The Big Idea

Sailing a bank through the Fed cyclone

Tom O'Hara, CFA | July 29, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

This year has been one of the most volatile periods for interest rates in at least a decade. Higher rates and wider spreads have left most fixed income assets underwater, including bank securities portfolios, and surging loan demand has turned up the pressure on economic capital. While higher rates have helped most bank earnings, a quick reversal caused by a recession could damage future earnings. Higher rates have also made bank deposit funding more expensive and harder to retain, forcing banks to start considering wholesale funding alternatives. Bank management now faces a series of choices for mitigating capital, credit and funding risk.

Bank capital deterioration

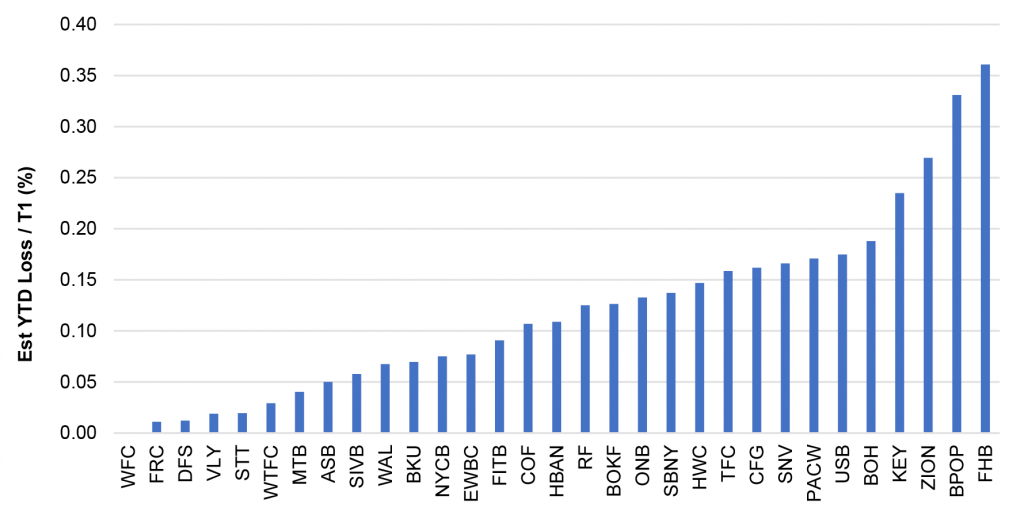

This year’s sharp rise in interest rates along with a broad spread widening for most credit asset classes has led to a significant drop in the value of banks’ loans and securities, putting pressure on capital. A sample of larger banks through June show a median estimated available-for-sale (AFS) loss of 12% as a share of Tier 1 capital (Exhibit 1). The majority of bank securities sit in the AFS portfolio, meaning the bank can sell those securities at any time if it needs liquidity. AFS portfolios are marked-to-market with changes in value reflected in the bank’s equity position. Tier 1 capital is primarily comprised of the bank’s common equity

Exhibit 1: Estimated loss this year in AFS as a share of Tier 1 capital

Source: S&P Capital IQ, Amherst Pierpont Securities

Banks have several ways to address this issue ranging from adding 0% risk-weighted assets (RWA), allowing assets to run off, executing a credit risk transfer transaction, selling assets or raising equity. Of the most plausible ways to relieve capital pressure, adding assets with a 0% risk weighting seems the most efficient.

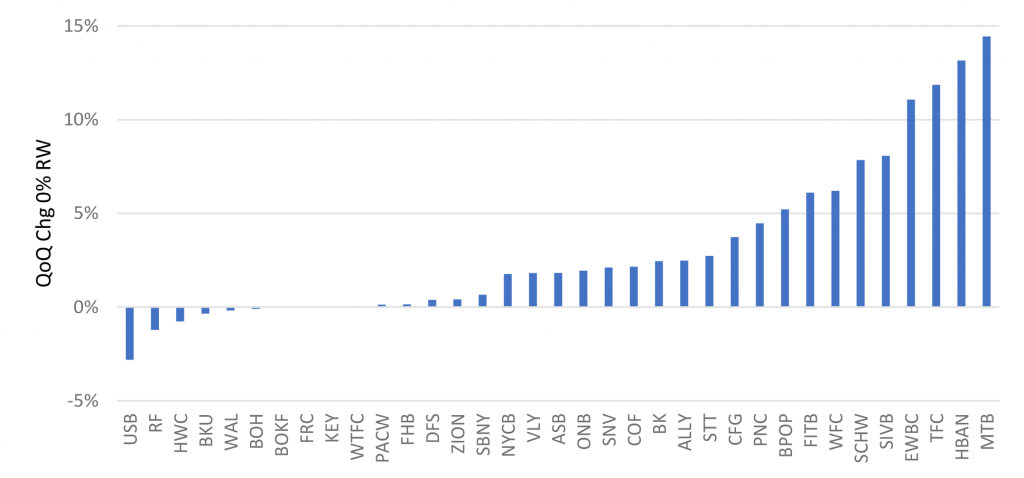

With wide nominal spreads to the Treasury curve in MBS and spreads at fair value between conventional and Ginnie Mae MBS at fair value, Ginnie Mae MBS look like a good solution for adding 0% RWA. Most investors know bank regulators assign risk-weights to different assets depending upon their perceived credit risk. US Treasury debt and Ginnie Mae MBS carry an explicit guarantee from the federal government, and therefore are 0% risk-weight. A representative sample of large banks in the first quarter of the year increased 0% RWA by a median 1.8% against a median decline in overall securities portfolio size of 3.2% (Exhibit 2).

Exhibit 2: A healthy rise in 1Q22 in 0% risk-weighted assets

Source: S&P Capital IQ, Amherst Pierpont Securities

Allowing assets to run off may seem like the easiest strategy for a bank to pursue, but recent loan demand has made it difficult to trim overall asset balances. The Fed’s H.8 released on July 15 shows an annualized 2.6% reduction in US commercial bank securities portfolios in June although total bank credit rose by an annualized 9.9%.

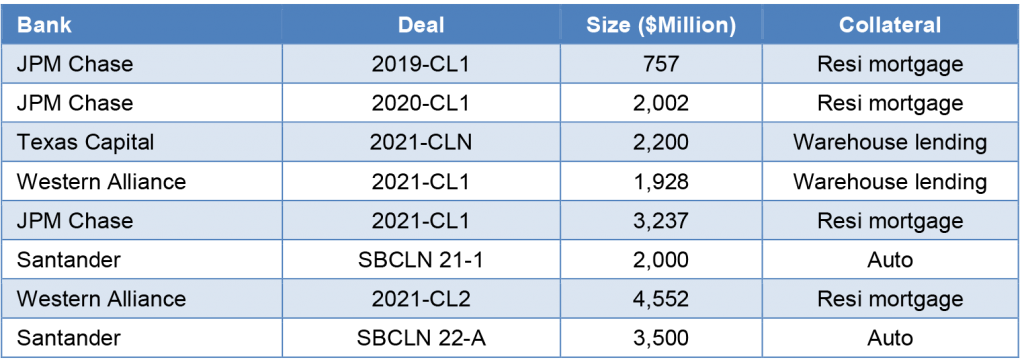

More banks are considering Credit Risk Transfer (CRT) structures for regulatory capital relief, designating balance sheet assets and transferring junior risk to capital markets investors (Exhibit 3). Most securitizable asset classes could be considered for a CRT structure, and more regional banks are now coming into the space as the benefits of these transactions become more well-understood.

Exhibit 3: Recent bank credit risk transfers

Source: Amherst Pierpont Securities

While selling assets could be an effective strategy for improving capital ratios, banks generally should not want to part with higher-yielding loan assets nor should they want to give up their customer relationships. This is why the H.8 continues to show growth in loan portfolios.

Finally, banks could raise equity to improve their capital ratios. This would typically be the last option for a bank, as equity is the most expensive part of their capital composition. Also, raising new equity dilutes existing shareholders, which would not make most equity investors or analysts happy.

Recession concerns rising

Banks are starting to prepare for both the credit risk and interest rate risk that a recession may bring. To prepare for credit risk, banks are starting to add to credit loss reserves, and they could additionally consider suspending capital distributions and selling weaker assets. Banks should also evaluate CRT transactions.

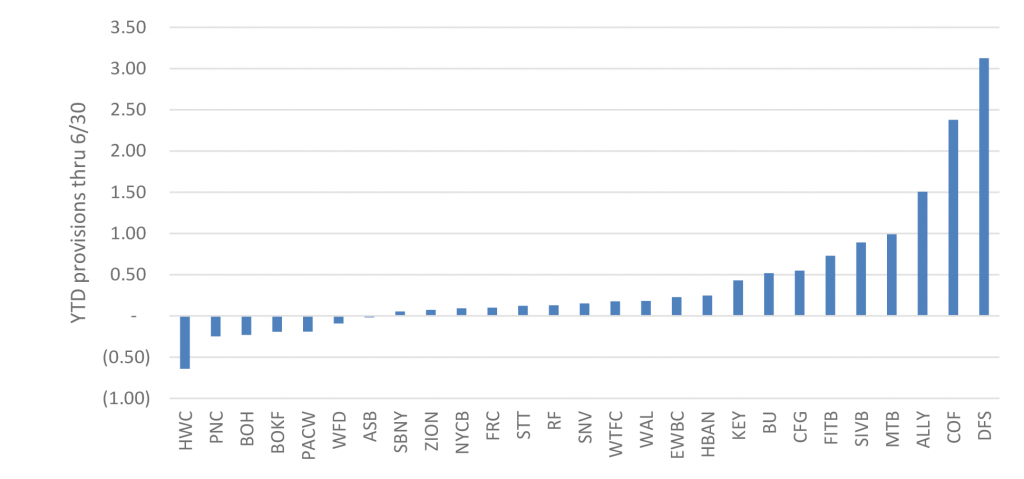

Regarding loss reserves, banks have generally been adding provisions year-to-date, partially due to strong growth in loan portfolios and partially due to heightened recession-related credit concerns (Exhibit 4, some 2Q22 numbers not yet available).

Exhibit 4: Year-to-date provisions on the rise

Source: S&P Capital IQ, Amherst Pierpont Securities

Suspending distributions to preserve capital is an option but, similar to issuing equity, unlikely to make equity investors and analysts happy. Suspending distributions is more likely to occur when a bank is already in trouble and less likely to be used as a preventive measure.

Selling weaker assets is also an option but not recommended as banks should not want to part with higher yielding loan assets or the related customer relationship.

A CRT transaction is one effective way for a bank to reduce credit risk, in addition to the capital benefits mentioned earlier. For 50% RWA such as prime quality residential mortgages, the bank would typically sell the bottom 5% of the capital structure to lower RWA to the minimum 20% and minimize most of the credit risk of the reference portfolio in most reasonable scenarios. The CRT also allows the bank to retain most of the earnings and all of the customer relationships.

Many banks are also expecting lower rates in a recession, a potential hit to earnings as most banks are asset sensitive—asset coupons resetting more quickly than liability coupons. Some banks have choices here between securities with longer duration, modifying loan structures or using derivates to add convexity to the balance sheet.

While banks have historically been buyers of shorter-duration CMOs, they should consider adding more 30-year pass-throughs to extend the duration of their securities portfolios. As mentioned earlier, nominal spreads on pass-throughs are wide, and Ginnie Mae MBS provide the added capital benefit of being 0% risk-weight.

Loan structures may be modified to include interest rate floors and collars. This is a simple method to add balance sheet duration and reduce asset sensitivity.

Finally, banks should consider using derivatives to supplement their overall rate risk strategy. A couple of the more common strategies used by banks are to use cash flow hedges of floating-rate coupons, either a receive-fixed swap to hedge floating rate assets or a pay-fixed swap to hedge floating rate liabilities. Both of these will add to a bank’s duration of equity and provide benefit when rates decline.

Deposit costs rising, more capital markets funding coming

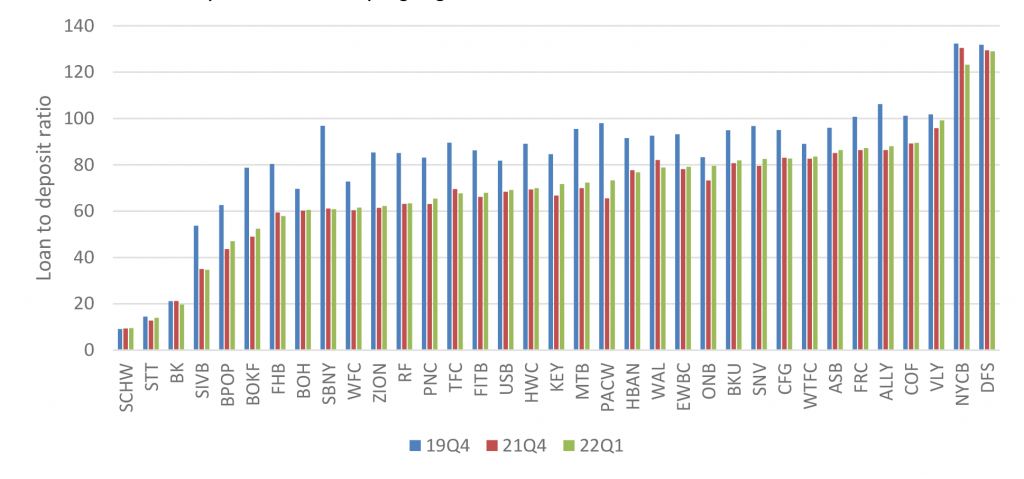

Along with rising interest rates come rising deposit betas and loan-to-deposit (LTD) ratios (Exhibit 5). LTDs are starting to rise and are expected to return to the more historical averages such as those we saw at the end of 2019:

Exhibit 5: Loan-to-deposit ratios creeping higher

Source: S&P Capital IQ, Amherst Pierpont Securities

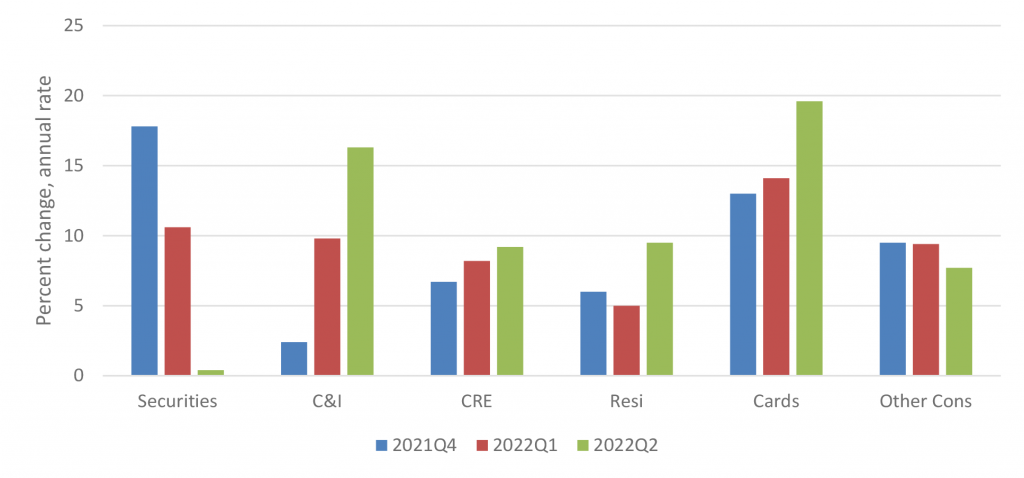

Adding to the potential wholesale funding need is the fact that banks are currently enjoying strong loan growth in most categories, while securities portfolios are stagnant (Exhibit 6).

Exhibit 6: Balance sheet component growth, annual rate

Source: Federal Reserve H.8 7/22/22, Amherst Pierpont Securities

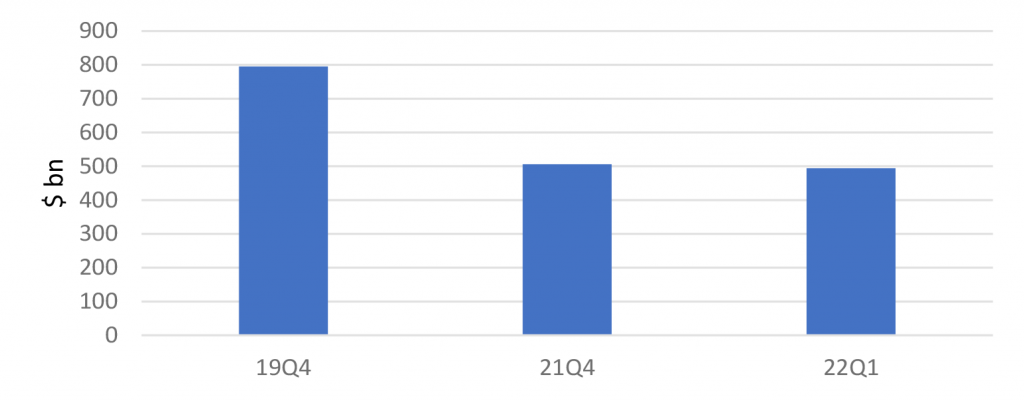

After letting more than $300 billion of senior debt mature (net) over the past two years (Exhibit 7), banks will likely supplement deposit run-off with more wholesale funding such as securities repo, FHLB borrowings, unsecured debt issuance and securitization.

Exhibit 7: Senior debt outstanding

Source: S&P Capital IQ, Amherst Pierpont Securities

Repo is an effective funding tool for securities, where haircuts may be as low as 1% to 2% for US Treasury debt, and spreads as tight as SOFR + 10 bp. For loan collateral, the FHLBanks usually provides competitive options, although collateral types are somewhat limited to real estate-related loans.

Unsecured corporate debt is a funding option that should show up more frequently over the next several months, even with spreads wide by historical standards, as corporate debt allows the bank to effectively fund its entire balance sheet at no haircut.

Securitization has not been used often by banks in recent years, but should be considered as an alternative for banks looking to remove entire asset pools from their balance sheets in order to realize an accounting gain, along with a reduction in balance sheet leverage.