus side, labor has been both hard to find and expensive over the past year or two. As a result, if a business can find a suitable piece of equipment that allows it to operate more efficiently with regard to labor input, now would seem to be a particularly opportune time to do so. In addition, the evolving workplace, with firms across a variety of industries attempting to determine the optimal mix of in-person and remote work, will likely demand ongoing investment.

There are two potential negative forces that could limit businesses’ desire to invest going forward. First, economic uncertainty is a buzzkill for investment. If a business manager cannot easily project the firm’s sales over the next few years, it is difficult to run the numbers and justify large outlays. In particular, fears of a downturn generally dampen investment activity. It is not a coincidence that in the second quarter, when fears of a recession surged on the back of a massive spike in energy costs, business spending on equipment in real terms slipped at a 2% annualized pace after posting a robust 11.4% annualized increase in the first quarter. As those recession fears faded to a degree in the summer, equipment outlays revived, posting a 10.7% annualized advance in the third quarter.

The other looming negative is likely to hit gradually over time. Rising borrowing costs will eventually make it more expensive to fund large investments. For now, businesses have ample funds on hand, as described above. Moreover, many large corporations managed to borrow at historically low rates and extend the duration of their bonds during the pandemic. Over time, as these bonds mature, refinancing them will grow more expensive. In addition, sooner than that, some businesses will feel the pain of the Fed’s rate hikes. For example, smaller companies that get funding from bank loans or leveraged lending may already be seeing steep increases in their funding costs.

Data check

Given the mix of forces weighing on investment decisions, recent data offer some insight into the health in investment spending on equipment. As noted above, the GDP component in real terms posted strong growth in the first and third quarters, sandwiched with a modestly negative reading in the second.

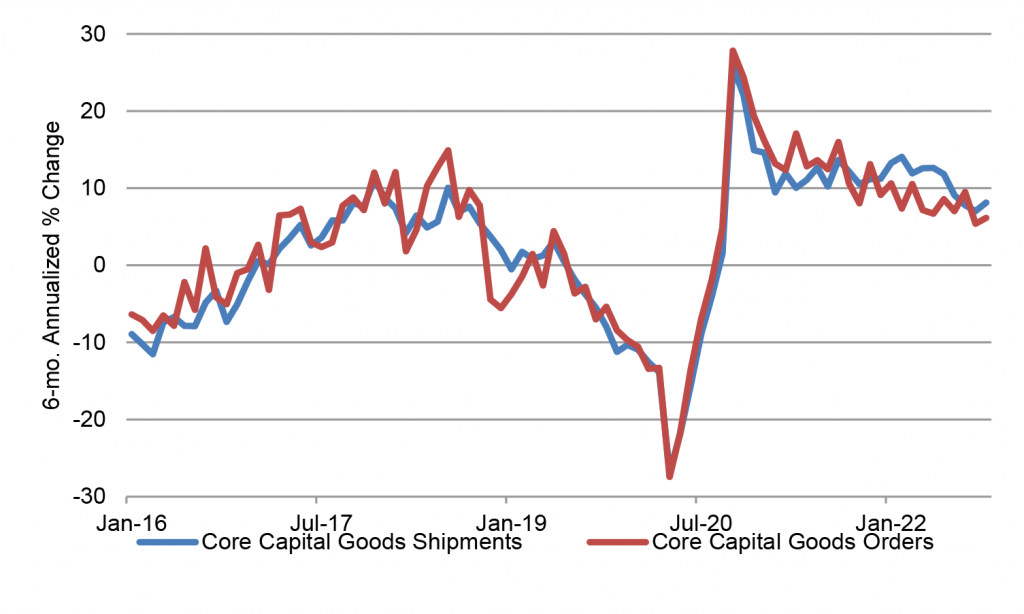

The monthly data on core capital goods orders and shipments offer a timelier look at the sector. In fact, the core capital goods shipments figure—in this case, “core” excludes the defense and aircraft sectors—serves as a decent proxy of the corresponding GDP component. The October durable goods report offered good news. After a soft result in September, core capital goods orders and shipments rebounded vigorously in October. The core capital goods orders figure posted a solid 0.7% gain, while the corresponding shipment figure surged by 1.3%, the sharpest monthly rise since January.

These data tends to be notoriously volatile from month to month, so a moving average tends to provide a more accurate read (Exhibit 2). While the pace of advance for each has decelerated somewhat this year, the gains are still impressive. The shipments measure increased at better than an 8% annualized clip in the six months through October, a solid result even after accounting for elevated inflation.

Exhibit 2: Core capital goods orders and shipments

Note: six-month annualized rate of change.

Source: Census Bureau.

A kicker that could further boost investment spending in the near term is the release of pent-up spending as special factors in the transportation sector unwind. Motor vehicle sales have been stronger in October and November, exceeding a 14 million unit annualized pace in both months compared to a 13.4 million unit average in the third quarter. This reflects the long-delayed unwinding of supply chain snags that have stymied auto sales for the better part of two years. Most of the impact of higher auto sales will accrue to consumer spending, but businesses are also likely to take delivery of more vehicles as inventories are replenished. Meanwhile, Boeing has finally made progress in resolving regulatory restrictions on the deliveries of both MAX and 787 Dreamliner planes recently, which could lead to a step-up in aircraft shipments in the coming months. Neither of these factors represent a sustainable source of demand over the long term, but they should support equipment outlays in the short term.

At the moment, my fourth quarter estimate for the business investment in equipment component of real GDP splits the difference between the soft second quarter reading and the double-digit gains posted in the first and third quarters. I have penciled in a 6% annualized advance. Heading into early 2023, the pace of growth could fade further, but there appears to be sufficient momentum to sustain at least some degree of increase in real terms.

In sum, the near-term outlook for business spending for equipment is good though not great. Still, weighed against consensus expectations for a mild recession in early 2023, if consumer spending and the largest chunk of business outlays continue to expand, it is hard to see how the economy will contract.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.