The Big Idea

On our way to an insurers’ market

Steven Abrahams | March 4, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

Life insurance portfolios may end up playing a bigger-than-usual role in the debt markets this year, especially since their balance sheets need spread income and can tolerate volatility and illiquidity. Lifers, along with other insurers, also have a continuing stream of investable premiums. The balance sheet and the cash set lifers apart from the Fed, which is ending portfolio growth this month, from banks, which are seeing their deposit base shrink, and from mutual funds and ETFs, which are seeing net redemptions. Lifers typically set the price in the longest and least liquid parts of the market, but they may start to play that role in other areas, too.

Drawn by wider spreads

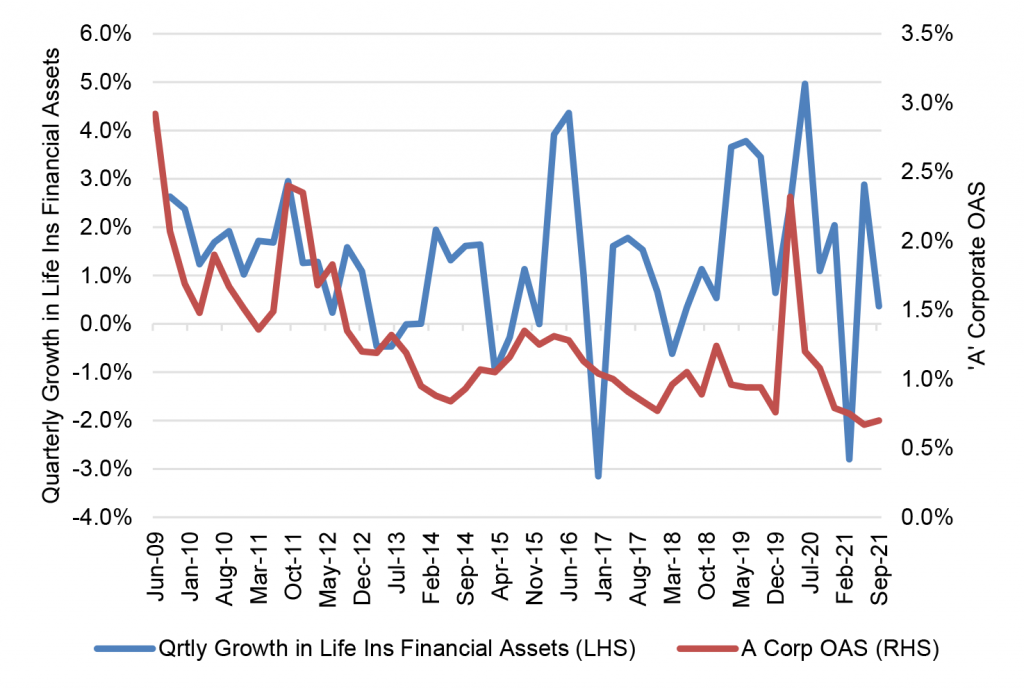

Wider spreads in the past have reliably drawn in life portfolios. Portfolio growth picked up following wider spreads around the peak of the European sovereign debt crisis in 2011, wider spreads around the peak of the energy crisis in late 2015 and early 2016 and wider spreads after the onset of pandemic in 2020 (Exhibit 1). Anecdotally, life portfolios in the last few weeks have started playing bigger roles in longer investment grade CMBS, in absorbing a late February surge in CLO issuance and in longer classes of private MBS.

Exhibit 1: Wider spreads usually accelerate life insurance general account growth

Note: Data for life insurance general accounts.

Source: Federal Reserve Z.1, ICE BofA US Single-A Corporate Index OAS as retrieved from FRED, Amherst Pierpont Securities

Lifers’ volatility tolerance partly reflects their long investment horizons and partly reflects accounting treatments that mute the impact of mark-to-market. Book yield accounting puts the focus on the spread between investments and the ultimate cost of the premiums. Rates can matter of course. Life portfolios usually have liabilities that run longer than assets—or put another way, lifers insure people that live well beyond the typical 30-year maturity of the longest investment assets. The mismatch creates rate risk in every new book of business, with falling rates hurting net asset-liability value and rising rates helping. Since March 2020, rates have run lower than the assumptions made when pricing most older vintages of life policies. Still, absolute rates are less important than spread for investing new money. Good asset-liability management is all about offsetting most of the impact of rate moves.

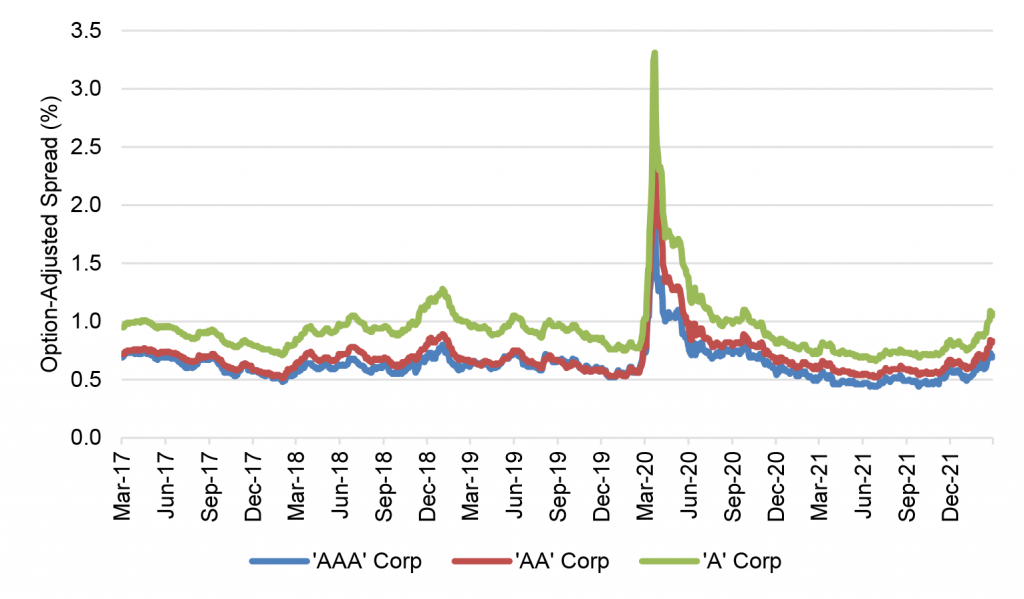

Spreads have moved in the direction of life insurers. Benchmark spreads in ‘AAA’, ‘AA’ and ‘A’ debt have moved to the point where they have been wider in less than 10% of trading sessions in the last five years (Exhibit 2). Most of the sessions where spreads closed wider than current levels came in the aftermath of pandemic. We are not there yet, but the mix of Fed policy, risks from the Russia-Ukraine conflict and even the impact of fiscal stimulus from spending in Europe and the US on defense and aid for Ukrainian refugees create plausible scenarios for much wider spreads.

Exhibit 2: Spreads sit at levels seen in less than 10% of sessions since 2017

Source: ICE BofA US Corporate Index OAS as retrieved from FRED, Amherst Pierpont Securities

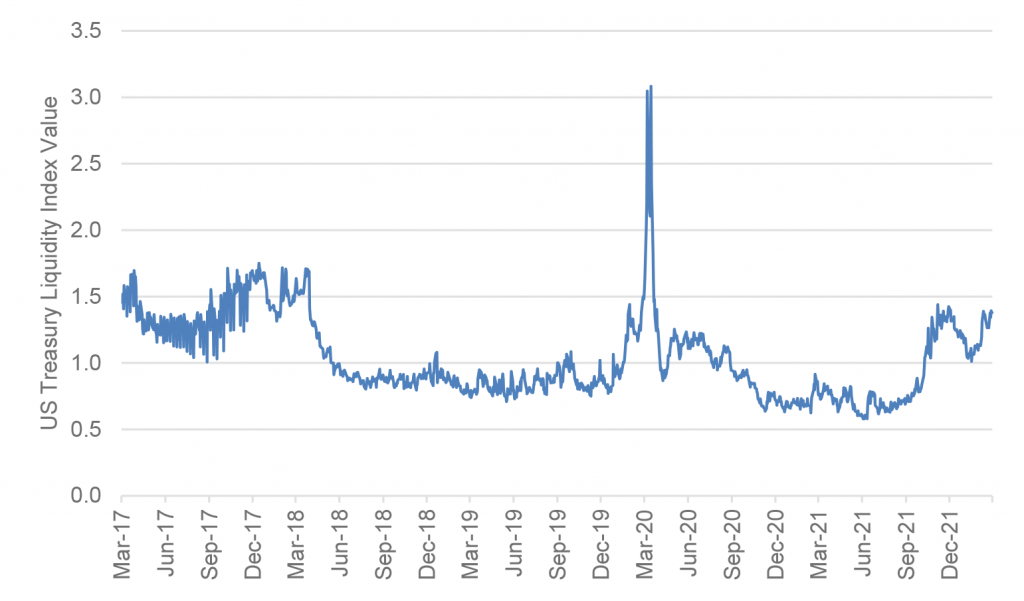

Liquidity has moved in insurers’ direction, too. Liquidity has deteriorated in the most liquid debt markets with less liquid markets trading erratically. The dispersion of yields in the US Treasury market between on-the-run and off-the-run issues has returned to levels triggered first this year by repricing of the Fed and before that by pandemic (Exhibit 3). Anecdotal reports from the agency pass-through and other markets suggest similar or greater deterioration.

Exhibit 3: Even in the US Treasury market, liquidity has deteriorated

Note: The index reflects the average difference in yield between US Treasury issues with a 1-year or longer maturity and the intra-day Bloomberg relative value curve fitter. In liquid markets, deviations go away quickly and index values are low. In illiquid markets, deviations persist and index values are high.

Source: Bloomberg, Amherst Pierpont Securities.

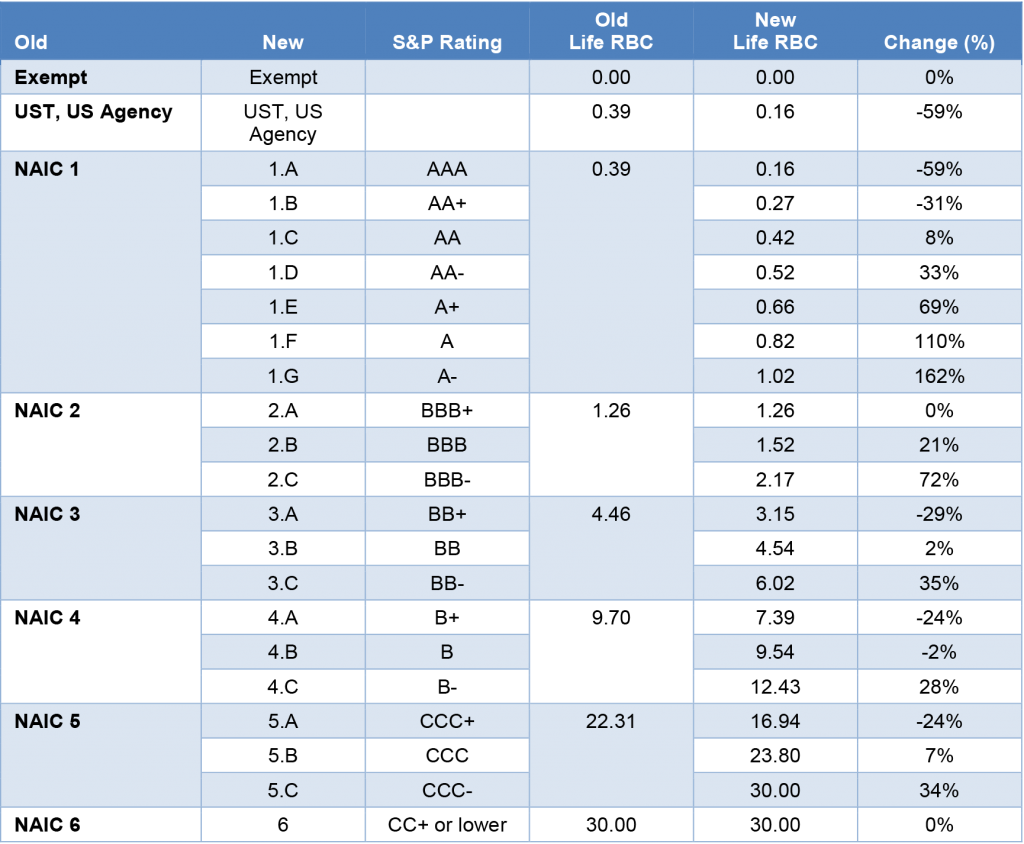

Life and other insurers are dealing with a few industry developments that may change patterns of new money investment. Risk-based capital requirements for securities now vary across 20 rating categories compared to six categories that applied as recently as 2020 (Exhibit 4). The shift lower in capital charges may make insurers especially receptive to ‘AAA’ and ‘AA’ assets trading at wide spreads due to deteriorating liquidity. Insurers are also weighing the potential impact of revisions to S&P’s approach to rating insurance companies. The approach penalizes assets rated by agencies other than S&P or not rated at all. The proposed revisions have drawn industry fire and remain out for comment until March 18. Conversations with several large insurers suggest they believe the rating agency will withdraw those provisions, but several smaller insurers have decided to stop buying assets that might be affected if S&P decides to move ahead.

Exhibit 4: New NAIC risk-based capita charges make finer distinctions by rating

Source: NAIC, Amherst Pierpont Securities

* * *

The view in rates

Since the start of war in Ukraine, the market has taken back roughly one hike in 2022. Fed funds futures and OIS forward rates imply roughly 5.5 hikes this year, down for more than six before war broke out.

The Fed’s RRP facility is closing Friday with balances of $1.48 trillion, close to the lowest of the year. Balances have dropped by $255 billion since the outbreak of war in Ukraine. It is too early to know the various causes for the withdrawals, but cash at the Fed facility would be vulnerable to sanction.

Settings on 3-month LIBOR have closed Friday at nearly 58 bp, up 7 bp in the last week. Setting on 3-month SOFR have drifted up to nearly 40 bp. The spread between 3-month LIBOR and SOFR has been widening. This arguably is the first minor test of differences in behavior between a risky LIBOR rate and a riskless SOFR rate.

The 10-year note has finished the most recent session at 1.73%, down 26 bp in a week due to Russia-Ukraine. Breakeven 10-year inflation finished the wek at 270 bp, up 14 bp on the week. The 10-year real rate finished the week at negative 97 bp, down 38 bp over the last week. The market is reflecting new, significant concern about whether growth will be sufficient to absorb future liquidity.

The Treasury yield curve has finished its most recent session with 2s10s at 25 bp, flatter by 15 bp in the last week, and 5s30s at 52 bp, steeper by 12 bp over the last two weeks. Flight-to-quality has outweighed the Fed path.

The view in spreads

Spreads generally look vulnerable while the Fed is calibrating policy to inflation and while the hot phase of the Russia-Ukraine conflict continues. Of the major spread markets, corporate and structured credit is likely to outperform, as it has since March 2020. Corporates benefit from strong corporate fundamentals and from buyers not tied to Fed policy. The biggest buyers of credit include money managers, international investors and insurers while the only net buyers of MBS during pandemic have been the Fed and banks. Credit buyers continue to have investment demand, but insurers are likely to take an increasingly strong hand in setting prices.

MBS faces pressure as the Fed considers a quick start to runoff. My colleague Brian Landy projects that new supply of MBS will run at $60 billion a month. He also estimates the Fed will need to allow runoff in MBS of more than $30 billion a month. Without the Fed or banks to take up an average of $90 billion in incremental supply, the burden would likely fall on mutual funds. Mutual funds do not have the capital to fully take up the slack.

MBS also faces pressure from new, higher loan limits on Fannie Mae and Freddie Mac MBS. Higher balances bring more negative convexity. Fed taper also reduces the amount of negatively convex loans filtered out of the TBA floating supply. The quality of TBA should erode this year, and spreads widen with it.

The view in credit

Credit fundamentals continue to look strong but could start to soften later this year if the Fed aggressively dampens demand. Russia-Ukraine should have limited direct impact on either the US corporate or consumer balance sheet. Corporations have record earnings, good margins, low multiples of debt to gross profits, low debt service and good liquidity. It will be important to watch inflation and see if costs begin to catch up with revenues. A higher real cost of funds would start to eat away at highly leveraged balance sheets with weak or volatile revenues. Consumers last year put on $1 trillion of new debt, starting to releverage the household balance sheet. Rising home prices and rising stock prices have both added to consumer net worth, also now at a record although not equally distributed across households.