The Big Idea

Out-of-consensus calls on 2023 Latin America

Siobhan Morden | November 18, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

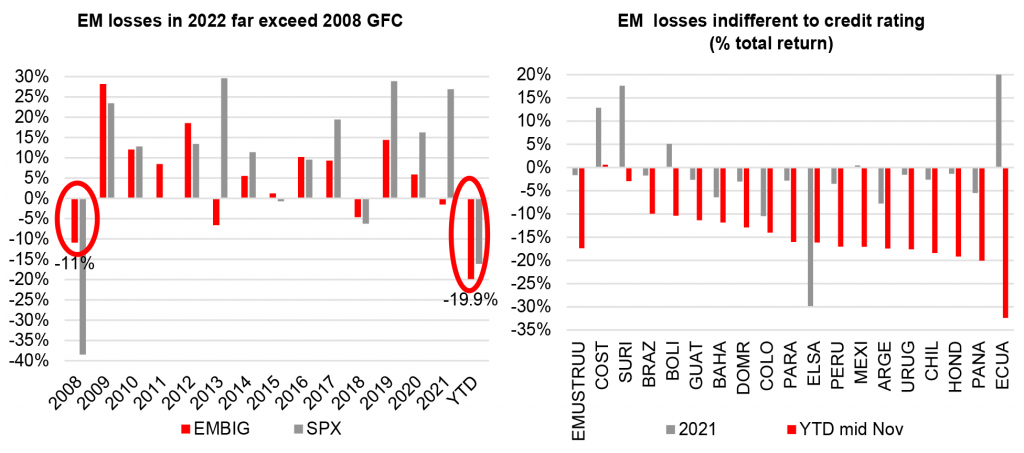

Emerging markets are closing the year with losses of around 20% and the worst performance in recent memory. Not even during the 2008 Global Financial Crisis did the markets get hit by the last year’s double whammy of wider credit spreads and much higher US Treasury yields. But bad news may become good news. Distressed valuations among select credits offer clear opportunities for positive surprise. And continuing uncertainty about global developments also argues for playing some defense and diversifying into select ‘BB’ sovereign credits with strong fundamentals, lower market beta and high current yields.

Poor returns have set up the opportunities for next year. In Latin America, only Costa Rica managed to post flat total returns this year (Exhibit 1). Losses across the rest of Latin America ranged from -10% in Brazil (BB-), -18% in Uruguay (BBB) and -32% in Ecuador (B-). This dragged some credits down to levels that discount important upside.

All of this leads to a pair of calls outside the consensus on 2023 Latin America:

- Invest in the upside on select assets trading at recovery value

- Invest in lower beta carry alternatives

Exhibit 1: Losses across emerging markets have overly discounted upside in some credits

Source: Bloomberg

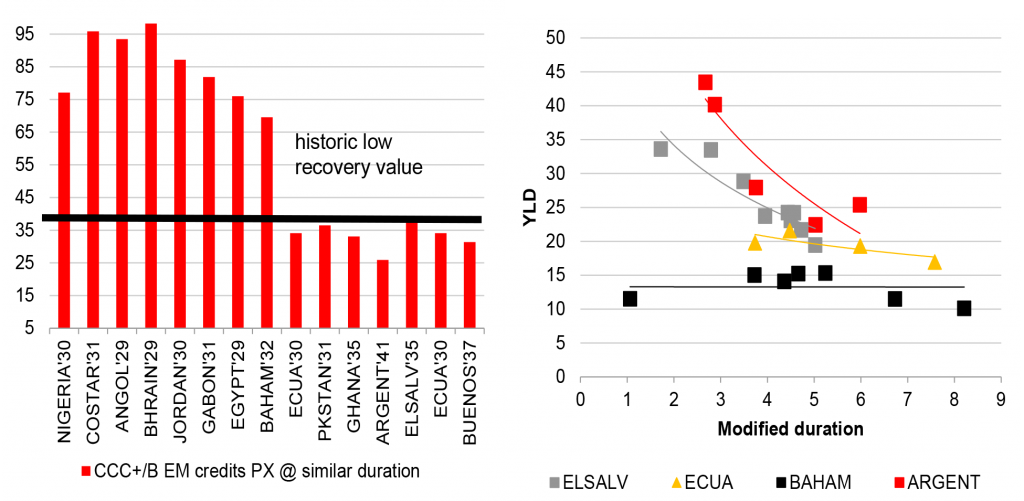

Upside on assets trading at recovery value

There are several credits that trade at their percentage-of-par claim on recovery value. The sub-40 bond prices for Argentina, the Province of Buenos Aires, Ecuador, and El Salvador imply imminent default with low recovery value (Exhibit 2). But this is where there is potential for positive surprise. There are credits like El Salvador that could pay for longer, or other credits that could even avoid default, such as the Province of Buenos Aires. And historically low bond prices also could also encourage countries to buy back debt, with El Salvador taking the lead and Ecuador soon to follow.

The Bahamas also is a top pick for next year. Its track record of effective policy management should continue to unwind macro imbalances. The continuing distressed yields do not fully account for potential economic stability and curve normalization. And its low bond prices again invite buybacks.

Exhibit 2: A range of credits trade below historic recovery value with distressed yield curves

Source: Bloomberg

El Salvador | Paying for longer. El Salvador will start 2023 with an important test in the January amortization of its Eurobond. My base case looks for a final payment at maturity with the possibility of another buyback on the 2025s. El Salvador can do this by diverting budget cash flow, relying on multilateral disbursements, or drawing down treasury deposits. The follow-through amortization payment on the 2023s would provide considerable budget flexibility.

The country has clearly demonstrated a willingness to pay, and the successful buyback last September also reduces the amortization calendar through 2025. The coupon payments are above-the-line payments financed with tax revenues and treated as fixed priority liabilities with corresponding cutbacks in domestic liabilities

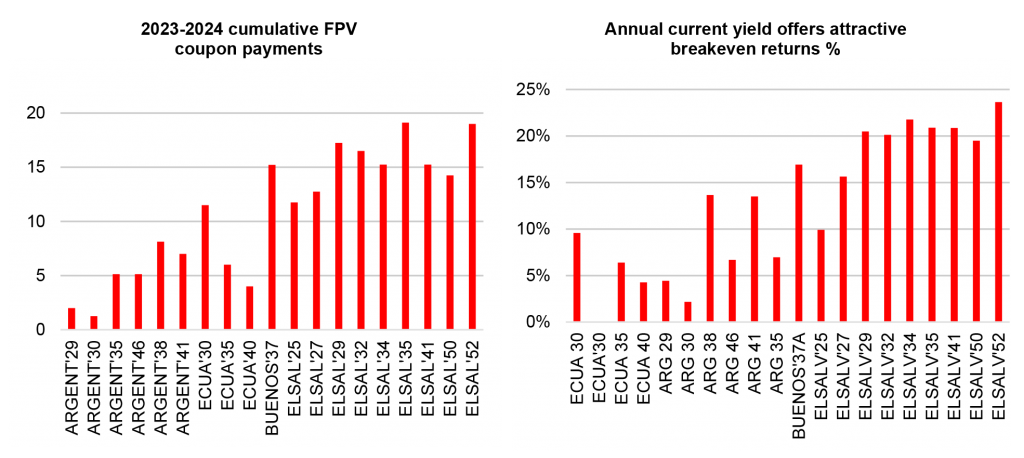

Smaller countries with smaller gross financing needs also typically do not choke on coupon payments. These coupon payments are quite valuable in light of bond prices still around 35-40 that translate into attractive breakeven returns (Exhibit 3). “Paying for longer” and avoiding default through at least 2025 would imply much higher bond payments closer to 50 on the longer tenors and much higher prices on the shorter tenors. There has been an important pivot since the September Eurobond buyback of the ELSALV’23s and ELSAL’25s with latest price gains. This removes El Salvador from the bottom of the pack for year-to-date performance and potentially the surprise outperformer for 2023.

Exhibit 3: El Salvador and Province Buenos Aires offer high coupons for attractive breakeven returns

Source: Bloomberg

Province of Buenos Aires | Avoiding default. This quasi-sovereign typically trades as a leveraged play on the sovereign. However, the high correlation to the sovereign and the higher spread premium does not recognize an important fundamental difference: The Province of Buenos Aires has a stronger balance sheet and much lower debt ratios. This is a common difference between sovereigns and quasi-sovereigns with fewer financing alternatives and less opportunity to accumulate debt.

The stronger fundamentals for the Province of Buenos Aires provide upside at current low bond prices. For those bullish on upside convexity in Argentina, the Province of Buenos Aires offers a better alternative with higher current yield at 17% and much lower default risk. The low cash price of 30 appears overly pessimistic compared to historic recovery value of 40-53, especially since cash flow and debt metrics wouldn’t argue for any solvency or liquidity relief. An expected moderate political and policy transition should not necessarily force a restructuring on the quasi-sovereigns based on convertibility risks alone. The BUENOS’37A also starts sinking fund payments in 2024 for cumulative payouts of 14 points through 2024 against current prices of around 30. This reflects the lowest breakeven recovery value through 2024 including El Salvador. And there is much more upside if the Province of Buenos Aires avoids default.

The Bahamas | Path toward normalization. There is nowhere that policy management matters more than in small open economies vulnerable to external shocks. First, it’s important to emphasize that the current macro imbalances have been the unfortunate outcome of two successive external shocks—not for policy mismanagement. Second, there has been an unblemished debt repayment track record. The Davis administration continues its proactive policy of sourcing adequate financing, under-executing the budget and improving investor relations.

The fiscal performance has been impressive with better-than-expected compliance through fiscal year 2021-2022 and into the first quarter of fiscal year 2022-2023. The country has had higher-than-expected revenues and spending cutbacks. The 12-month rolling primary accounts have now shifted into surplus with a marked departure from historical primary deficits. There has also been an ambitious launch on data transparency as well as frequent calls to improve investor communication and reduce unnecessary risk premium.

There is also the potential for debt buybacks after having contracted a financial advisor with monthly disbursements to a buyback fund. The curve has already normalized from the distressed curve inversion with a downward shift and bullish steepening. This trend should continue under my constructive view of fiscal discipline, liquidity buffers and debt liability management and reaffirms my bullish view. The supportive externals may allow for a break to below the distressed threshold of 1,000 bp.

The lower beta carry alternatives

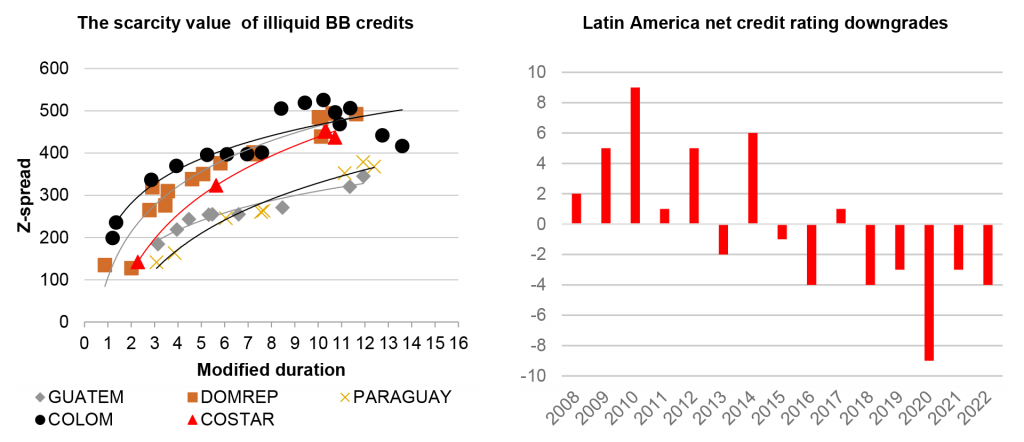

Continuing high uncertainty heading into 2023 highlights the importance of defensive positions. Latin America along with other emerging market regions have seen another year of net rating downgrades with fundamentals still weak after Covid. Next year brings continuing risk of stagflation while fewer and more expensive financing may undermine fiscal discipline. There are a few credits like Costa Rica and Guatemala that offer an ideal combination of technicals and fundamentals:

- Positive rating action,

- High 7%-8% yields and

- Lower market beta.

The illiquid group of ‘BB’ credits like Paraguay, Guatemala and Costa Rica offer a buffer and diversification against continuing risk of contagion from external developments as well as resilient fundamentals and financing flexibility.

Costa Rica | The year of upgrades. Costa Rica has been the stealth outperformer in 2021 and 2022 and now finally the candidate for potential upgrades next year. This track record has been impressive but not surprising considering the fiscal transformation after two critical reforms: the fiscal rule and the public employment reform. The primary fiscal deficit of 2% of GDP in September 2018 has turned into a surplus of 2.2% of GDP in September 2022. This turnaround is even more impressive since it came despite repeated external shocks that represents a clear departure from other countries in the region. This now sets the country on a path towards debt sustainability and credit rating upgrades towards ‘BB’.

The rigidity of the fiscal rule in a highly democratic country reaffirms the importance of strong institutions. There has also been an important transformation across the society and the political establishment that recognizes the importance of a fiscal anchor and pushes back against any weakening of the fiscal rule. The lower gross funding needs also lowers the rollover risks with broader access to multilaterals and the first country to access the IMF-RFT loan facility. There has already been a convergence of credit spreads to BB comps; however, the illiquidity and low market capitalization reassures for low beta status against other liquid benchmark comps like DomRep and Colombia (Exhibit 4).

Exhibit 4: Costa Rica and Guatemala buck the trend of rating downgrades and offer scarcity value relative to liquid ‘BB’ credits

Source: Bloomberg, *Moody’s net rating action of cumulative rating action (+1) point upgrade and (-1) point downgrade

Guatemala | Resilient fundamentals. Boring is okay. The low beta status of a stable ‘BB’ credit remains an advantage with external conditions still uncertain. Guatemala, like Costa Rica, benefits from a lower stock of debt and a lower correlation to global financial markets. This reflects sponsorship from buy-and-hold investors and low if any contagion for the low integration of their local financial markets to global financial markets.

The ‘BB’ credits also now offer attractive yields with higher carry and less sensitivity to US Treasury rates. Guatemala ticks all the boxes across liquidity and solvency indicators with no obvious setbacks from unfavorable externals, other than the inflationary spike. There is more policy flexibility against the inflationary shock with a strong foreign exchange rate and clear fiscal anchor. The central bank prefers a more flexible monetary stance after weighing downside risks to growth from potential external shocks. Guatemala has delivered a particularly robust fiscal performance with the fiscal deficit improving far beyond 2019 pre-Covid levels. The central government deficit finished 2021 at 1.2% of GDP, the best levels over the past 10 years. The track record of fiscal discipline explains the low 30% debt-to-GDP ratio and the high foreign direct investment inflows. This provides a cushion against a relaxation on budget targets this year. The bottom line is that the strong fundamentals provide resiliency against external shocks and diversification against other EM credits.

Siobhan Morden

Santander Investment Securities

1 (212) 692-2539

siobhan.morden@santander.us

U.S. Fixed Income Trading Commentary Disclaimer

This commentary has been prepared by the U.S. fixed income trading desk of Santander Investment Securities Inc. (together with its affiliates, “Santander”) for its institutional investor clients only, and may under no circumstances be redistributed beyond the recipient in whole or in part. The recipient is an “institutional account” as defined in FINRA Rule 4512(c) that (i) is capable of evaluating investment risks independently, both in general and with regard to particular transactions and investment strategies and (ii) will exercise independent judgment in evaluating any potential investments and any recommendations of any broker-dealers. For the avoidance of doubt, this commentary is not suitable for or intended for retail investors.

This commentary has not been produced or reviewed by, and does not otherwise reflect the views or input of, the Research Department of Santander (“Santander Research”). This commentary may conflict with the views of Santander Research, is not subject to all of the independence and disclosure standards applicable to research reports prepared for retail investors and is not independent from the interests of Santander. Santander may have positions (long or short) in, effect transactions in or make markets in the subject securities (or related derivatives) mentioned in this commentary, and such positions or trading may be inconsistent with this commentary. However, Santander is under no obligation to make a market in or otherwise provide liquidity in any security discussed herein. This material may have been previously communicated to Santander’s trading desk. Santander may have in the past or may in the future provide investment banking services (including underwriting activity and loans) or other services for the companies mentioned in this commentary.

This commentary has been provided for informational purposes only and is not a recommendation, offer or solicitation for the purchase or sale of any security or related instrument. This communication is intended to be short term and brief in nature, and therefore does not provide a full analysis of any issuer or security or a sufficient basis upon which to base an investment decision. The individual circumstances of the recipient’s investment objectives and needs have not been considered in this commentary, and nothing in this commentary constitutes investment, legal, accounting or tax advice or a representation that any investment strategy or service is suitable or appropriate to the recipient’s individual circumstances. Information contained herein has been compiled from sources believed to be reliable, but no representation or warranty, express or implied, is made as to its accuracy or completeness. The recipient should not rely on this commentary for any investment decision or other action, and Santander expressly disclaims any liability for any losses arising from any reliance on or otherwise related to this commentary. This commentary reflects the personal views of the individual sender of such commentary, and no part of his or her individual compensation was, is or will be directly or indirectly related to its content. This commentary is provided as of the date and time thereof, and Santander does not undertake any responsibility to update or revise any of the information contained herein, which may change without notice. Past performance is not indicative of future results.

Fixed income securities, including those described herein, are subject to many risks, including, but not limited to, interest rate risk, the credit risk of the issuer, inflation risk, liquidity risk and risk of a downgrade by rating agencies. Emerging markets investments are additionally subject to political, economic, legal, regulatory, market, settlement, execution, currency and other risks. Fixed income, and specifically emerging markets, investments are not suitable for all investors.

Santander Investment Securities Inc. is an SEC registered broker-dealer, FINRA member and SIPC member. Santander Investment Securities Inc. is a direct, wholly-owned subsidiary of Santander Holdings USA Inc., which is a direct, wholly-owned subsidiary of Banco Santander, S.A