By the Numbers

KBRA pushes back on S&P’s proposal for insurer ratings

This material is a Marketing Communication and does not constitute Independent Investment Research.

KBRA has started to push back against an S&P proposal that would likely hurt smaller rating agencies and affect the ability of insurance companies to invest in certain fixed income products. S&P’s proposed approach to insurer financial strength would penalize securities without an S&P rating by raising the amount of capital needed to hold the investment. KBRA argues that its ratings deserve much more favorable capital treatment than the one proposed by S&P, although it is unclear whether S&P will be swayed.

KBRA on April 18 issued a public response to a proposal originally floated by S&P on December 6. The proposal focuses on a broad set of influences on financial strength—current capital, asset credit risk, interest rate and other market risks across assets and liabilities, risks of loss in different lines of business, the impact of diversification and so on—but provisions for setting capital on bonds and loans has drawn sharp fire. Any asset without an S&P rating, in the proposed approach, gets penalized. In particular:

- For corporate and government ratings, S&P lowers a Moody’s or Fitch investment grade rating by one notch and a speculative grade rating by two notches; for instruments rated by both, S&P uses the lowest notched rating

- For structured finance, S&P lowers the rating in general by three notches; if rated by both, S&P may lower the lowest rating by two notches

- For assets without an S&P, Moody’s or Fitch rating, the proposal would treat these assets as ‘CCC’

Treatment of assets without a rating from a major agency has drawn especially sharp fire. An asset rated ‘AAA’ by KBRA, DBRS Morningstar, Egan-Jones or other agencies would drop to ‘CCC’, potentially raising capital required under the S&P approach by more than 1,000 times.

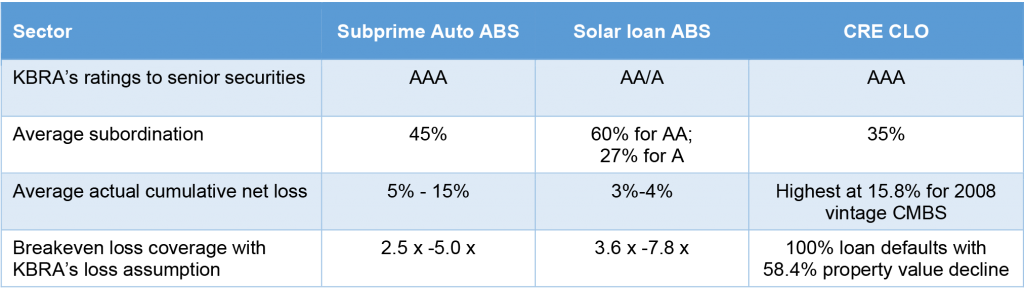

The KBRA response argues that S&P’s approach does not fairly assess the risk of KBRA-rated assets. The response focuses on subprime auto loan ABS, where both KBRA and S&P play, solar loan ABS, where KBRA dominates and S&P has just started to play, and CRE CLOs, where S&P has no market presence. In all examples, KBRA argues that structural protections should allow those securities to withstand losses in most draconian scenarios, a much stronger profile than ‘CCC’ (Exhibit 1).

Exhibit 1. KBRA’s breakeven loss coverage

Note: Breakeven loss coverage indicates the rated class could take a multiple of historic cumulative collateral losses before incurring loss of class principal. Protection comes from subordination, excess spread and other sources.

Source: KBRA

KBRA already has seen an impact from the S&P proposal. At least seven deals moving through the KBRA rating process have been put on hold since the S&P announcement by issuers concerned about going to market with a major rating agency, according to Caitlin Colvin, a managing director at KBRA. Some bankers have reported issuers taking deals to S&P that might have used only KBRA in the past.

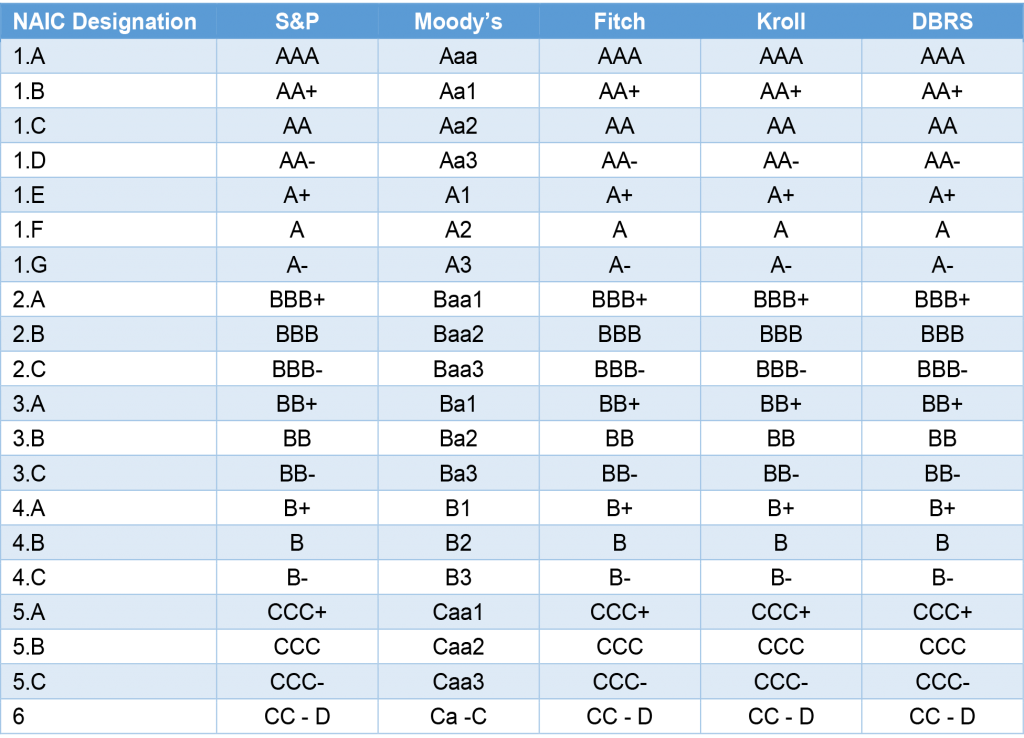

KBRA gets much better treatment under S&P’s current approach to insurer financial strength ratings, at least for US insurers. Where S&P does not have a rating on a security, the agency uses the current designation from the National Association of Insurance Commissioners to map to other rating agencies. That mapping puts KBRA and DBRS on even ground with S&P, Moody’s and Fitch (Exhibit 3). S&P is dropping this approach, however, in favor of one that would apply both inside and outside the US.

Exhibit 2. NAIC generic rating symbol mapping

Source: NAIC, available here.

S&P is taking comments on its approach through April 29, but market participants already started to react. Some insurance investors have reportedly stopped buying assets that might be affected by the proposed S&P approach and Structured Finance Association and the American Council of Life insurers plan to file comments on the proposal as well. And the Wall Street Journal reports that 26 congressional Democrats and Republicans sent a letter to SEC Chairman Gary Gensler on April 14 asking for a closer look into S&P’s move. “Many impacted stakeholders have expressed concern that this treatment of investments is potentially anticompetitive,” the letter said, “and we share this concern.”

For more background, see Concern continues around S&P insurer ratings.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.