The Big Idea

Welcome back, workers

This material is a Marketing Communication and does not constitute Independent Investment Research.

The labor market has been grossly out of balance for at least a year, with demand far outstripping supply. But businesses over the last month or two have reported somewhat better success hiring and retaining workers. This coincides with a surge in labor force participation, according to BLS data. It appears people sidelined due to pandemic have been returning to the job market in large numbers since Omicron faded. While this may temper the trend somewhat, labor markets are still tightening and are likely to continue to do so for the foreseeable future.

Prime-age labor force participation

The labor force participation rate is calculated from the BLS monthly household survey. Respondents are classified as employed, unemployed—not working but actively looking for a job in the past month—or out of the labor force. The labor force participation rate captures the ranks of the employed and unemployed as a percentage of the working-age population.

One of the difficulties with the labor force participation rate is that the working-age population is defined as 16 and over. It consequently includes everyone over 65. As our population is growing older and a greater proportion of the public is in their retirement years, the aggregate labor force participation rate will naturally decline. This has been going on for over a decade. In the late 2000s, the 65-and-over cohort represented about 16% of the working-age population. The figure is now more than 21%.

An age-adjusted labor force participation rate can be calculated by holding population weights constant—that is, running a counterfactual where the age composition of the adult population never changes. This alternative series has rebounded from depressed levels just after the pandemic and is within less than a percentage point of the pre-pandemic level, which was the highest since 2001.

A slightly less comprehensive but more straightforward way to control for the aging of the population is to focus on what economists call the prime-age labor force participation rate, which includes those ages 25 to 54. These are the cohorts with consistently high labor force participation rates.

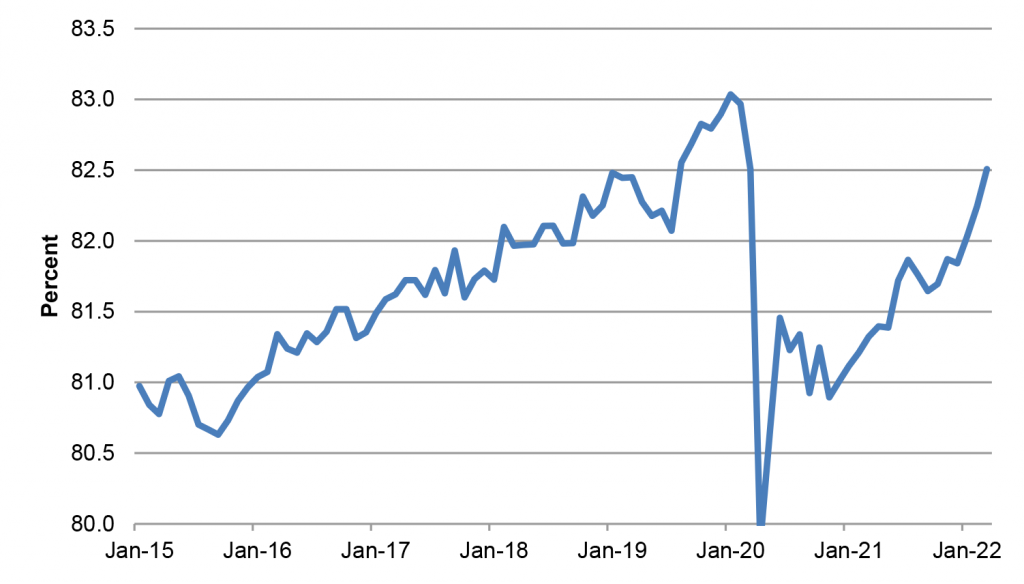

The prime-age labor force participation rate has surged in recent months. It was at 83.0% just before the pandemic began and dropped by about 3 percentage points in March and April of 2020. It quickly retraced half of that drop by June 2020. However, after that, progress was limited, as generous fiscal support, health concerns, and childcare difficulties dissuaded some from working. The prime-age labor force participation rate actually fell in the second half of 2020 by half a percentage point to 81.0% by December, then clawed back eight tenths of a percentage point through all of 2021. However, in the first three months of 2022, the measure has surged by seven tenths of a percentage point, rising to 82.5% in March. This brought it to within half a point of the February 2020 high and in line with the 2019 average (Exhibit 1).

Exhibit 1: Labor force participation rate ages 25 to 54

Source: BLS.

To put numbers to the percentages, based on the March 2022 population level for ages 25 to 54, moving from March’s 82.5% reading up to the pre-pandemic high of 83.0% would entail another 635,000 people entering the job search. At the pace of payroll growth seen in recent months, that magnitude of new job candidates would be snapped up in a month or two. In short, labor force participation is almost back to normal for prime-age workers, which means that, going forward, the prospect of millions of workers returning to alleviate the tightness of the labor market is highly unlikely—in fact, it has mostly already happened.

Age detail

Looking at the more detailed breakdown in labor force participation by age offers two additional insights on the post-Covid dynamics of the labor market. First, adults of child-bearing age represent the bulk of the recent surge in labor force participation. For the 25-34 and 35-44 age cohorts, labor force participation rates have jumped by 1.3 and 1.5 percentage points, respectively, over the past six months, roughly double the rise in the overall labor force participation rate.

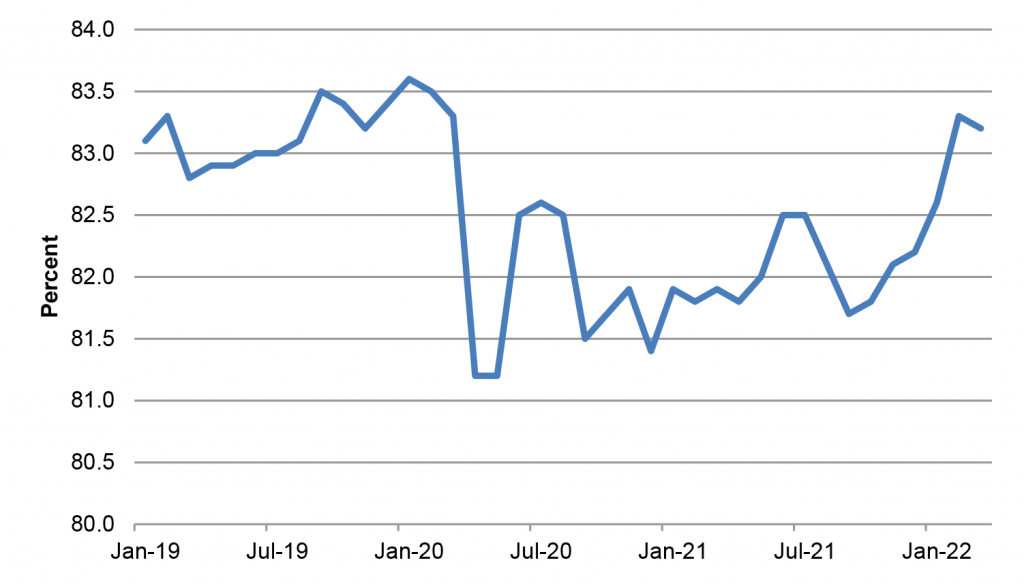

In particular, for the 35 to 44 age cohort, school policies appear to have governed labor force participation to a significant degree. The participation rate jumped in the summer of 2020 and in the summer of 2021—when seasonal adjustments likely already accounted for some parents staying home to care for their kids—and dipped in September of each year, when remote or hybrid school schedules required parents to be home (Exhibit 2). However, the participation rate has broken out higher over the past several months.

Exhibit 2: Labor force participation rate ages 35 to 44

Source: BLS.

Evidently, parents have finally within the past 3 to 6 months been able to return to work, as schools are almost entirely in person and widely expected to remain so. This dynamic appears to represent a major part of the recent jump in labor force participation.

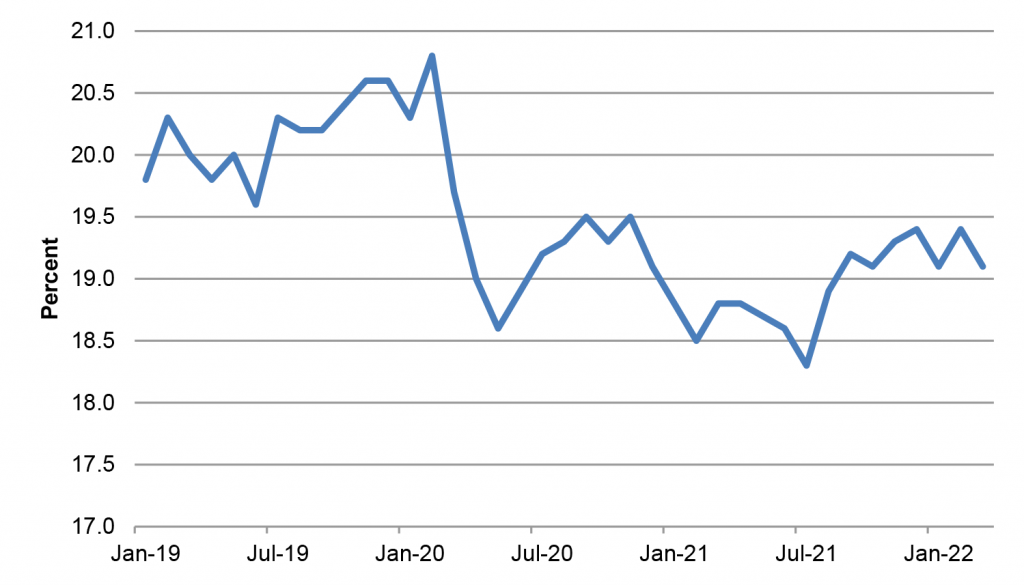

In contrast, there is another group that is not coming back, at least not yet. The labor force participation rate for those 65 and over dropped noticeably early in the pandemic and, unlike for other age cohorts, has failed to bounce (Exhibit 3).

Exhibit 3: Labor force participation rate ages 65 and over

Source: BLS.

Economic researchers have shown that there were 2 to 3 million excess retirements in 2020, as people who were close to retirement age and were furloughed during the lockdowns chose not to come back. Given the disproportionate health impact of Covid on older people, it is understandable that they would be more cautious about exposing themselves to the public by returning to work.

Nonetheless, even as vaccinations became widely available—almost 90% of seniors are fully vaccinated and two-thirds of them also received a booster—and the health risks of Covid have receded, these retirees have chosen by and large to stay retired. Historically, the re-entry rate for retirees tends to be low, but the fact that the labor force participation rate for this age cohort is about the same as it was in April 2020 is striking. One factor that likely helps to explain this development is the steep improvement in asset prices. The increase in home and equity values over the past two years would have greatly padded recent retirees’ nest eggs, making it easier for them to kick back and enjoy their golden years.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.