The Big Idea

Help is on the way

Stephen Stanley | July 8, 2022

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

There has not been much good news on the inflation front this year. Inflation has proven broad and persistent. While the underlying pressures on prices continue, consumers have begun to see a bit of relief at the pump. Retail gasoline prices peaked in mid-June and have begun to come off rapidly. Gasoline futures point to significant further declines going forward. While core inflation is likely to remain quite high for the time being, headline inflation should begin to moderate in July while food prices and key portions of the core, such as shelter costs, likely continue to post sharp increases. The CPI may still rise substantially, albeit much more slowly than in May and June. And it looks unlikely to deter an aggressive Fed.

Pain at the pump

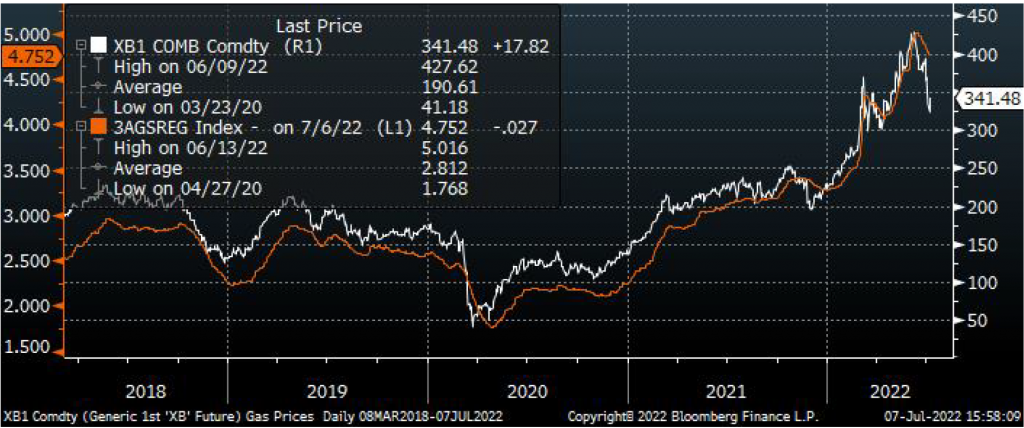

Retail gasoline prices closely track the wholesale price of fuel. The current gasoline future, which measures the wholesale price of gasoline coming into New York harbor, is a solid predictor of prices at the pump. There is a tight relationship between the current gasoline future for regular unleaded gasoline and the national average retail price for regular unleaded, as reported by AAA (Exhibit 1).

Exhibit 1: Gasoline futures compared to. AAA retail gasoline prices

Source: Bloomberg, NY Mercantile Exchange, AAA.

Retail prices track the movements in futures prices closely with a lag of usually a few weeks. The gap between wholesale and retail prices has averaged 84 cents since the beginning of 2015. Over half of that difference reflects excise taxes, 18.4 cents a gallon at the federal level and averaging about 30 cents a gallon at the state level. The rest covers the cost of transporting the fuel and other expenses of gasoline stations such as labor, rent, insurance and other things. A few states have waived their excise taxes temporarily this year, and there has been talk of Congress doing the same at the federal level, although the prospects of the latter seem improbable at this time.

Gasoline futures were already trending higher early in the year, but they spiked on February 24 when Russia invaded Ukraine. After a brief period of relief in March, which translated to a drop in retail prices in April, wholesale gasoline prices surged again in May and June, reaching an all-time high on June 9 of $4.28 a gallon.

Gasoline prices at the pump closely tracked the ascent of futures. After the brief respite in March and early April, retail prices surged for about two months before reaching the $5 a gallon mark for the first time ever in June.

The headline CPI reflected the climb in fuel prices. Headline CPI inflation surged by 0.8% in February and 1.2% in March. After a respite (“only” a 0.3% rise) in April, headline inflation reaccelerated to a 1.0% jump in May and may have risen by 1.2% in June, in large part due to soaring energy costs.

Relief!

Since the current gasoline futures price peaked on June 9, it has come off by almost $1 dollar a gallon, a steep descent. In fact, the current future closed at $3.24 a gallon on Wednesday before rebounding on Thursday.

Perhaps given the intense scrutiny from government officials, the lag in the translation from wholesale to retail prices in the current episode was extraordinarily short. In fact, the AAA national average peaked only four days after the futures price topped out. Since mid-June, retail gasoline prices have already come off by more than 25 cents a gallon to around $4.75 as of July 6.

Things could, of course, change rapidly in either direction in a matter of days, but if futures prices were to stabilize at Thursday’s close of around $3.40 a gallon for an extended period, then retail gasoline prices could be expected to fall by at least another 50 cents a gallon over the next month or two.

Implications for CPI

A conservative approach on the speed of the descent in retail gasoline prices might assume we get to around $4.50 a gallon by the end of July, $4.30 by the end of August, and $4.20 by the end of September, then the monthly averages for retail gasoline may decline on a seasonally adjusted basis by around 5.5% in July, between 3.5% and 4% in August, and about 2.5% in September.

These results would take about two tenths of a percentage point off the headline CPI in July and August and a tenth in September. After the massive increases in the CPI in May and presumably June, such relief would be quite welcome. Even so, with food prices and most core components probably remaining on steep uptrends, headline inflation is likely to remain too rapid for the Fed’s comfort over the summer, perhaps rising by close to 0.4% a month over the next three months. As it happens, such a trajectory would leave the year-over-year advance for the headline CPI barely off by September from what I expect to be a 40-year high of 8.9% in June.

While a plunge in gasoline prices will offer welcome relief to consumers and will help limit the damage on the inflation front over the next few months, I doubt that the FOMC will see anything that would justify changing course from its aggressive tightening strategy.