The Big Idea

Causes and solutions of a chronic housing shortfall

Laurie Goodman | September 23, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

The US faces a chronic housing shortage that has built up since the Global Financial Crisis and become acute with the pandemic. The math is simple: household formation has simply outstripped production. And the effect is felt in home prices and rents and the availability of good housing. But there is growing awareness of the supply shortage, and that has set state and local governments in motion to relax restrictions and allow more units on less land and with more efficient building methods. Lending markets have opportunities to improve financing of accessory dwelling units and manufactured housing, and to ease funding for renovating and preserving houses. For builders and lenders and the debt and equity that support them, the strains in lending present opportunities to fill these financial gaps.

Quantifying the imbalance between housing supply and demand

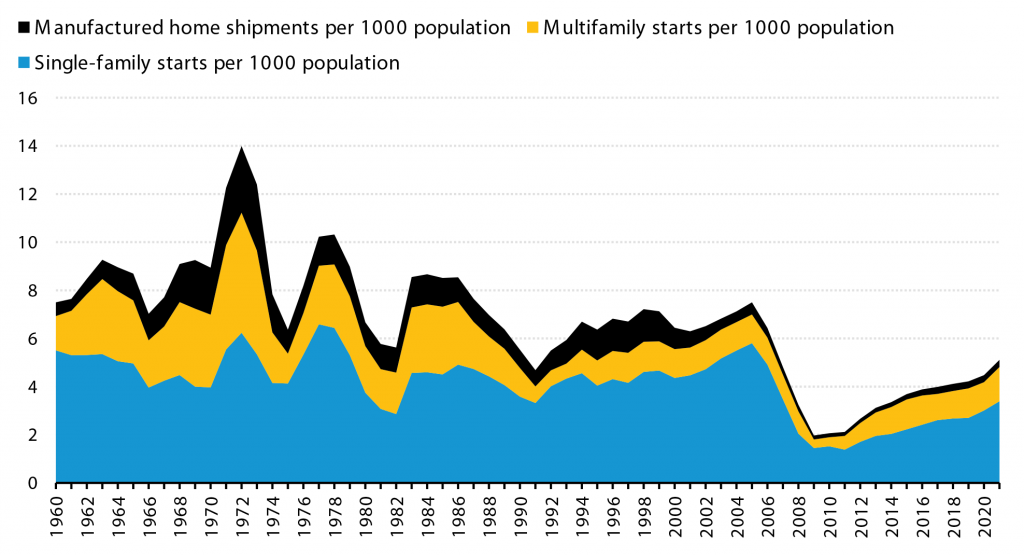

The housing market faces a shortage of millions of homes. And that shortfall comes through clearly simply by looking at trends in the number of housing units built for every 1,000 people. That number stood at 5.1 at the end of 2021, the result of 1.69 million units produced for a population of 331 million. While that pace is up from very low levels just after the Global Financial Crisis, it still stands well below the average of 7.8 units built for the 48 years from 1959 to 2006. The numbers also show that single-family units have recovered very slowly and still run well below levels of the 1990s and early 2000s. And multifamily units, while much lower than in the 1960s, 1970s and early 1980s, have accelerated to their highest pace since the passage of the 1986 Tax Act, which eliminated some of the favorable tax breaks for investment properties.

Exhibit 1: Population-adjusted housing production falls below historic averages

Note: population-adjusted construction is single-family (1-4) units plus multifamily units plus manufactured housing built per 1,000 population.

Source: Urban Institute calculations from U.S. Census Bureau data.

Other estimates of housing shortfall also paint a striking picture. Freddie Mac’s chief economist Sam Khater and his team argue that the underbuilding of single-family and multifamily homes by the end of 2021 left a shortage of 3.8 million units. Ken Rosen and his team from Rosen Consulting Group use the long-run annual rate of construction from 1968 to 2000 to argue that the cumulative building from 2001 to 2020 still fell short by 5.5 million. Stephen Stanley, elsewhere in this special issue, estimates a shortfall at the end of 2021 of at least 2.5 million units. And a range of work shows the shortfall affecting all parts of the market. Supply falls short in homes for 1-4 families, broadly labeled single-family homes, as well as multifamily homes. All estimates point in the same direction for all key sectors of housing.

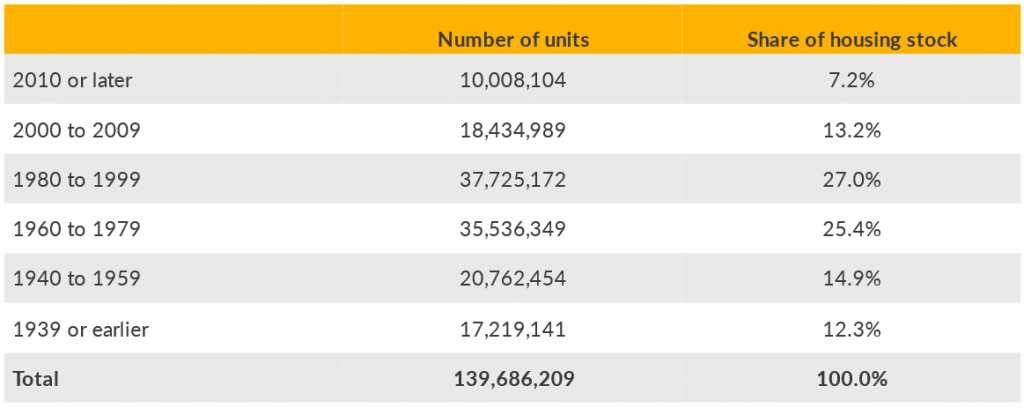

Discussions of shortfalls in housing supply usually give short shrift to the number of homes falling out of use every year, but that is missing an important and growing opportunity. The US housing stock is aging quickly. The median home was built in 1978 and turns 44 this year (Exhibit 2). This means that preservation of existing homes will become increasing important in the years ahead.

Exhibit 2: The US has an aging housing stock

Source: 2019 American Community Survey.

To drive home the importance of preservation consider the following. In 2021, builders completed 1.34 million new housing units to push total US units at around 140 million. It is unclear exactly what annual obsolescence rate to use, but even a rate of 0.333% (one third of 1 percent), that would suggest 462,000 homes going obsolete each year, leaving net production under 900,000. An obsolescence rate of 0.4%, would suggest 560,000 homes going obsolete, bringing the net annual addition to 780,000. if the obsolescence rate is 0.5%, that would suggest 700,000 homes going obsolete, cutting the net annual addition to the housing stock by more than half. We don’t have good data on the obsolescence rate, but these numbers seem very conservative.

Policymakers and others have put some focus on increasing the supply of multifamily homes. Policy and trade groups have emphasized the obstacles to multifamily construction, including zoning restrictions that are more stringent for multifamily than for single-family units, impact fees and complex permitting processes. Housing advocates have also generated considerable support for increasing the low income housing tax credit, the primary government program available to address the shortage of affordable rental housing through the creation and preservation of affordable units in underserved markets.

But the supply shortfall in single-family homes has received little focus, and that is a bigger part of the housing stock. According to the 2021 American Community Survey, 77% of the nation’s housing stock is 1-4 unit structures, 18% is multifamily and 5% is manufactured homes. Single-family homes comprise close of 70% of all new housing starts. Because it such a large part of the market, the focus here will fall on single-family homes, particularly affordable single-family homes where supply shortage is the most acute I the affordable sector.

Causes and solutions to the supply shortage

The supply shortage in housing reflects a few stubborn constraints: restrictive zoning regulations, excessively stringent building codes, high cost of construction labor and materials and financing constraints for housing construction and preservation. Just as there is on single cause, there is no single solution. Rather, there is a long list of solutions, each of which will help, and none of which will “solve” the problem.

Restrictive Zoning

Zoning laws came about to allow state and local governments to regulate land use within their borders. While zoning can clearly improve quality of life—very few people want a huge factory next to their home—excessively restrictive zoning contributes to the housing supply shortage. Ordinances in many states and localities put priority on detached single-family construction over higher density housing. But even then, not all single-family construction gets treated the same. Certain types of affordable single-family housing such as manufactured homes and accessory dwelling units, or ADUs, are either banned or burdened by regulation to the point of an effective banned. Minimum lot size, minimum square footage or requirements for special permits adds to costs and delays. In much of the country, we simply need to increase the density of new single-family units and pivot to lower cost alternatives to traditional site-built housing.

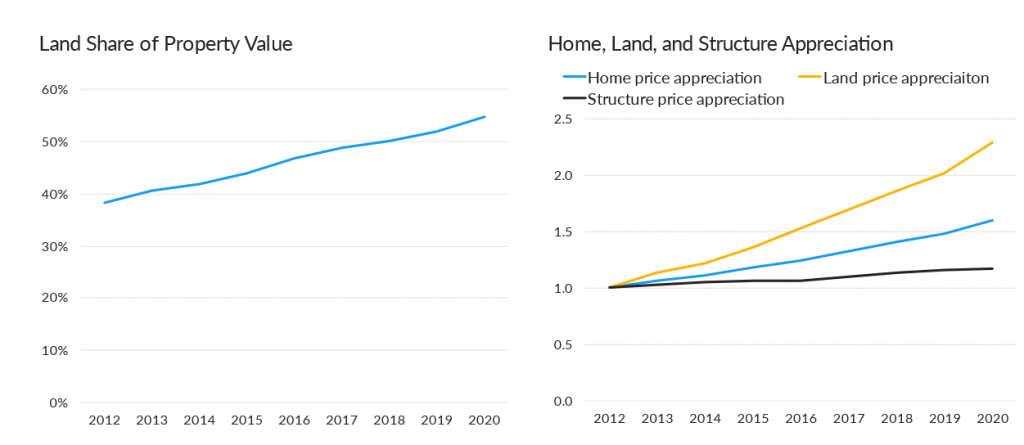

The lift from denser housing comes in part because land costs have increased far more than the costs of the structures—in part due to zoning rules. Land has become an increasingly large share of the value of the property. This strongly suggests that one key to more affordable housing is more intensive land use. Building homes on smaller lots to maximize land use would help considerably.

Exhibit 3: Land prices are an increasing share of total housing construction cost

Source: American Enterprise Institute (AEI) and Urban Institute calculations.

Zoning has particularly restricted two single-family affordable products that certainly would allow more intensive land use: ADUs and manufactured housing. It is worth highlighting the particulars of each.

- Alternative dwelling units

ADUs are small, second housing units on the same grounds as a single-family home. They can include backyard cottages, basement apartments or garage conversions. Historically, most single-family residential zones in the US prohibited ADU construction, or included rules that made it difficult to build these units. But today, while zoning remains a barrier to ADU construction in most parts of the country, some cities and states are increasingly permitting ADUs to be built in single-family zones as a matter of right. Bottom line: this is considered politically acceptable higher density.

California and Oregon as well as the cites of Minneapolis, Seattle, Austin, Texas, and Burlington, Vermont, now permit ADUs in single-family zones as a matter of right. In California, if the lot is zoned for single-family use, the owner can build and rent out an ADU on the property, and restrictions on lot coverage, and minimum lot size are prohibited. Parts of structures such as storage units and garages can be turned into ADUs. Setbacks are no longer required, or are limited for four feet, increasing buildable space. Fire code setbacks still apply. An ADU is not required to have parking if it is within a half mile of public transit, is part of a proposed of existing primary residence or is in a historic district. And an ADU can be built even if the homeowners association restricts or prohibits it; it can also be built in a historic district, and can be added to homes subject to historic preservation. Many other cities allow these structures, but with restrictions.

Currently, as Freddie Mac pointed out there are 1.4 million ADUs and 85.6 million detached single-family homes in the US. That is, 1.6 percent of homes have an ADU. As more cities allow ADUs by right, we would expect production to increase.

- Manufactured housing

Manufactured housing is the most affordable form of housing. The US Census estimates the sales price of a new manufactured home in 2021 was $108,000 excluding land. These units had an average size of 1,497 square feet, resulting in a cost of $72 per square foot. By contrast, site-built housing averaged $365,904 excluding land, with an average square footage of 2,544, for a cost of $144 per square foot—more than twice the price of manufactured housing.

Despite this, zoning in many areas has become increasingly hostile toward manufactured homes. These zoning restrictions can take the form of excluding manufactured housing completely, excluding manufactured housing on land zoned for single-family or requiring a larger lot size for manufactured housing than for other single-family homes. One result of this: developers have built very few manufactured home communities since 2000, and the number of units shipped today—around 100,000 a year during the 2018-2021 period—is much lower than it was in the 1977-1994 period—an average of 240,000 a year.

Fannie Mae notes that these zoning rules are routed in a preference for municipalities wanting to maintain certain aesthetics that are typical of traditional, site-built homes. But manufactured homes today are higher quality than ever before, and, in many cases, cannot be differentiated from their site-built counterparts; they may have pitched roofs, front porches, and decorative windows and trims. A re-evaluation of zoning codes with respect to manufactured housing is critical.

With land costs rising much more quickly than the cost of structures and becoming an ever more costly input, more intensive land use is required to promote more affordable housing products such as ADUs and manufactured homes. Zoning changes are key to this.

Restrictive Building Codes

Building codes also have become much more restrictive over the past decade. The National Association of Home Builders estimates that total regulatory costs Including loss development and structure construction phases account for nearly 24% of the price of a finished home. Using the census median sales price of $440,000, this comes to $105,000 for each home. These costs cover zoning approvals, compliance and delay costs, environmental reviews and the cost of land left unbuilt. Nearly half is regulatory costs incurred while building the structure, with building code enhancements implemented over the last decade as the single largest item

These costs do protect public welfare, but the competing interest is affordability. Rolling back these enhancements may be seen by some to be seen as weakening building safety and resilience. But perhaps the cost reductions justify having marginally less resilient structures; and perhaps the new performance goals could be met with lower cost materials and practices, rather than continued accretion to codes.

There does not seem to be a clear way to determine which building code enhancements make sense and which do not based on costs and benefits. It is clear that it is untenable to continue to add rules with no sense of cost as it is limiting the supply of available housing.

High cost of construction labor and materials

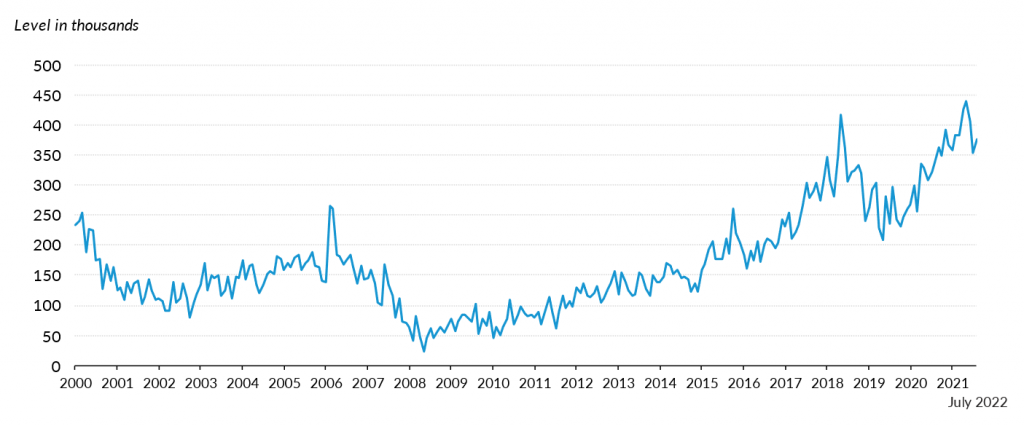

The shortage of construction labor and the rising costs of materials increases the costs of building new homes and rehabilitating and preserving existing homes. The rising labor costs reflect generally rising wages, as well as two industry specific factors: many workers left the industry in 2008, and a very high proportion of the industry is foreign born, with curbs on immigration affecting this industry more than most. Nationally, about 17% of the labor force is foreign-born, but that share is 32% of the construction industry. The result: construction job openings are at a near all-time high (Exhibit 4).

Exhibit 4: Construction job openings are near historic highs

Source: US Bureau of Labor Statistics Job Openings and Labor Turnover Survey.

Communities can cut construction costs by building smaller units or reduce labor costs with more efficient construction. Factory-built housing is just less expensive than site-built homes. Costs drop in part because of automation, economies of scale and because factories can run in all weather. And costs drop, too, because products are standardized for less waste.

It is important to realize that despite these efficiencies, modular, panelized and precut homes account for a dwindling share of total single-family completions. In the 1990s and early 2000s, these homes accounted for 6% to 7% of annual single-family completions. But now the number is just 3%. In 2020, builders completed only 28,000 modular, panelized and precut homes compared with 912,000 site-built homes.

The use of modular, panelized and pre-cut housing could be expanded if these products could be built to federal standards, rather than state and local standards. Currently manufactured homes are built to HUD standards, they are not subject to state and local standards. Modular, panelized and pre-cut homes are treated like site-built homes, subject to state and local standards and inspections. Even when a factory-built home is “inspected” in a factory in a given state, the approval is generally not valid in other states. Building to federal standards would increase economies of scale and the use of these products.

Financing issues

An additional issue is the difficulty of financing the construction and preservation of housing in general, and especially affordable housing. While the cost of land, materials and labor has gone up, builder access to financing has gone down. A few areas make the case:

- Acquisition development and construction lending

Bank acquisition development and construction lending, or AD&C, is an especially important source of financing for smaller builders. These market participants often do not have access to other forms of financing. Big homebuilders often rely on the bond markets. Banks have been pulling back on AD&C loans since the Global Financial Crisis and show few signs of expanding access. In fact, both the Federal Reserve’s Senior Loan Officers’ Survey and the National Association of Home Builders survey on AD&C financing show further tightening so far in 2022. Banks often note that this is the result of increased regulatory scrutiny for this type of lending.

The retreat in AD&C reverberates across the system: smaller builders are often those that specialize in the more affordable units, exacerbating the shortage in the most vulnerable sector of the market. Moreover, with limited financing, builders focus on their most profitable opportunities first, and this is larger, more expensive homes. While the median number of square feet in new homes has started to level off lately, the increased new home amenities have more than offset this modest decline.

Regulators and the private market could make a difference in the AD&C story. A re-evaluation of this risk by regulators is certainly in order. Beyond regulators, as other real estate lending markets, particularly since traditional mortgage lending is down, this could be a business for non-bank entities to explore.

- Manufactured housing

Manufactured homes can be titled as personal property, referred to as chattel, or as real estate. Mortgages on real estate, which require the borrower to own the land, are available at rates only marginally higher than site-built homes and on very similar terms. But chattel loans carry much higher interest rates and shorter terms, such as 20 years rather than 30 years. For borrowers that do not own the land—the home is in a manufactured home community, where a third of manufactured homes sit, or is on rented land or family land that cannot easily be encumbered for a mortgage—a chattel loan is the only option. Moreover, some borrowers opt for a chattel loan even when they own the land because the application process is quicker and applicants are less likely to be denied financing.

There is effectively no government financing for chattel loans. Fannie Mae and Freddie Mac do not have programs that accommodate chattel loans, and the FHA program (Title 1) is not really working; FHA finances only a handful of loans a year. FHA and Ginnie Mae are currently looking for ways to improve the program. The GSEs have discussed adding a chattel program but have not done so, although a pilot may be forthcoming. A GSE program, when scaled, would improve financing to this sector.

- Alternative dwelling units

Even in those relatively few areas where ADUs are allowed as a matter of right, financing remains an issue. Mortgage underwriting to build an ADU generally does not take into account either the expected rental income the unit will generate or the value of the improvements. Mortgage loans are generally made on the “as is” market value of the property. That is, with traditional financing such as cash out refinancing or home equity lines of credit, the loan is made on the before-repair market value of the home. To get “credit’ for the repairs in an initial loan, the borrower must use renovation financing; these loans are cumbersome, restrictive and have a high denial rate. More concretely, the 2021 HMDA data show a denial rate for rehab loans of 38.8%. This compares to denial rates of 13.4% for purchase and rate/term refinance loans and 16.6% for cash-out refinancing.

- Renovations

Cumbersome renovation programs affect not only ADUs but all renovation efforts. With an aging housing stock, home preservation becomes increasingly important. And although the GSEs and FHA have rehabilitation and renovation lending programs, they are far from optimal. The FHA offers structural renovations through their 203(k) program, but the borrower must hire a HUD consultant to oversee the renovation. Fannie and Freddie do not require the borrower to hire a consultant for major repairs, but the GSEs have recourse to the lender for the risks of project non-completion, cost overruns and poor-quality repairs. This naturally limits lender participation.

Freddie Mac has a new program, CHOICEReno EXPress, which began on November 1, 2021 for more limited renovations or repairs of up to 15% of the purchase price in high-needs areas and 10% in other areas that will not require lender recourse. Buyers can use this program at the time of home purchase, and it requires an appraisal of the after-repair market value of the property at the time of application. This new Freddie Mac program is a step in the right direction: it is more streamlined than the traditional Fannie Mae and Freddie Mac programs, and without lender recourse; the hope is that more lenders will participate in the program. Freddie Mac hopefully will provide an update on market response.

More fundamentally, while these renovation programs could be tweaked to make them easier to access and lower the denial rate (expanding Freddie’s new program for example), the only real solution is a complete overhaul. Homeowners are often lack the knowledge and expertise to carry out major renovation projects. The GSEs and FHA must select a few approved contractors that have agreed to do repairs at a fixed price, maintaining quality; the borrower would choose from this limited menu. The prospect of losing the GSE or HUD approved status would give contractors a strong incentive to carry out the work on schedule and within budget.

Meeting the affordability challenges

Waiting for demographics to solve the housing supply problem will take decades. The rate of population growth is slowing; census results show the population grew by 13.2% from 1990 to 2000, 9.7 percent from 2000 to 2010, 7.3 percent from 2010 to 2020, and census projections indicate that it expected to grow by 6.5% from 2020 to 2030 and 4.9 percent from 2030 to 2040. Assuming that the number of people per household remains roughly constant, the number of additional families being added per decade will decline, albeit more slowly. We added about 8.5 million households from 2010 to 2020; this analysis would suggest 8.12 from 2020 to 2030, 6.58 from 2030 to 2040. This will in turn require less additional housing per year, potentially alleviating supply pressure. But the timeline is such it will be like watching paint dry. Supply should be the critical housing focus.

As Stephen Stanley points out in this issue, an acute housing supply shortage and a recent surge in demand has increased prices. But even larger forces are at work. While higher interest rates will cool the housing market going forward, there is clear need to increase housing supply, especially affordable supply. There is a litany of ways to do it. There are opportunities for builders and lenders to solve the affordable supply shortage, the single largest challenge in the housing market. With big solutions come big rewards.

Laurie Goodman is a housing and mortgage finance analyst in New York.