The Big Idea

Recession now?

Stephen Stanley | June 24, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

Fears of recession have suddenly mushroomed. There has been some evidence of slowing in a few sectors of the economy, most notably housing. But underlying momentum appears solid for the moment, led by consumer spending. Predictions of economic downturn still have been exacerbated by contraction in first quarter real GDP and by the current Atlanta Fed GDPNow forecast of a flat second quarter. Based on the common definition of recession as back-to-back negative quarters for GDP, some analysts are suggesting the economy is on the cusp. The economy may be vulnerable down the road once Fed rate hikes take full effect, but in the near term it looks far from the brink of a downturn.

Clarifying first quarter GDP reading

Before delving into estimates for the second quarter, a quick review of first quarter GDP result is warranted. While the topline real GDP figure was indeed well into negative territory—currently at -1.5% annualized—underlying demand continued to expand in the quarter. In fact, real consumer spending advanced at a 3.0% annualized clip while business fixed investment surged at nearly a 10% annualized pace. My favored measure of underlying demand, real final sales to domestic purchasers, which is simply real GDP minus inventories and net exports, increased at a 2.7% annual pace in the first quarter, stronger than in either of the final two quarters of last year.

The main driver of the negative GDP reading in the first quarter was a massive widening in the real trade deficit. Imports in real terms jumped by 18% for a second straight quarter as retailers and other businesses strained to satisfy torrid domestic demand with products from overseas, hardly evidence of economic weakness! The net exports component of real GDP subtracted 3.2 percentage points from growth last quarter.

In addition, inventories were also a drag in the first quarter. Firms continued to build inventories at a rapid pace, $170 billion annualized, but that represented a slowdown from the forth quarter pace of $193 billion and subtracted about 1.1 percentage points from growth.

In short, while real GDP technically fell in the first quarter, the economy was far from contracting in a traditional sense. The other main set of indicators that the National Bureau of Economic Research, the official arbiter of business cycle dates, uses when ascertaining turns in the economy is employment and the labor market. With payrolls growing by over 500,000 a month in the first three months of the year and the unemployment rate falling by more than quarter of a percentage point from December to March, there is no way that the NBER would consider the first quarter of 2022 to be the beginning of a recession, regardless of how conditions evolved subsequently.

Atlanta Fed GDPNow

That brings us to the current quarter. As the Fed has accelerated the pace of rate hikes and financial conditions have tightened considerably, there have been a few signs of cooling. In particular, the housing sector appears to be coming off the boil. It is understandable that financial market participants, looking at the S&P 500 drop almost 25% from its January highs and interest rates rise faster than they have in decades, are worried. Similarly, consumer sentiment has plunged, as households have grown grumpy in the face of 40-year highs in inflation. Still, fears of an immediate economic downturn have been exacerbated by an outlier reading from a widely followed GDP tracker.

The Atlanta Fed GDPNow indicator is a model that researchers at the bank have published since the middle of the last decade. The idea is to project the key components of GDP by making forecasts for the monthly data that determine the quarterly output figures. Generally, some components of GDP are more straightforward to forecast than others. Personal consumption expenditures are released monthly, and the quarterly figures are simply an average of the monthly readings. The same is true for trade. In contrast, other components are not quite so easy to project. For example, there are monthly figures for inventories, but they are nominal book value readings. To get to the GDP concept of real inventories requires estimating the inventory valuation adjustment and deflator.

In any case, economists have for decades been projecting current-quarter GDP in real time. Each forecaster has his or her own methodology for predicting the various components. The Atlanta Fed GDPNow offers a more automatic process. For the 13 high-level components of GDP, the Atlanta Fed GDPNow model derives regression equations. First, the model has to predict the unknown monthly observations used to predict the GDP components. It does so by using autoregressive equations—that is, future observations of a variable are estimated based on the past behavior of that variable. Those predicted observations are in turn plugged into a model equation translating to the relevant quarterly GDP component.

Over the course of a quarterly GDP data cycle, the Atlanta Fed GDPNow estimate starts out as a pure forecast. Indeed, it is a forecast that does not consider any outside information that economists may have access to. For example, I am privy to things like automakers’ tentative production schedules that would inform my forecast early in a quarterly cycle. I may know something about the weather, oil prices, or any numbers of other outside elements that allow me to make a more informed GDP forecast than the “blind” GDPNow model. As a result, at the beginning of the quarterly cycle, the Atlanta Fed model is not especially insightful.

However, as the quarterly cycle progresses, and researchers who run the Atlanta Fed GDPNow model begin to receive monthly data to fill in the blanks, the model’s accuracy typically improves. By the end of the quarterly cycle, just before the first official estimate of GDP is released, the differences between the GDPNow estimate and those of other economists should mainly reflect relatively minor differences in the various forecasting models that economists have constructed to process the relevant monthly inputs.

Current quarter

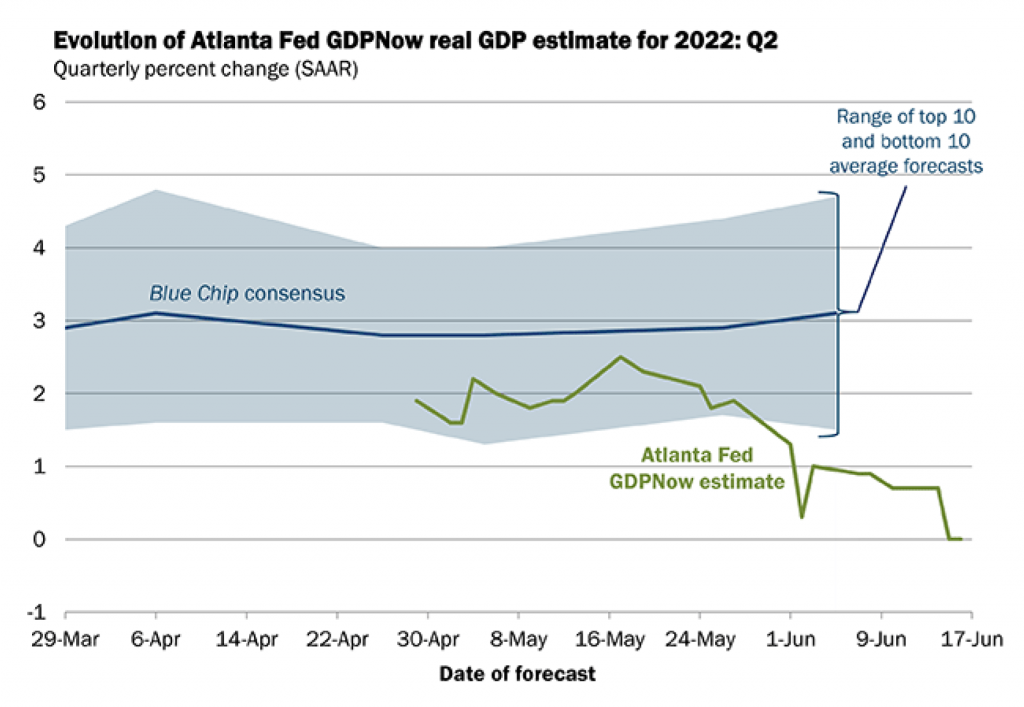

That brings us to the current quarter. From the beginning of the cycle, the Atlanta Fed GDPNow model estimate for second quarter real GDP growth has been an outlier to the downside. Exhibit 1, from the Atlanta Fed web site, shows the evolution of the GDPNow estimate versus the Blue Chip Economic survey consensus.

Exhibit 1: Atlanta Fed GDPNow vs. Private Consensus

Source: Blue Chip Economic Indicators and Blue Chip Financial Forecasts, Atlanta Federal Reserve Bank.

As Exhibit 1 shows, the Atlanta Fed GDPNow estimate started out well below the Blue Chip consensus and has only moved further downward from there. The average forecast from the June Blue Chip Economic survey, conducted about three weeks ago, was 3.1%. By comparison, my current forecast is somewhat above consensus at 4.1%

Nonetheless, many reporters and even a number of market participants deem the Atlanta Fed GDPNow estimate as an authoritative forecast, regardless of where we are in the quarterly data cycle. In the current quarter, the GDPNow figure has taken on outsized importance because it has been so weak, suggesting that the economy has a roughly even-odds chance of a second straight negative GDP reading.

In examining the differences between my forecast and the Atlanta Fed’s “Now cast,” the biggest gaps occur in the two most volatile components, net exports and trade. The Atlanta Fed model is currently projecting a drag from inventories of 1.7 percentage points and a drag from net exports of 0.1 percentage points. A third major divergence between my forecast and the GDPNow model is that I expect another strong gain in business investment in equipment while the Atlanta Fed’s model is spitting out a flat result.

Not surprisingly, I feel much more comfortable with my numbers than the Atlanta Fed’s. I would note a few points underlying my projections that the Atlanta Fed’s model would not be accounting for. On the inventory front, automakers’ latest schedules call for a 17.2% annualized surge in unit production from Q1, which ought to show up mostly in inventories (as unit sales were likely down modestly in Q2 from Q1). On trade, I suspect that the Atlanta Fed model is treating the sharp April narrowing in the trade deficit as fluky. However, an examination of the detailed import and export flows suggests that it was the explosive March widening that was the anomaly. In any case, my estimate for the May merchandise trade gap is considerably worse than the consensus (a higher deficit), and yet I am projecting a significant positive contribution from net exports to Q2 real GDP growth (close to a full percentage point). Finally, while the Atlanta Fed has the same information that I have on business investment in equipment, I struggle to understand why the model is offering a projection of a flat Q2, as core capital goods shipments in April were already substantially above the Q1 average (and core capital goods orders point to continued growth in the months ahead).

It will be interesting to see how the Atlanta Fed GDPNow model estimate evolves over the next few weeks, as May monthly data for several key contributors to GDP become available. My presumption is that it will rise noticeably.

Finally, I would note that even if the current Atlanta Fed estimate for Q2 real GDP were to come to fruition, the composition of output would look similar to Q1’s, with trade and inventories dragging the headline down while underlying demand grows substantially. Barring a shocking drop in jobs in June, the labor market figures would also support the notion that the economy continued to advance markedly in the spring. In short, the worries about an economic downturn having begun in the first half of 2022 are overblown. To be sure, I view a recession as an odds-on bet. But not for a while longer.