The Big Idea

Summer camps

This material is a Marketing Communication and does not constitute Independent Investment Research.

The market has split into two camps this summer. Camp Inflation believes the Fed will need to fight persistent inflation at all costs. Camp Growth believes the Fed will pull up short if growth suffers too much. For now, Camp Growth looks like it is winning the tug-o-war based on fed funds futures showing a tighter Fed into early 2023 and an easier one shortly afterwards. But Camp Inflation looks right. And that is a recipe for rate and spread volatility, raising the cost of holding and rebalancing risk. Market liquidity is showing the effects.

The Fed in the last week has tried to rally Camp Inflation:

- “I think we’re going to have to see convincing evidence across the board—headline and other measures of core inflation all coming down convincingly—before we’ll be able to feel like we’re doing enough and we’re doing a good job.” – James Bullard, FOMC voter and president of the St. Louis Fed, on August 3 after calling for fed funds of 3.75% to 4.00% by the end of this year.

- “We’re committed to getting inflation down.” – Loretta Mester, FOMC voter and president of the Cleveland Fed, on August 4, after restating the Fed’s 2% inflation target and arguing for more rate increases.

- “Nowhere near done.” – Mary Daly, San Francisco Fed president, on August 2, commenting on the path from current policy rates to a Fed pause.

These remarks echo Fed Chair Powell’s suggestions that stable prices could come at the cost of recession and rising unemployment.

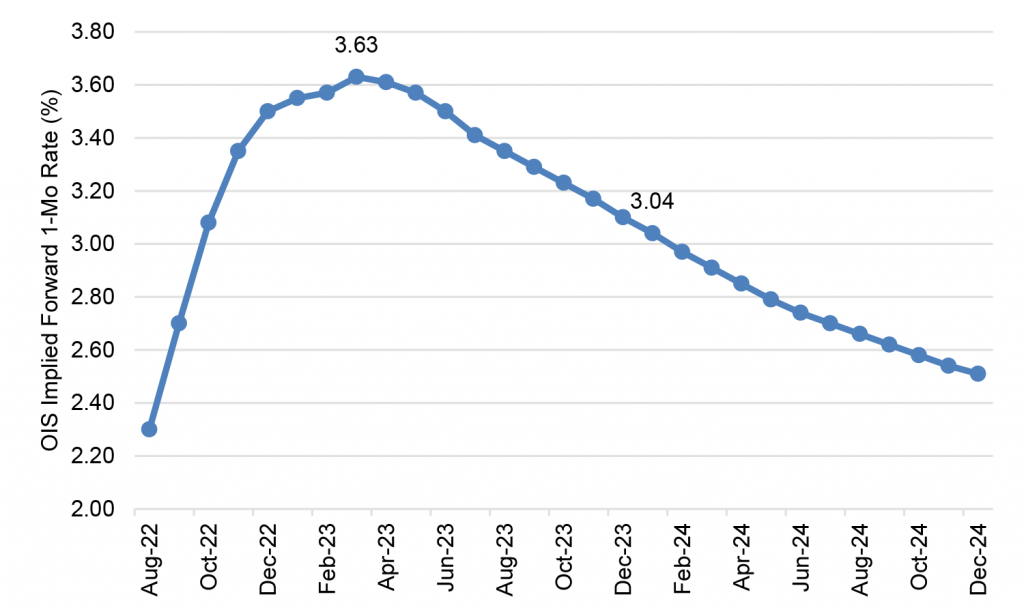

Camp Growth isn’t buying it, even after Friday’s release of June’s 528,000 in new jobs. Implied forward fed funds finished Friday showing a peak rate of 3.63% in March next year, with the rate dropping to 3.04% by the end of the year.

Exhibit 1: Implied fed funds see a tighter Fed into early 2023, easier afterwards

Note: 1-month forward rates from the 8/5/2022 closing OIS curve.

Source: Bloomberg, Amherst Pierpont Securities

The current implied path of fed funds only makes sense if the Fed pivots to focus on slower growth or if inflation collapses. The Fed’s concern about growth in 2008, in 2018 and in 2020 feed Camp Growth’s faith that the Fed will pivot. But the Fed in those episodes had inflation well under control and could afford to pivot. That is not the case this time. Inflation is broad and looks persistent with momentum behind rising prices especially for shelter and labor. Falling prices for food and energy could bring headline CPI down in short order, but core and PCE look unlikely to tumble.

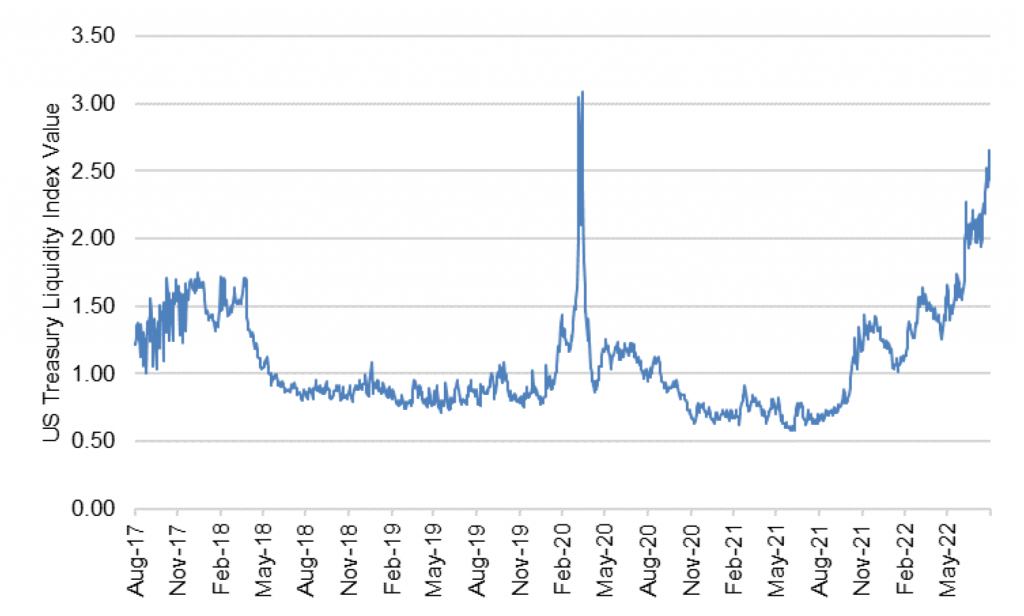

A flow of contradictory information—payrolls and inflation readings rallying Camp Inflation, GDP rallying Camp Growth—have pushed realized and implied volatility up and made it difficult to hold and rebalance risk. Liquidity has eroded in the Treasury market (Exhibit 2). It has eroded, too, in MBS and in investment grade corporate debt, too. Lower trading volumes, wider bid-ask and more price sensitivity to large flows have raised the cost of responding to new information and added risk to the markets.

Exhibit 2: Treasury liquidity is closing in on March 2020 levels

Note: The index reflects the average difference in yield between US Treasury issues with a 1-year or longer maturity and the intra-day Bloomberg relative value curve fitter. In liquid markets, deviations go away quickly, and index values are low. In illiquid markets, deviations persist, and index values are high.

Source: Bloomberg, Amherst Pierpont Securities.

The only portfolios with reliable appetite seem to be those insulated from mark-to-market risk. Insurers continue to invest steadily and the lending side of banks continue to grow at the fastest pace in years.

For the public markets to regain their footing, the tug-o-war between Camp Inflation and Camp Growth has to get resolved. There’s a good chance that will happen this fall, nearly six months after the Fed’s first hike. At that point, the two camps on either end of the rope will see the long and variable effects of Fed policy. If inflation persists, the market should reprice rates even higher in the front of the curve. If inflation starts to fall, intermediate rates should start to fall. In either case, volatility should start to drop and risk assets should get a reliable bid again.

* * *

The view in rates

Even though the 2-year note closed Friday at 3.23%, it still looks rich while the 10-year note looks like it is in the neighborhood of fair value. The 2-year rate should approach 3.50% assuming a Fed more concerned about inflation than recession. Fair value at 10-year and longer maturities still looks solidly in the neighborhood of 2.50%, but the possibility of a sustained fight with inflation may require compensation above fair value even in long maturities. The 2s10s curve looks likely to invert by around 70 bp before Fed tightening is over.

Fed RRP balances closed Friday at $2.19 trillion, roughly the average since mid-June. Yields on Treasury bills out to early October trade below the current 2.30% rate on RRP cash. Money market funds have little alternative but to put proceeds into RRP.

Settings on 3-month LIBOR have closed Friday at 286 bp. Setting on 3-month term SOFR closed Friday at 263 bp.

The 10-year note has finished the most recent session around 2.83%, up 18 bp on the week. Breakeven 10-year inflation finished the week at 247 bp, down 8 bp from a week before. The 10-year real rate finished the week at 35 bp, up 25 bp on the week.

The Treasury yield curve has finished its most recent session with 2s10s at -40 bp, inverted another 16 bp on the week. The 5s30s finished the most recent session at 11 bp, flatter by 22 bp on the week.

The view in spreads

Persistent volatility should make it hard for risk spreads to tighten, MBS should still outperform credit as the Fed tightens and growth slows. Nominal par 30-year MBS spreads to the blend of 5- and 10-year Treasury yields finished the most recent session at 125 bp, wider by 10 bp on the week. MBS OAS, on the other hand, continues to slowly tighten, suggesting good net demand. Par 30-year MBS OAS finished the week at 12 bp, wider by 4 bp on the week. Credit spreads seem insufficient to cover the spread volatility likely as growth slows and concern about recession grows. After nearly two years of better performance in credit, the tide should start to turn toward MBS.

The view in credit

Credit fundamentals should soften as the Fed dampens demand and growth begins to slow. In some quarters, the conversation has turned from whether recession will arrive to the shape of recession once it does. Corporations have strong earnings for now, good margins for now, low multiples of debt to gross profits, low debt service and good liquidity. It will be important to watch inflation and see if costs begin to catch up with revenues. A recent New York Fed study argues inflation generally helps companies lift gross margins. A higher real cost of funds would start to eat away at highly leveraged balance sheets with weak or volatile revenues. Consumer balance sheets look strong with rising income, substantial savings and big gains in real estate and investment portfolios. Homeowner equity jumped by $3.5 trillion in 2021, and mortgage delinquencies have dropped to a record low. But inflation and recession could take a toll and add credit risk to consumer balance sheets.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.