The Big Idea

A long winter ahead for rates

Steven Abrahams | October 21, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

Fundamentals do a poor job of explaining valuations in longer US rates at this point, so the more likely explanation is deceptively simple: more sellers than buyers. The US Treasury itself as an issuer is a net seller along with the Fed, banks, mutual funds and foreign central banks. Only foreign private portfolios have held up their hand to buy. Given the motives of most of these portfolios, selling pressure in Treasury debt could stay in the market until the spring. But with possible relief in the spring, fundamentals then should argue for much lower yields in the long end of the curve.

More sellers than buyers

Sellers in the Treasury market have made themselves fairly clear, and most are selling for reasons largely unrelated to the level of rates or relative value:

- The US Treasury. The federal deficit makes the US Treasury a steady net seller, and the Treasury issued or sold $99 billion in notes and bonds in September. My colleague Stephen Stanley projects the Treasury will sell more than $100 billion a month through March next year before annual tax receipts deliver enough cash to let the Treasury temporarily stop issuing. That could end a large part of the selling pressure in the spring.

- The Federal Reserve. QT hit full stride in September with Fed Treasury balances dropping by $60 billion and set to continue until the Fed declares the balance sheet normalized, likely two years or more. The Fed along with banks made up the biggest net buyers of Treasury debt from March 2020 through March 2022 and now has reversed direction.

- US banks.: Banks began shedding Treasury balances in August at a pace so far of roughly $35 billion a month. Banks hold Treasury debt largely to meet regulatory or management liquidity targets or in the absence of better investments. But banks this year have steadily lost deposits, driving down investment liquidity needs, and have seen good loan demand, reducing the need for investment securities. Banks expect deposits to continue rolling off and loan demand to continue well into next year.

- Fixed income mutual funds. Mutual funds have a well-known boom-and-bust exposure where good performance leads to investor inflows and bad performance reverses the tide with a vengeance. With the Bloomberg Barclays US Aggregate Bond Index down by 16.8% this year, mutual funds have seen steady redemptions. Only in August did funds get a reprieve after six weeks of good performance. But redemptions have returned. Investors have pulled $62 billion since mid-August, and with Treasury allocations averaging an estimated 29%, that makes for $18 billion in selling. Mutual funds will likely continue selling liquid Treasury debt along with agency MBS to fund redemptions, hoping to avoid more painful sales of less liquid assets. Funds will need a run of good performance for redemptions to stop.

- Foreign central banks. The days of strong foreign central bank buying are long gone, with the foreign official share of outstanding Treasury debt dropping from more than 30% a decade ago to slightly more than 15% today. The most recent data from Treasury show foreign central banks and other official portfolios in August sold a net $9 billion, bring total net sales for the year to more than $96 billion. Expect foreign central banks to look for marginal ways to diversify away from the US dollar.

Only foreign private portfolios have net bought US Treasury debt this year, and at a record pace. Foreign private portfolios added a net $183 billion of notes and bonds in August, bringing the year-to-date total to $655 billion. This source of net buying is likely to continue as global demand for safety and liquidity likely rises.

Even if foreign private portfolios continue their August pace in September and beyond and sellers do the same, visible selling outweighs visible buying at least until the US Treasury slows issuance in the spring. Those are big and important ‘ifs’, but the broad strokes of buying and selling line up with the latest rise in rates.

One obvious blind spot in tallying flows is the particular parts of the yield curve where the buying and selling take place. The inversion of the curve, with maturities out to five years heavily influenced by the immediate Fed path, clearly creates incentives to sell long and buy short. That might influence banks and mutual funds, adding to the tendency for longer rates to rise. But that is theory, not proof.

Fundamentals argue for lower long rates

The 10-year rate started climbing above fundamentals in August, rising with the rest of the yield curve. That makes sense for shorter rates hinged on the Fed, which has steadily announced its intention since at least Jackson Hole to hike and hold until inflation is dead. But expected inflation and real rates over the long run should anchor the long end of the curve. Both of those argue for longer rates below 3.00%.

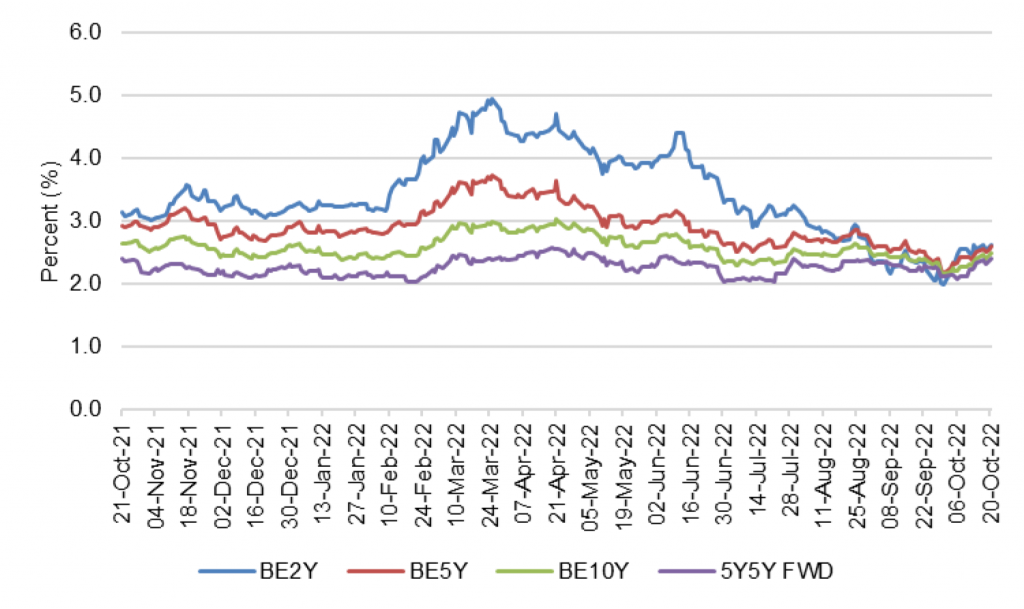

- Expected inflation. Long rates should cover the cost of average inflation over the long run, and inflation expectations have become easier to see over time. The TIPS market shows breakeven inflation over the next 10 years modestly above 2%, with the 5-year forward 5-year inflation rate priced at 2.41% (Exhibit 1). For investors concerned about liquidity and other issues that can cloud the information embedded in TIPS, recent surveys by the New York Fed show consumer inflation expectations five years from now at 2.2%. Both the market and consumers expect the Fed will beat inflation in the long run. There’s a starting point for fundamental fair value in longer rates.

Exhibit 1: TIPS anticipate inflation over the next decade slightly above 2%

Source: Bloomberg, Amherst Pierpont Securities

- Expected real rates. Long rates should also cover the expected real cost of money—the rate in the long run that clears money supply and demand. The current 5-year forward 5-year real rate is 1.7%, well above most estimates of the long-run US real rate of interest. Real rates across the curve are high, too (Exhibit 2). Unfortunately, the real rate does not get posted in the markets every day. It is only inferred. But the Fed’s current estimate of neutral fed funds is one benchmark, and that now stands at 2.5%, only 50 bp higher than the Fed’s 2.0% estimate of long-term inflation. That implies a neutral rate of 0.5%. Other approaches to estimating real rates also pin the US real rate since 2010 somewhere between 0.5% and 1.0%. Current real rates look as if the market expects the Fed to tighten financial conditions and keep them there for the next decade. If anything in the rates market is fundamentally mispriced, longer real rates are it.

Exhibit 2: Real rates look high across the curve

Source: Bloomberg, Amherst Pierpont Securities

Green shoots in the spring

It seems plausible that net selling pressure in Treasury debt will only ease after March next year as US Treasury issuance slows, making for a long and volatile winter in the Treasury market. That also coincides roughly with the first anniversary of the first Fed hikes in this cycle, a point where the Fed should be able to gauge the amount of work, if any, still needed to reign in inflation. If selling pressure eases and the market realizes the Fed will not need to keep real rates high for the next decade and beyond, the long end of the yield curve should be set to rally.

* * *

The view in rates

OIS forward rates now imply fed funds will peak around 4.85% early next year and hold through September 2023. That is roughly consistent with the September FOMC dots. But broad inflation, stoked by shelter and medical costs and tight labor, could make the Fed’s fight harder. There is still risk of repricing the Fed path.

Fed RRP balances closed Friday at $2.26 trillion, only slight above the average since June. Yields on Treasury bills into early November continue to trade below the current 3.05% rate on RRP cash. Money market funds have little alternative but to put proceeds into RRP

.

Settings on 3-month LIBOR have closed Friday at 436 bp, higher by 62 bp on the week. Setting on 3-month term SOFR closed Friday at 106bp, higher by 47 bp.

Further out the curve, the 2-year note closed Friday at 4.48%, roughly fair value based on Fed dots through 2024. The 10-year note closed well above fundamental fair value at 4.22%, so the higher yield has to get chalked up to a market seeing or expecting supply to overwhelm demand. It is shaping up to be a long and volatile winter for the rates market.

The Treasury yield curve has finished its most recent session with 2s10s at -26 bp, steeper by 19 bp on the week. The 5s30s finished the most recent session flat, steeper by 31 bp on the week. The 2s10s curve looks likely to invert by around 70 bp shortly before Fed tightening comes to an end. That is a trade for sometime next year.

Breakeven 10-year inflation finished the week at 254 bp, higher by 39 bp from a week before. The 10-year real rate finished the week at 168 bp, unchanged on the week.

The view in spreads

Volatility should continue while the Fed’s path stays in flux. It is becoming increasingly clear that the lack of Fed forward guidance and the emphasis on data has created much more uncertainty than the benchmark tightening cycle of 2004 through 2006. That makes news on growth, inflation, unemployment and policy much more important in this market. And the higher informational content adds to realized volatility. Both MBS and credit have widened steadily since mid-August. Nominal par 30-year MBS spreads to the blend of 5- and 10-year Treasury yields finished the most recent session at 173 bp, wider by 1 bp on the week. Par 30-year MBS OAS finished the week at 64 bp, wider by 2 bp on the week. Investment grade cash credit spreads have finished the week at 192 bp over the SOFR curve, wider by 5 bp.

The view in credit

Credit fundamentals have started to soften with the weakest credits showing slower revenue growth so far in 2022, declining free operating cash flow and less cash on the balance sheet. Ahead lays weaker demand, margin pressure, a soft housing market and various risks from Covid and supply interruptions. Inflation will land differently across different balance sheets. A recent New York Fed study argues inflation generally helps companies lift gross margins, although airlines and leisure may have an easier time passing through costs than healthcare, retail and restaurants. In leveraged loans, a higher real cost of funds would start to eat away at highly leveraged balance sheets with weak or volatile revenues. Consumer balance sheets look strong with rising income, substantial savings and big gains in real estate and investment portfolios. Homeowner equity jumped by $3.5 trillion in 2021, and mortgage delinquencies have dropped to a record low. But inflation and recession could take a toll and add credit risk to consumer balance sheets.