The Big Idea

Looking at business inflation expectations

This material is a Marketing Communication and does not constitute Independent Investment Research.

The Federal Reserve spends a great deal of time and energy examining inflation expectations, which are viewed as a key if not primary driver, of longer-term inflation. Policymakers get a read on households’ and economists’ expectations through surveys and on market expectations through TIPS breakevens. The Atlanta Fed also surveys businesses in its district on their inflation expectations. Examining inflation through the lens of price setters offers helpful insight into the Fed’s likely difficult task of bringing price hikes back under control.

Atlanta Fed survey of business inflation expectations

The Atlanta Fed has created a number of data series that have proven useful to financial markets and others interested in the economy including the GDPNow calculation, the Atlanta Fed wage tracker, and the Sticky-Price CPI. Another useful effort by the Atlanta Fed is the Business Inflation Expectations survey.

Each month during the week CPI is released, the Atlanta Fed sends a survey to about 300 businesses of various sizes headquartered in its district. The responses are then weighted by industry share of GDP to ensure a realistic representation across economic sectors.

Among other questions, each respondent is asked to project the change in their business’s unit costs over the next 12 months. Or, more precisely, they are offered five different ranges—down more than 1%, plus or minus 1% to unchanged, up 1% to 3%, up 3% to 5%, and up more than 5%–and asked to assign a probability to each. From the responses, researchers calculate a mean, a median, a mode, and the variance of responses. In addition, once a quarter, panelists are also asked to project the rate of change of their unit costs for the next five to 10 years. The Atlanta Fed has created a series of businesses’ expectations of their unit costs that replicates the year-ahead and long-term inflation expectations results from the University of Michigan survey of households.

It is worth noting that the Atlanta Fed asks directly about firms’ unit costs, not the prices they intend to charge. In a sense, this survey is one step removed from an “inflation expectations” survey. However, inquiring about unit costs is still a valuable exercise, as businesses generally set their prices based on their expectations regarding their costs and some sense of what the market will bear. The second factor is, of course, highly uncertain, but over long periods of time, presumably final prices will rise or fall in rough proportion to changes in unit costs Otherwise, profit margins would fall to zero or widen without end. The Atlanta Fed results become a decent proxy for businesses’ estimates of underlying inflation pressures.

Survey results

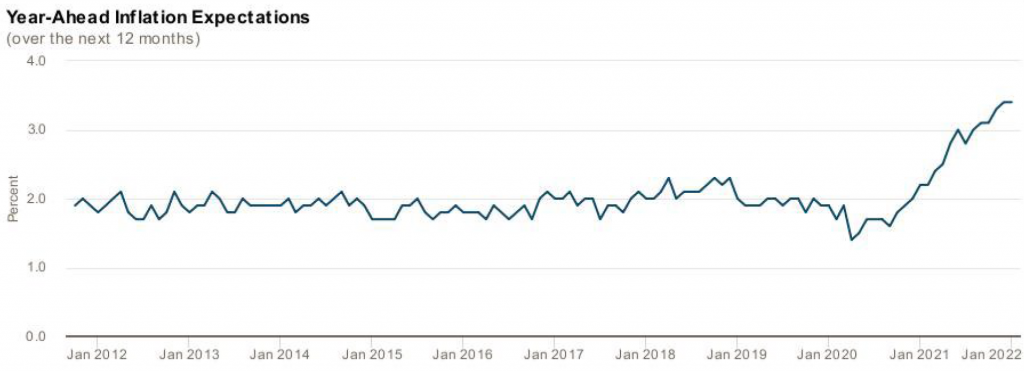

The most recent monthly results, from the survey conducted in January, show that businesses on average expect their unit costs to increase by 3.4% over the next 12 months (Exhibit 1). It ran at roughly 2% for a decade before dipping in early 2020 and has steadily accelerated since then, reaching its current level, a record high, in December. The responses were roughly evenly split between three of the five groupings, with close to 30% each expecting a 1% to 3% rise, a 3% to 5% increase, or a jump of more than 5%. Interestingly, while the level of expectations has trended up, the variance of responses is actually at its lowest in the 10-year history of the survey, which suggests that an elevated pace of cost increases is being endured by a high percentage of businesses of all sizes and in all industries.

Exhibit 1: Atlanta Fed year-ahead business inflation expectations

Source: Atlanta Fed Business Inflation Expectations (BIE) Survey

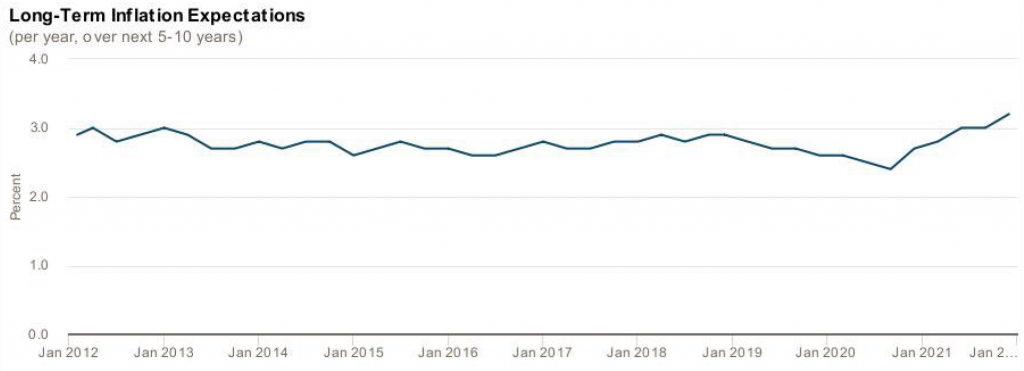

The fluctuations in the longer-term business inflation expectations series have been more restrained. The series ran just below 3% for most of the past decade, dipped in the early days of the pandemic, and have accelerated sharply since late 2020 (Exhibit 2). In the most recent quarterly survey, in December, the average expectation increased from 3.0% to 3.2%, the first time that the series has ever exceeded 3%.

Exhibit 2: Atlanta Fed long-term business inflation expectations

Source: Atlanta Fed Business Inflation Expectations (BIE) Survey

The January 2022 survey also asked a few special questions regarding firms’ workforce and expectations of wages. The expectations regarding wage changes for the next year were especially noteworthy. Respondents anticipate that their low-skill workers will, on average, see 10.2% gains in hourly wages over the next 12 months, while high-skill workers are expected to see 6% advances on average.

Corroboration from the North

The Philadelphia Fed regional survey of manufacturers happened to include a similar set of special questions this month. The results, released on January 20, showed that manufacturing firms anticipate elevated cost increases for 2022. The average expected change in energy costs (6.4%), other raw materials (8.9%), intermediate goods (6.4%), and wage and benefit costs (6.4%) are all quite elevated. In each case, a strong majority of firms expected the rises in 2022 to be larger than the actual cost changes seen in 2021.

Conclusion

The narrative that the inflation bulge in 2021 was predominantly transitory and driven by fleeting supply-side bottlenecks has largely crumbled in recent months. The survey results detailed above offer further proof that higher inflation is likely to have legs. Cost increases are not expected to recede much this year, which presents clear upside risk that any deceleration in price increases could be far smaller than generally expected.

Last week, an economist at the Atlanta Fed, Brent Meyer, was interviewed by Market News International regarding the results of the January Business Inflation Expectations survey. He noted that “I’m starting to be very concerned about what we’re seeing in inflation expectations now.” He cited the wage expectations noted above as evidence that “wage growth has become more broad-based.” He hesitated to invoke the prospect of a 1970s-style wage-price spiral, but he said that “that sort of dynamic is not too far off from what could potentially happen.” He also added that a few firms in the Atlanta Fed District have started to report that their sales were insensitive to price hikes as large as 10%, a sign of sustained robust demand.

In light of the fact that the headline business inflation expectations readings are still only just above 3%, it would appear that, similar to the University of Michigan household survey results and TIPS breakevens, longer-term inflation expectations, while on the high side, are not an urgent problem. However, the underlying detail offers more cause for concern. It appears that labor costs are actually accelerating at a much faster pace, and firms have already demonstrated that, in the aggregate, they have significant pricing power to pass those rising costs along to their customers.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.