By the Numbers

An aging supply of CLOs builds up in the warehouse

This material is a Marketing Communication and does not constitute Independent Investment Research.

Warehouse financing for the CLO market continues to signal that issuance could cool off quickly later this year, although a healthy supply of deals is still in the pipeline. The number of outstanding warehouse lines has bounced up and down since January but still stands only a bit below last year’s peak. The increasing average age of outstanding lines nevertheless suggests that once the current pipeline clears through the back half of 2022, issuance should drop sharply.

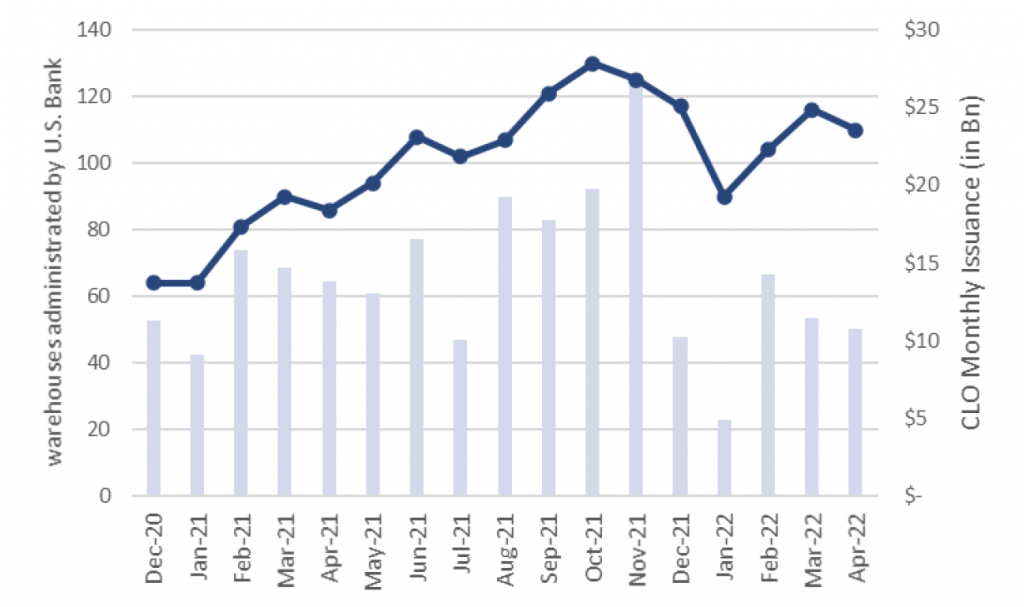

US Bank, the largest CLO trustee, reported in April 110 CLO warehouses under administration (Exhibit 1). US Bank historically has a 52% to 54% trustee market share, implying total open warehouses today of between 200 and 210. That compares to peak warehouses under US Bank administration in October last year of 130, implying more than 250 lines open across the market then. The number of lines administered by US Bank dropped sharply into January, presumably reflecting deals going to market ahead of the deadline for issuing LIBOR-indexed debt. But the number of administered lines has since rebounded. The rebound might suggest a repeat of last year’s market, but something else is going on.

Exhibit 1. The ups and downs of outstanding CLO warehouse lines

Note: The number of warehouses open reflect only those administered by US Bank.

Source: U.S. Bank, S&P LCD

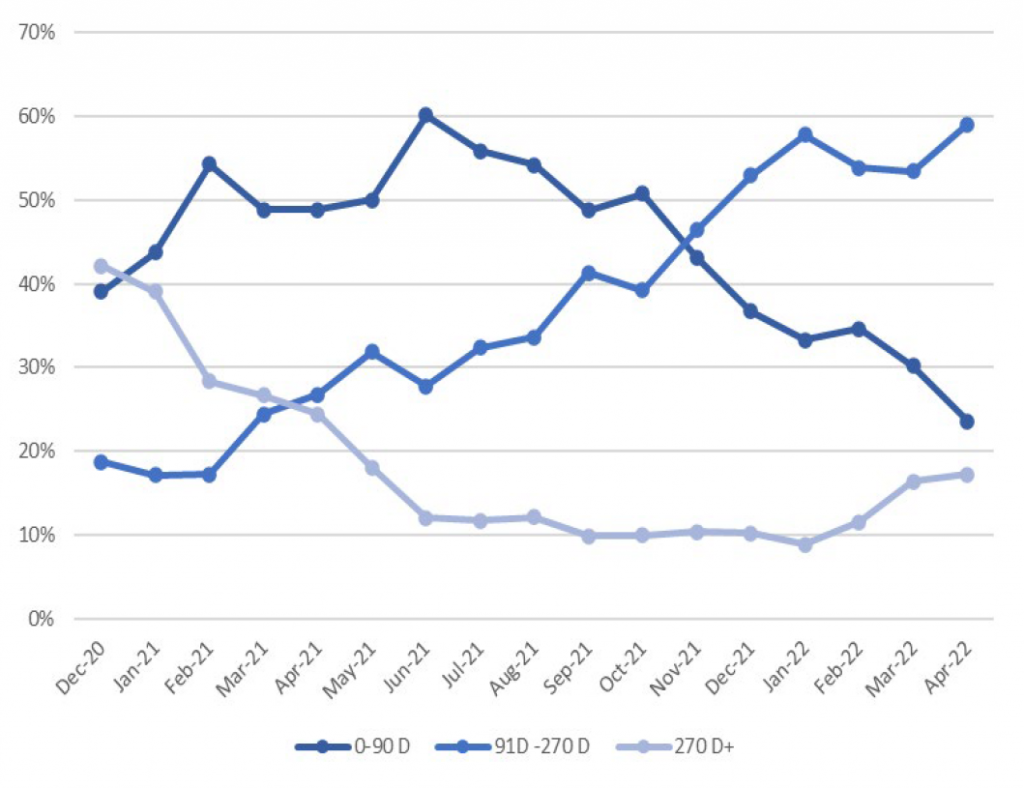

A rise in number of outstanding warehouse lines clearly reflects more lines opening than closing—usually closing after issuing a CLO. Last year, the surge at least partly reflected a backlog of deals waiting for rating agencies and other parties to get through the required work. The number of warehouses aged three months or shorter (0-90D) has declined from 60% in June last year to 24% lately (Exhibit 2). In contrast, the share of warehouses aged in between three months and nine months (91D – 270D) has kept trending up. And the share of warehouses aged nine months (270D+) or more has increased from 9% to 17% this year.

Exhibit 2. The average age of outstanding warehouse lines is rising

Note: the data reflect only warehouse lines administered by US Bank.

Source: U.S. Bank.

A few possibilities could explain the age extension in CLO warehouses:

- After fast growth last year, warehouse lenders may be playing defense in the wake of market volatility

- Widening spreads on CLO debt and the relatively steadier pricing on leveraged loans may have soured some CLO equity investors and managers on the economics of new deals and reduced demand to borrow

- Some managers have chosen lately to print-and-sprint—pricing a deal without a portfolio in the warehouse and aggregating loans afterwards, reducing demand for warehouse financing, or

- Favorable warehouse economics coupled with rising funding costs in the capital markets may have pushed CLO managers to simply wait for a better issuance window to open

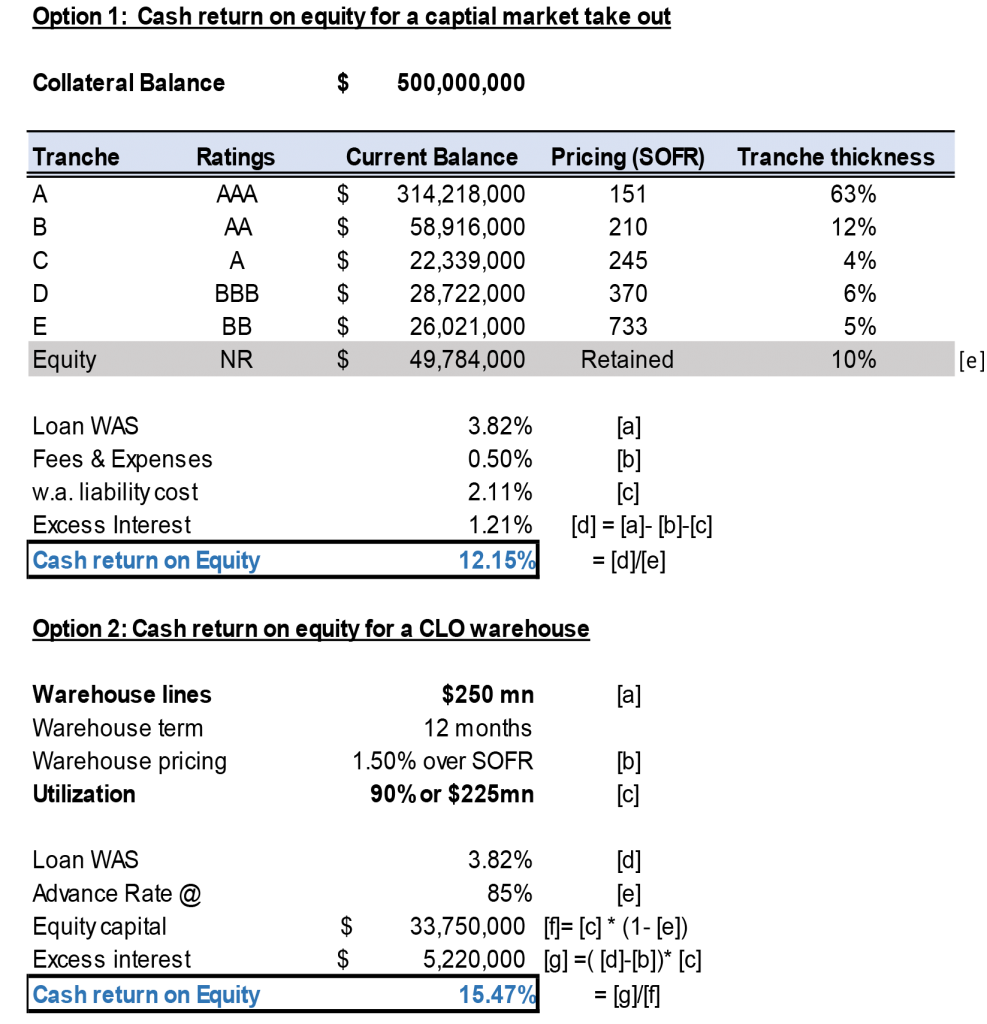

Of these possible explanations, the appeal of warehouse financing over capital markets for now is clear. The funding cost for a new issue BSL CLO has increased from an average of 180 bp in the beginning of this year to 210 bp for some recently priced deals. While CLO warehouses are typically lower levered than CLO deals—5x to 7x leverage in warehouse compared to 9x to 10x leverage through a CLO—an average of low- to mid-100 bp pricing in warehouses offer better economics to most CLO managers. A hypothetical example suggests warehouse financing could offer better cash flow return on equity (Exhibit 3). Of course, warehouse facilities are heavily negotiated between lenders and managers, and the economic impact on equity will be very sensitive to the advance rate, pricing, and fees inputs.

Exhibit 3. Cash-on-cash return on equity may be better for now in a warehouse

Source: Amherst Pierpont Securities estimates

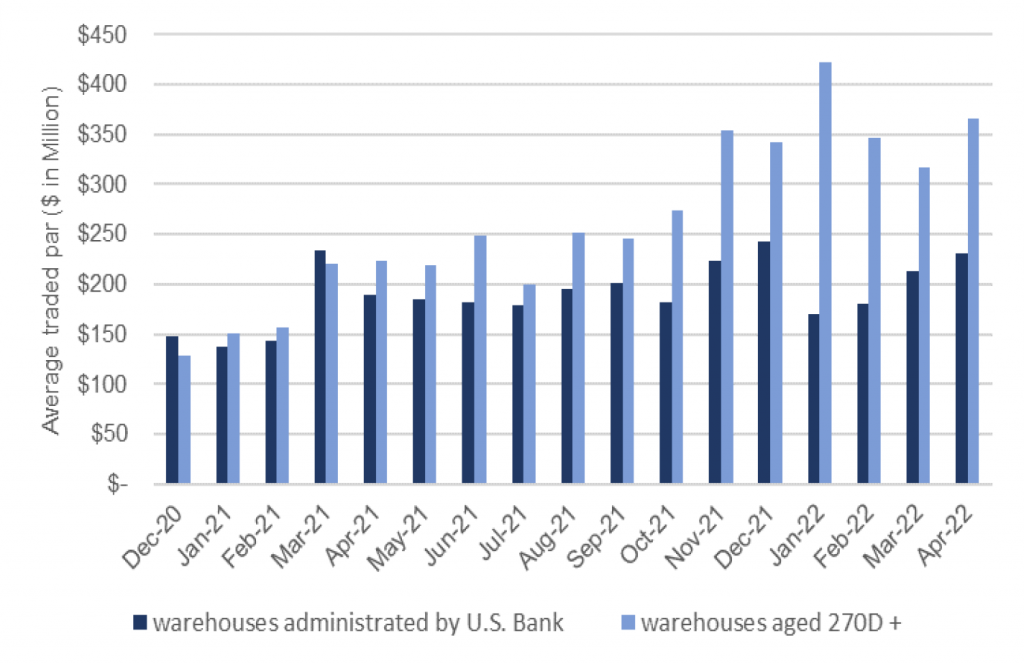

In addition to age extension, warehouse traded par, the aggregate dollar amount of loans in warehouses, also points to a current backlog in CLO warehouses. The average traded par in warehouses aged nine months or older has been much higher than the average traded par in all warehouses under US Bank’s administration (Exhibit 4).

Exhibit 4. Older warehouses have built up steadily larger balances

Note: the data reflect only warehouse lines administered by US Bank.

Source: U.S. Bank

While the current market seems to be discouraging new warehouses, the current backlog needs to be cleared. It is very rare for warehouse lenders to ask CLO managers to liquidate their loan portfolio. Instead, lenders can make the warehouse line to amortize and, in this case, the traded par in warehouse will be reduced accordingly. Another viable solution is to negotiate for an extension. Warehouse lenders can ask CLO managers to post new collateral or simply reduce the advance rate in the warehouse line. Either way, the economics for CLO managers to stay in warehouse will be more expensive, therefore, incentivize managers to execute a capital market take out. That could give equity investors significant leverage in negotiating better terms, lower fees, better pricing or all of the above.

CLO equity and debt investors look like they have an important opportunity ahead. With warehouse balances relatively high but getting older by the day, the pressure to issue should build into July. The average term of a warehouse is 12 months but can be as short as six months. In a very few cases, lenders offer evergreen facilities. The leading edge of warehouses now 90 days to 270 days old starts to bump up against maturity in mid-summer. There may be room to negotiate, but it is not infinite. The back half of this year could see a bit of the CLO market equivalent of a shotgun wedding—issuance under pressure. That creates the potential opportunity. Investors should sharpen their pencils. The low level of new warehouses suggests that after the late 2022 supply, primary issuance will drop significantly.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.