The Big Idea

Rising risk premiums in the money markets

Steven Abrahams | March 11, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

The cost of funding anything with risk is going up. Pick your favorite benchmark and it says any borrower with even a hint of risk has to pay more for funding since February 24. Even in the Treasury market, rising dispersion of yields in intraday trading says marginal risk comes at a price. With the Fed about to start drawing liquidity down, the price of risk looks likely to keep going up.

More for a fist full of dollars

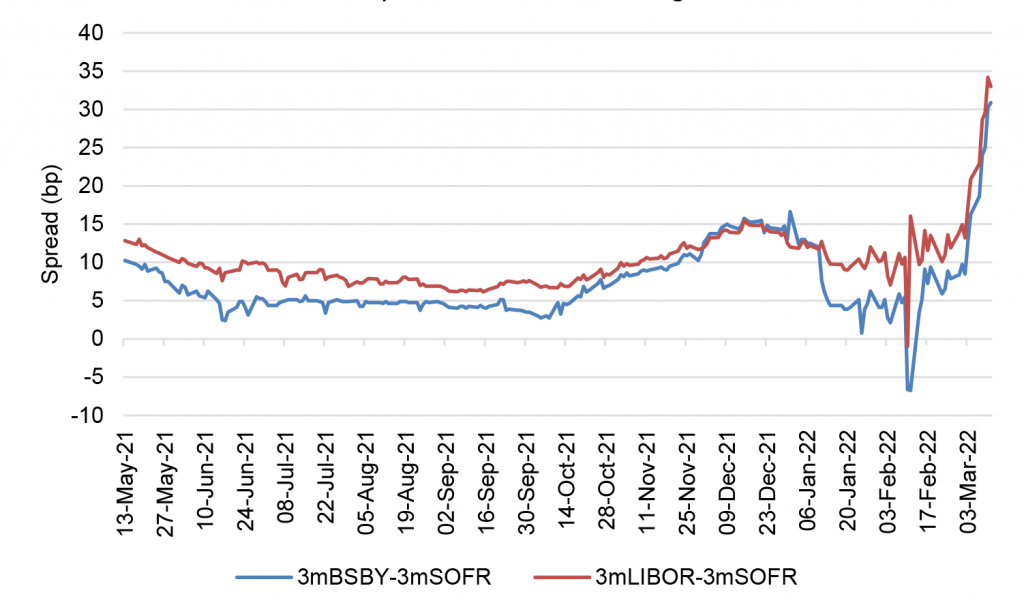

The relative cost of dollars for banks has moved up since the February 24 Russian invasion of Ukraine. The yield spread between 3-month LIBOR and SOFR has moved from 13 bp to 33 bp, and between 3-month BSBY and SOFR from 9 bp to 31 bp (Exhibit 1). It is still well below crisis levels. In March 2020, the spread between 3-month LIBOR and SOFR peaked at 140 bp. But it is near levels of modest stress in the last few years.

Exhibit 1: A relative rise in the price for bank borrowing

Source: Bloomberg, Amherst Pierpont Securities

The latest wider spreads anecdotally come in part from demand for dollars in the commodities markets, where interruption of exports from Russia and Ukraine have sent prices sharply higher. Commodities traders have had to pay more for inventory, drawing down bank lines of credit and sending banks into the commercial paper markets to replenish. Traders and speculators with short positions in commodities derivatives have had to meet margin calls, also drawing down bank lines of credit. Money market participants report that banks in Canada, the Scandinavian countries, Japan, New Zealand and elsewhere that often cater to commodities accounts have been noticeably active in commercial paper in the last few weeks.

The demand for dollars also may reflect sanctions that have made it difficult to move dollars out of Russia. Creditors expecting dollars from Russia now likely find themselves short and possibly needing to borrow to cover their own bills.

Traders in the repo market report that haircuts and spreads on the most liquid securities deliverable to the Fixed Income Clearing Corp have not changed. On riskier assets, haircuts have not changed but funding spreads have widened.

A first test of LIBOR-SOFR

As an aside, this is a first and minor test of the difference between a risky and a riskless rate in a market under pressure. LIBOR or BSBY, the risky rates in this episode, now reflect a premium over SOFR, the riskless rate. In the past, this might have limited implications beyond the normal market price of risk. But a range of risky assets including corporate debt and CLOs are increasingly indexed to SOFR. Since the assets’ index no longer reflects risk premium, the price of these assets will need to adjust to make up for the difference between SOFR and the risky rate.

A higher price for liquidity in the Treasury market

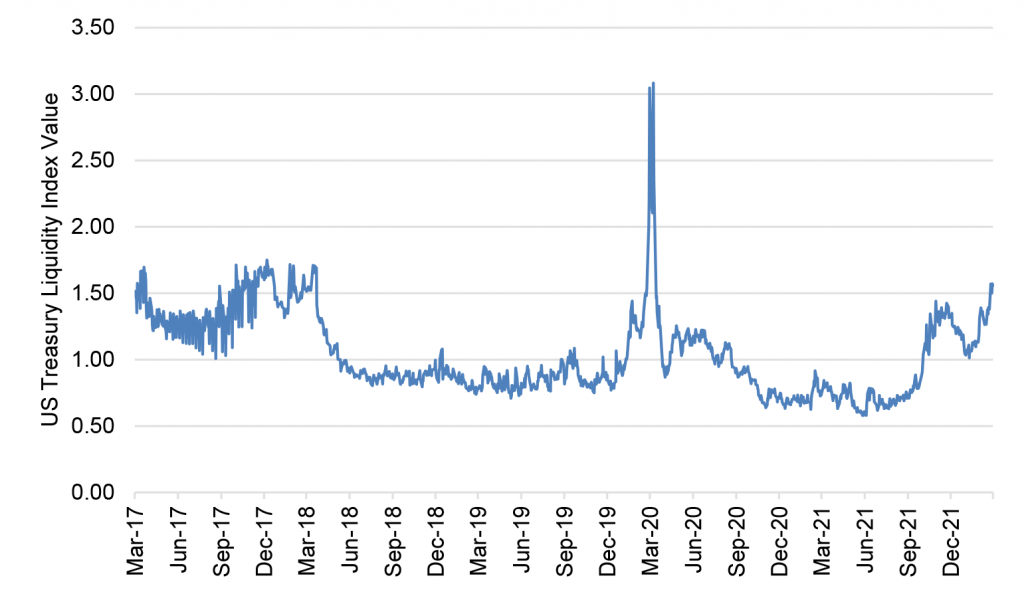

The price of risk is also going up in the Treasury market. Yield spreads between one-the-run and various off-the-run securities have become more dispersed, reflecting increasing concentration of capital is the most liquid issues and less policing of relative value in off-the-run issues (Exhibit 2). The risk here is not credit but liquidity, and this market is saying that the flexibility or optionality of converting quickly to cash is become more valuable.

Exhibit 2: A repricing of liquidity in the Treasury market

Note: The index reflects the average difference in yield between US Treasury issues with a 1-year or longer maturity and the intra-day Bloomberg relative value curve fitter. In liquid markets, deviations go away quickly, and index values are low. In illiquid markets, deviations persist, and index values are high.

Source: Bloomberg, Amherst Pierpont Securities.

Here comes the Fed

Fed Chair Jerome Powell’s Humphrey-Hawkins testimony left little doubt that the Fed would hike 25 bp on March 16, the opening salvo in officially starting to reduce financial system liquidity. Bank deposits, money market mutual fund balances and lately the Fed’s reverse repo facility balances also have been coming down, already pointing to a declining pool of investable cash. Unless demand to borrow drops, a declining pool of cash will only make the price of risk go up.

Although risk premiums in the money markets often get described as compensation for credit risk or illiquidity, they could just as easily be turned around and described as the cost of holding cash or converting quickly into cash. Holding cash should cost more in uncertain markets because cash has option value. Options look likely to get more valuable in the months ahead, and risk spreads look likely to get wider.

The base issue across the money markets and elsewhere across in the debt markets is uncertainty. There is plenty of uncertainty in the Fed path, which is why it has not provided forward guidance. That guidance has to be next to impossible to lay out because the course of inflation is highly uncertain. It was uncertain before the latest run-up in commodity prices, and more uncertain now. For practical purposes, the Fed cannot afford to narrow its options. Then there is uncertainty in the course of the Russia-Ukraine conflict both in the short run and in the long run. In the short run, the unknowns include the timelines and ultimate cost to both sides, the impact of refugees from the conflict on the rest of Europe and beyond and the prospects the conflict goes beyond Ukraine’s borders. In the long run, it seems very likely that either Russia, Ukraine or both come out of the conflict highly destabilized, leaving Europe and the rest of the world with significant risk. This is the risk money markets have just started to price.

* * *

The view in rates

The Fed’s RRP facility is closing Friday with balances of $1.56 trillion, slightly below average for the year. Balances have moved up by $74 billion in the last week. It will be important to watch what the Fed does with the RRP rate on March 16. There is some concern that a rising rate on the RRP could start to draw deposits away from banks.

Settings on 3-month LIBOR have closed Friday at 80 bp, up 22 bp in the last week. Setting on 3-month SOFR have drifted up to 47 bp, up only 7 bp in the last week. The spread between 3-month LIBOR and SOFR continues to widen as the market adds to the premium for taking risk.

The 10-year note has finished the most recent session at 1.99%, up 26 bp in a week. Breakeven 10-year inflation finished the week at 297 bp, up 27 bp on the week. The 10-year real rate finished the week at negative 98 bp, roughly unchanged from a week ago. Real rates dropped sharply as Russia invaded Ukraine, reflecting new, significant concern about whether growth will be sufficient to absorb future liquidity.

The Treasury yield curve has finished its most recent session with 2s10s at 24 bp, roughly unchanged in the last week, and 5s30s at 41 bp, flatter by 11 bp over the last two weeks. Flight-to-quality has outweighed the Fed path.

The view in spreads

Spreads generally look vulnerable while the Fed is calibrating policy to inflation and while the hot phase of the Russia-Ukraine conflict continues. And even after the hot phase of Russia-Ukraine ends, there is considerable uncertainty about stability in Russia and Ukraine in the long run. Of the major spread markets, corporate and structured credit is likely to outperform, as it has since March 2020. Corporates benefit from strong corporate fundamentals and from buyers not tied to Fed policy. The biggest buyers of credit include money managers, international investors and insurers while the only net buyers of MBS during pandemic have been the Fed and banks. Credit buyers continue to have investment demand, but insurers are likely to take an increasingly strong hand in setting prices.

MBS faces pressure as the Fed considers a quick start to runoff. My colleague Brian Landy projects that new supply of MBS will run at $60 billion a month. He also estimates the Fed will need to allow runoff in MBS of more than $30 billion a month. Without the Fed or banks to take up an average of $90 billion in incremental supply, the burden would likely fall on mutual funds. Mutual funds do not have the capital to fully take up the slack.

MBS also faces pressure from new, higher loan limits on Fannie Mae and Freddie Mac MBS. Higher balances bring more negative convexity. Fed taper also reduces the amount of negatively convex loans filtered out of the TBA floating supply. The quality of TBA should erode this year, and spreads widen with it.

The view in credit

Credit fundamentals continue to look strong but could start to soften later this year if the Fed aggressively dampens demand. Russia-Ukraine should have limited direct impact on either the US corporate or consumer balance sheet. Corporations have strong earnings, good margins, low multiples of debt to gross profits, low debt service and good liquidity. It will be important to watch inflation and see if costs begin to catch up with revenues. A higher real cost of funds would start to eat away at highly leveraged balance sheets with weak or volatile revenues. Consumer balance sheets look strong with rising income, substantial savings and big gains in real estate and investment portfolios. Homeowner equity jumped by $3.5 trillion in 2021, and mortgage delinquencies have dropped to a record low.