By the Numbers

The evolution of Freddie Mac K-deals

Mary Beth Fisher, PhD | March 11, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

Freddie Mac’s flagship multifamily K-deal program has evolved over the past two years. The elimination of mezzanine classes and launch of the when-issued program have affected deal structure and realigned historical spreads between fixed-rate Ks and DUS. A cheat sheet of K-deal programs highlights these changes and underscores a relative value opportunity for total return accounts that will likely become a persistent feature of fixed-rate 10-year and 7-year K-deals.

Size and scope of K-deal programs

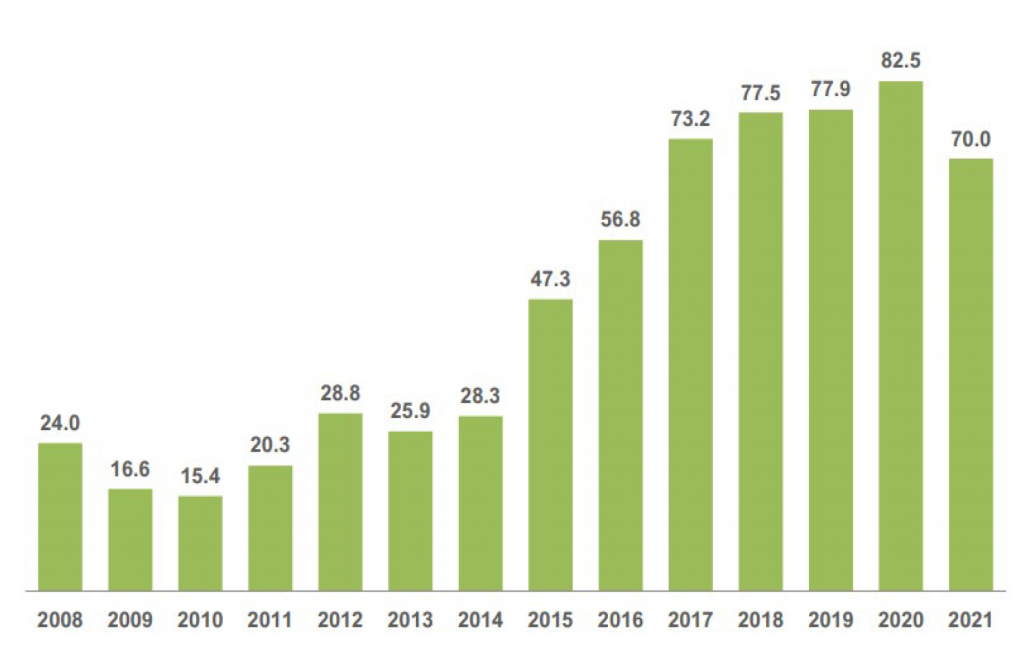

Freddie Mac’s multifamily loan production totaled $70 billion in 2021, with total securitization volume of $80 billion. About 90% of that is securitized through one of the K-deal programs, while around 9% is securitized through the small balance (FRESB) loan program.

Exhibit 1: Freddie Mac multifamily loan production

Note: Data through December 2021. Source: Freddie Mac Multifamily Securitization Overview

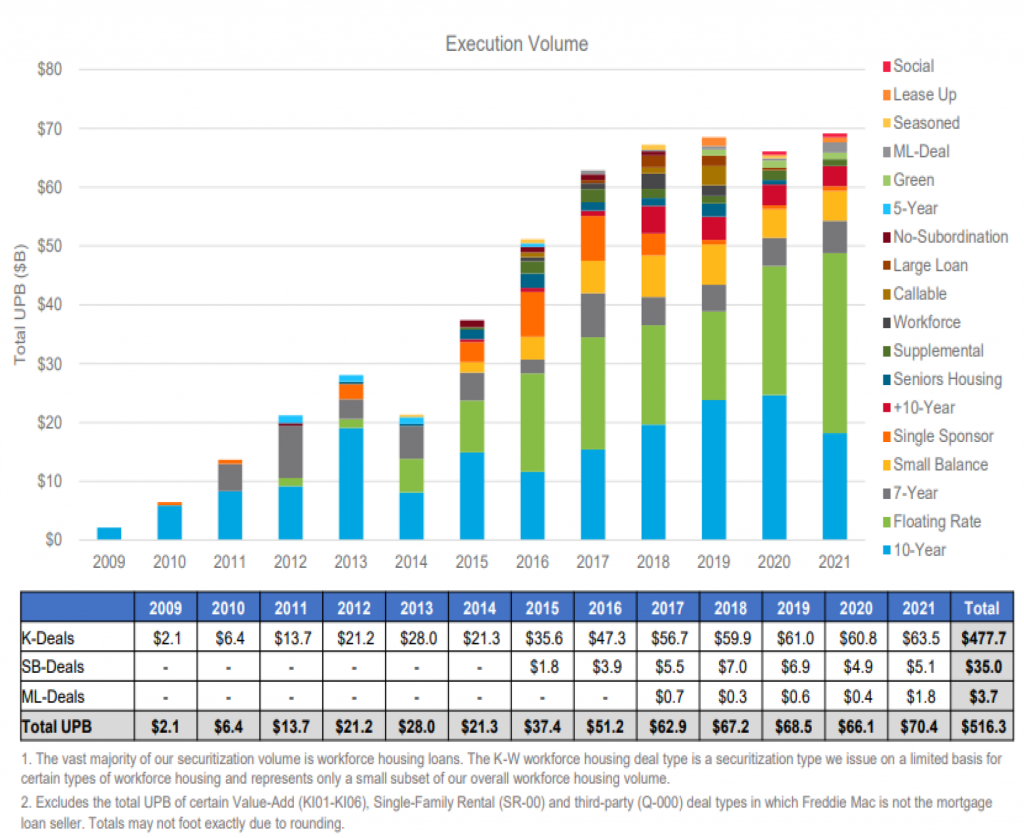

There are a variety of active and retired K-deal programs, though the primary ones – those with the largest issuance year over year – are fixed-rate 10-year, 7-year, 15-year (which Freddie calls 10+ year), and floating rate deals (Exhibit 2).

Exhibit 2: Freddie Mac multifamily securitization volume

Note: Data through December 2021. Source: Freddie Mac Multifamily Securitization Overview

Evolution and adaptation

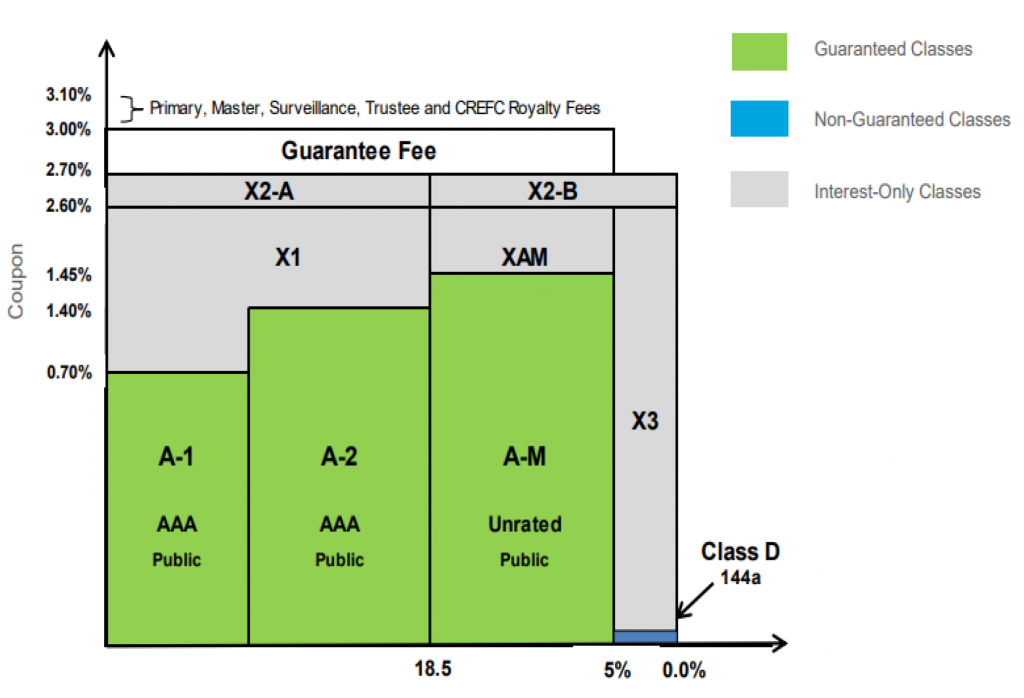

The structure of K-deals has evolved over the last few years. The current general structure of fixed-rate K-deals is shown in Exhibit 3. There are three guaranteed, sequential pay principal and interest classes including A1, A2 and AM in order of ascending final maturity; a B-piece, D, which is the single loss-absorbing subordinated tranche; and several interest-only classes attached to the guaranteed and unguaranteed tranches. The unguaranteed mezzanine tranches of deals, previously B and C classes, were eliminated in early 2020 in response to market volatility during the pandemic and an impending change in the capital rules drafted by the Federal Housing Finance Agency.

Exhibit 3: Sample fixed-rate K-deal structure

Source: Freddie Mac Multifamily Securitization Overview

The first loss B-pieces, typically bought by hedge funds or private equity, were not expanded in response to the elimination of the mezz tranches. Instead, the first evolution in the deal structure was a shift in the relative size of the guaranteed versus loss-absorbing classes. For example, in standard 10-year K-deals the mezzanine tranches used to account for 4% (B) and 2.5% (C) of the deal size, with the first loss D tranche typically being 7.5% thick, making the combined subordinate classes 14% thick. After the B and C classes were eliminated, the last guaranteed sequential pay class – the AM tranche – was gradually expanded. In 2021, the D class shrank from 7.5% to 5%, pushing the AM class to fully 15% of the deal.

Credit quality

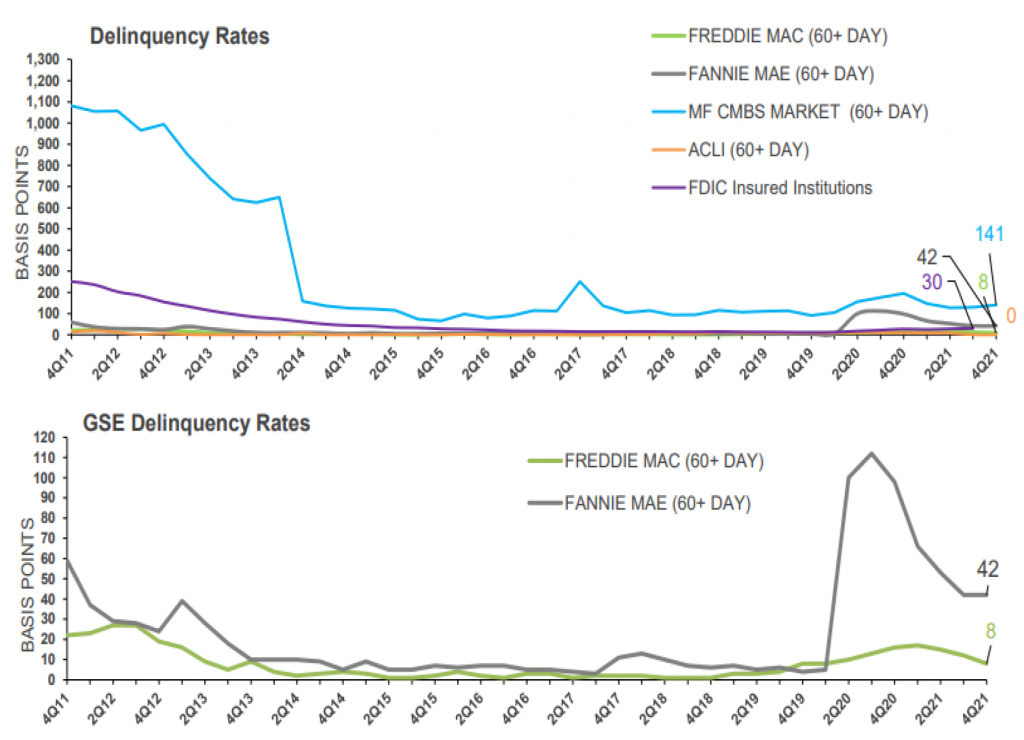

The shrinking of the first loss piece of K-deals might raise eyebrows, but the credit quality of the portfolio has been exceptional since the K programs began in 2009. Overall, both Fannie and Freddie’s multifamily delinquency rates have been well below those of other lenders during the pandemic (Exhibit 4).

Exhibit 4: Multifamily delinquency rates

Notes: Freddie Mac does not report forbearance loans in delinquency rates if the borrowers are in compliance with the forbearance agreement. Fannie Mae’s delinquency rate includes loans that received a forbearance.

Sources: Freddie Mac, Fannie Mae, American Council of Life Insurers (ACLI) Quarterly Investment Bulletin, FDIC Quarterly Banking Profile, TREPP (CMBS multifamily 60+ delinquency rate, excluding REOs) for periods prior to 3Q17, Wells Fargo CMBS research for 4Q17- current CMBS delinquency rates. Current delinquency rates for FDIC are not yet available. Freddie Mac Multifamily Securitization Overview, page 9 of 72 as numbered.

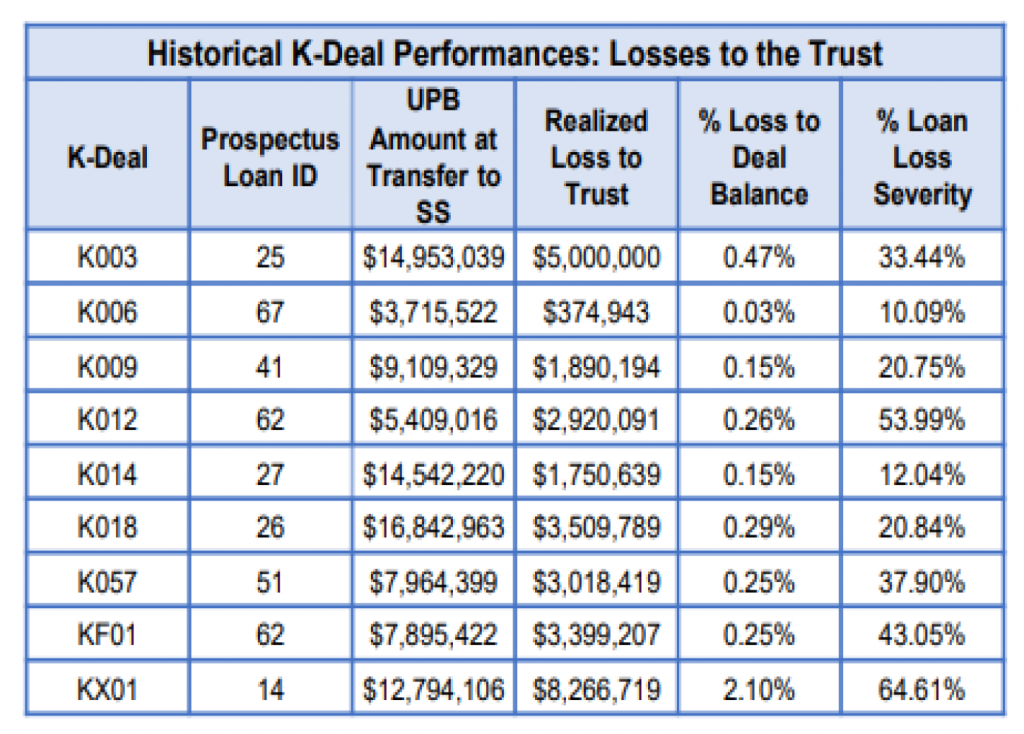

Losses in the K-deal multifamily portfolio have been very small historically (Exhibit 5). Of the hundreds of K-deals issued across all programs, only 9 deals have experienced credit losses. With the exception of the KX01 deal, the average loss to the deal balance was 23 bp, which is equivalent to 3.08% of the principal balance of a 7.5% B-piece. The KX01 deal is a kick-out deal and the B-piece was a conservative 85% of the balance, so the loss represented 2.5% of the outstanding principal of the B-piece. The exceptionally low historical losses is likely one of the reasons that the loss absorbing B-piece classes have remained mostly in the 5% to 10% range for most K-deals despite the elimination of the mezzanine tranches.

Exhibit 5: Historical losses

Note: Losses through June 30, 2021. Total losses to B-piece investors have been $30.13 million since inception of the K-deals in 2009. Freddie Mac has not realized any credit losses on their K-deal guarantees.

Source: Freddie Mac

The other big shift in the K-deal program has been the introduction of the when-issued (WI) certificates for 10-year and 7-year Ks in late 2021 (notes in the Cheat Sheet). The details of the WI program and its impact on the market is discussed at length in A total return opportunity in Freddie Mac’s WI program. The condensed version is as follows:

- When issued (WI) certificates for the AM and A2 classes are issued up to 90 days prior to the collateral being fully assembled and the deal brought to market.

- The WI certificates have a fixed coupon and pay interest; the WIs are tradeable and can be financed in the repo market, just like Treasury WIs or regular Ks.

- To date, secondary trading of WI K certificates prior to their conversion to regular Ks at settlement of the underlying deal, has been very thin but is expected to build.

- Because the collateral pool is not finalized, WIs are issued with credit criteria that is similar to, but somewhat weaker than, historical credit characteristics of existing 10-year and 7-year Ks.

- The projected maturity of the WI AM and WI A2s is also 10.25 years because it has to incorporate the full 90 days prior to deal settlement, despite the fact that most deals have come within a month of WI issuance.

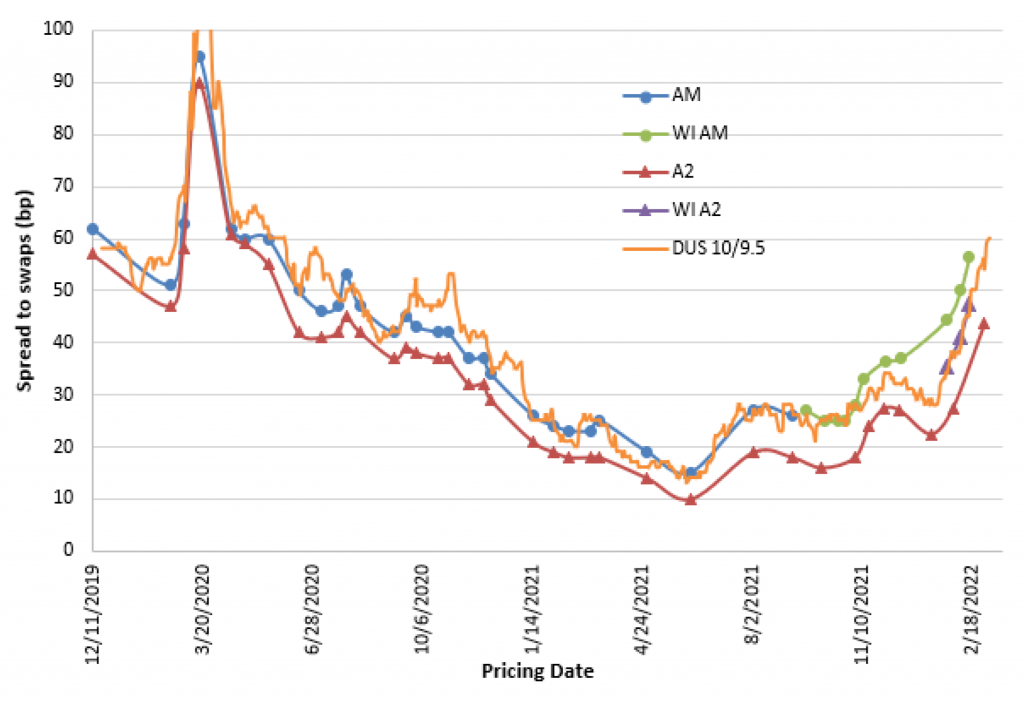

A host of challenges, market volatility and regulatory hurdles for banks and insurance companies – long the primary buyers of benchmark K deals – has pushed WI AMs and WI A2s about 4 to 5 bp wide of where the underlying class will probably trade. Fannie Mae 10/9.5 DUS, which used to trade in-line with the AM class of 10-year Ks, now trades in-line with the WI A2 class and inside of WI AMs (Exhibit 6).

Exhibit 6: Relative spreads of 10-year K-deal AM, A2 classes versus 10/9.5 DUS

Note: Data through 3/8/2022.

Source: Bloomberg, Amherst Pierpont Securities

Money managers and total return investors have stepped into the void left by banks and insurance companies and have been buying the WIs at issue. Holding the WIs until the underlying deal comes to market and selling them after the certificates convert should produce excess return of about 5 bp over the holding period. This widening of the WIs is likely to persist unless banks and insurance companies can get comfortable with holding a TBA-like instrument without assigned collateral, potentially over month and quarter-ends. This creates a good relative value trade for investors who can step in.

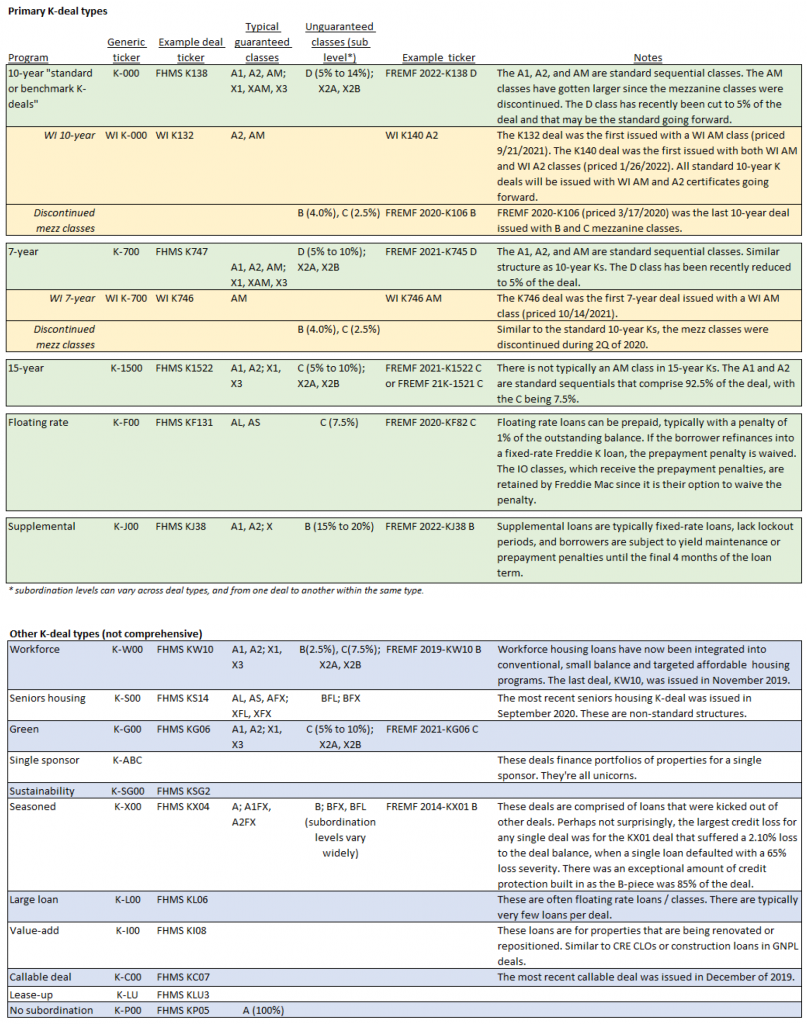

Cheat sheet on various K-deal programs

Source: Freddie Mac, Amherst Pierpont Securities

Lockouts and prepayments

The majority of fixed-rate, first-lien loans in K-deals are subject to a typically 2-year lockout period. After expiration of the lockout period, the loan requires defeasance to be prepaid. The loan enters an open period during the final 4 months of the term where it can be prepaid without penalty.

- Defeasance replaces the mortgage loan with Treasury securities that produce an identical principal and interest stream to the defeased loan.

- There is no impact on the cashflows for the investors, and the credit quality of the pool improves. Unguaranteed classes that are rated can be upgraded when the deal has high levels of defeasance.

- Prepay reports for standard, fixed-rate K-deals are not typically produced because prepayments via defeasance do not change the duration or convexity of the bonds.

Supplemental, junior-lien loans in KJ-deals, floating-rate loans in KF-deals, and some fixed-rate loans are subject to yield maintenance provisions and/or static prepayment penalties (usually 1% of the outstanding balance) to be prepaid. These loans also have an open period during the final 4 months of the term.

- Prepay speeds and reports are produced by APS (thank you, Brian Landy) because the cashflows of the KJ and KF deals are impacted by prepayments. Those reports are available here (right side of page, APS Freddie Mac CMBS Prepays).

- The prepayment premiums for fixed-rate mortgages are generally distributed to the principal and interest bearing classes and then the interest only classes. The B-piece does not receive prepayment penalties.

- The prepayment premium for floating-rate loans is usually a static prepayment penalty of 1%. The penalty can be waived by Freddie Mac if the borrower refinances into another Freddie loan. These penalties are generally distributed to a designated X interest only class, which in KF deals is retained by Freddie Mac.

- The yield maintenance charges and prepayment premiums are not subject to Freddie Mac’s guarantee.

Additional resources

Freddie Mac Multifamily Securitization Overview

Freddie Mac K-Deals (there are a lot of links to additional information on this page)