The Long and Short

Bank trading revenue dips as loan growth signals recovery

Dan Bruzzo, CFA | January 21, 2022

This material is a Marketing Communication and does not constitute Independent Investment Research.

The big six US money center banks saw trading revenue dip more than expected in the last quarter of 2021, with record-breaking M&A advisory fees offsetting some of the decline. The group continued to release reserves as allowance for loan loss balances edged toward more normal levels; and some banks signaled an improving landscape for loan growth, especially in consumer lending. Shareholders mostly responded negatively to the final results of 2021, although bank stocks are coming off an extended period of growth that lasted throughout most of last year. Spreads on debt barely moved as investors awaited post-earnings debt launches. The banks priced $27 billion in debt for the week ending January 21, with the deals generally well received.

Equity markets reacted negatively to JPMorgan Chase’s (JPM: A2/A-/AA-) fourth quarter 2021 earnings report, as shares were down by more than 5% at today’s market open. Another record-breaking quarter in M&A dealmaking fees failed to offset the disappointment of fixed income trading revenue falling more than expected and non-interest expenses coming in higher than expected. We would caution bondholders not to read too much into the move in share prices for the banks today, as they had appeared somewhat poised for a correction / profit taking following the strong performance over the past year relative to broader markets. JPM reported EPS of $3.33 versus the $2.99 consensus estimate, while top-line revenue of $30.35 billion beat the $30.01 consensus but fell short of the higher end of the range of expectations. The bank released $1.8 billion in reserves against $550 million in net charge-offs for a net benefit to earnings of $1.3 billion, which was a larger contribution than many had been expecting after JPM and its bank peers had already been paring down reserves over the past several quarters. Non-interest expenses were $17.9 billion, up 5% year-over-year and higher than the $17.6 billion consensus estimate, as compensation expenses grew 14% year-over-year. Total trading revenue declined 11% year-over-year to $5.3 billion. That was driven by a larger-than-expected 16% drop in FICC revenue to $3.3 billion, which management attributed to the difficult environment for rates, along with weaker revenue in credit, currencies, and EM versus the prior year period. Equities trading revenue was down 2% to $2.0 billion. Helping offset the weak trading environment, was another record quarter for M&A advisory fees as investment banking revenue shot up 28% Year-over-year to $3.2 billion. M&A advisory fees were up 86% to $1.6 billion. Equity underwriting revenue of $802 million missed estimates, while Debt underwriting was $1.14 billion ahead of expectations. In traditional lending categories growth remains elusive, but JPM saw average loans increase by 6% Year-over-year versus a 17% increase in deposits. Management highlighted card loan growth of 5% and still elevated auto loans up 7%, but supply chain issues continued to impact originations.

Bottom-line: A challenging quarter for the industry’s premiere banking franchise, but we would not read too heavily into the equity move as spreads appear largely unchanged on the day’s earnings reports (and ahead of the issuance that is poised to follow). Our sector weighting view on Domestic Banks remains Marketweight since late 2020, reflecting tighter valuation in spreads and still present headwinds in the industry, such as persistently low rates, constrained loan demand, and the flat albeit improving yield curve. As the nation’s largest lender among US money center banks, JPM remains a core holding within the segment. While JPM is trading tight to peers, the bank’s “fortress balance sheet” and extraordinary capital position, as well as its continued strong performance in the challenging operating environment, dictate its leading stature among US money center banks.

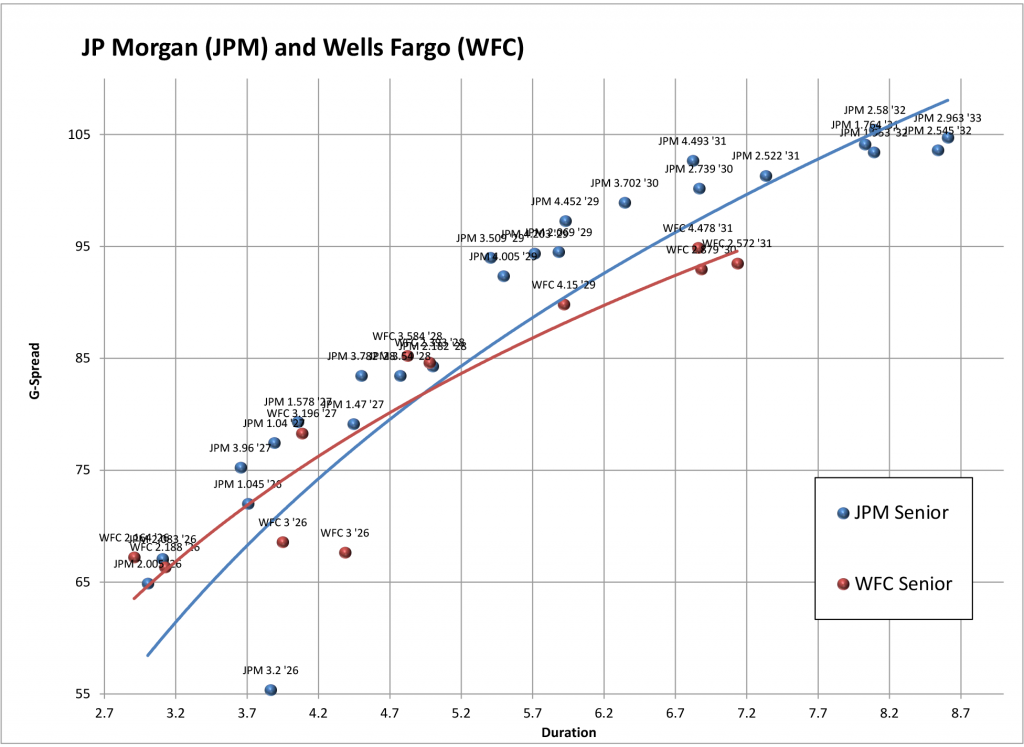

Exhibit 1. We maintain our preference for JPM intermediate paper, as there does not appear enough additional spread available in WFC to compensate for lingering regulatory risk and operational challenges

Source: Amherst Pierpont, Bloomberg/TRACE G-spread Indications

Wells Fargo (WFC: A1/BBB+/A+) top-line performance beat expectations as management trimmed expenses to help bolster the bottom-line. Management also provided enough positive guidance regarding green shoots in lending to stoke a small gain in the share price. Total revenue jumped 13% year-over-year to $20.9 billion, well ahead of the $18.9 billion consensus estimate. WFC’s fourth quarter EPS was $1.38, beating out the $1.12 consensus forecast. Earnings results included several one-time items including an $875 million decrease in the allowance for credit losses, a $943 million net gain on the sale the Corporate Trust Services business, and a $268 million charge on the impairment of leased rail cars. There were no charges this quarter related to the consumer banking scandals of the past. The bank continues to move on from its past misdeeds under new management and toward an eventual turnaround. Total non-interest expenses of $13.2 billion declined 11% year-over-year, as cost reduction efforts directly impacted the bottom line. WFC’s efficiency ratio (all-in cost measure) improved to 63% versus 71% year-over-year and well below the 68% consensus estimate for the quarter. Loan growth remained elusive in the quarter as firm-wide average loans were down 3% year-over-year, due in large part to a 10% dip in consumer loans, and period-end loans increased just 1%, versus the 7% growth in average deposits. Still, management provided some of the most optimistic guidance that we have seen in recent quarters, projecting significant loan growth for the current year.

Bottom-line: WFC is still working toward repairing its severely bruised reputation under new management but continues to make gradual headway. We would be buyers of WFC credit on any short-term or headline-related weakness, but we believe bonds do not currently offer enough discount to JPM to compensate investors for the still present operational and regulatory risks associated with the credit.

Citigroup’s (C: A3/BBB+/A) fourth quarter 2021 earnings results appear to have largely echoed those of JPM, with weaker than expected trading results dragging down the overall performance and stoking a modest sell-off in share price. Likewise also, Citi posted record results in M&A advisory fees throughout 2021, but failed to offset overall weakness in performance in the fourth quarter. Top-line revenue increased just 1% Year-over-year to $17.0 billion, edging out the consensus estimate of $16.8 billion. Adjusted EPS in 4Q21 was $1.99, topping the consensus forecast of $1.62, but net income fell 26% year-over-year to $3.2 billion as operating expenses grew 18%. One-time items included a $1.2 billion pre-tax gain on the sale of Citi’s consumer businesses in Asia and the bank also released $1.4 billion in reserves against $866 million in net credit losses. Fixed income trading revenue declined 20% to $2.5 billion, falling short of the $2.7 billion consensus estimate. Equities trading revenue was down 3% year-over-year to $785 million, also missing the consensus forecast. Investment banking revenue was up 43% year-over-year as M&A advisory fees were $571 million – the best recorded in a decade. Debt underwriting increased 24% year-over-year to $767 million and Equity underwriting increased 16% year-over-year to $507 million. In traditional lending, end-of-period loans were down 1% year-over-year while deposits were up 3%.

Bottom-line: Citi appears to have shaken off the regulatory issues from late 2020, delivering results that have been mostly in-line with peers throughout most of 2021, helping smooth the transition for relatively new CEO Jane Fraser. We maintain our view that Citi remains among the preferred risk/reward picks in the Big Bank peer group, within the context of our Marketweight for Domestic Banks within the IG Index.

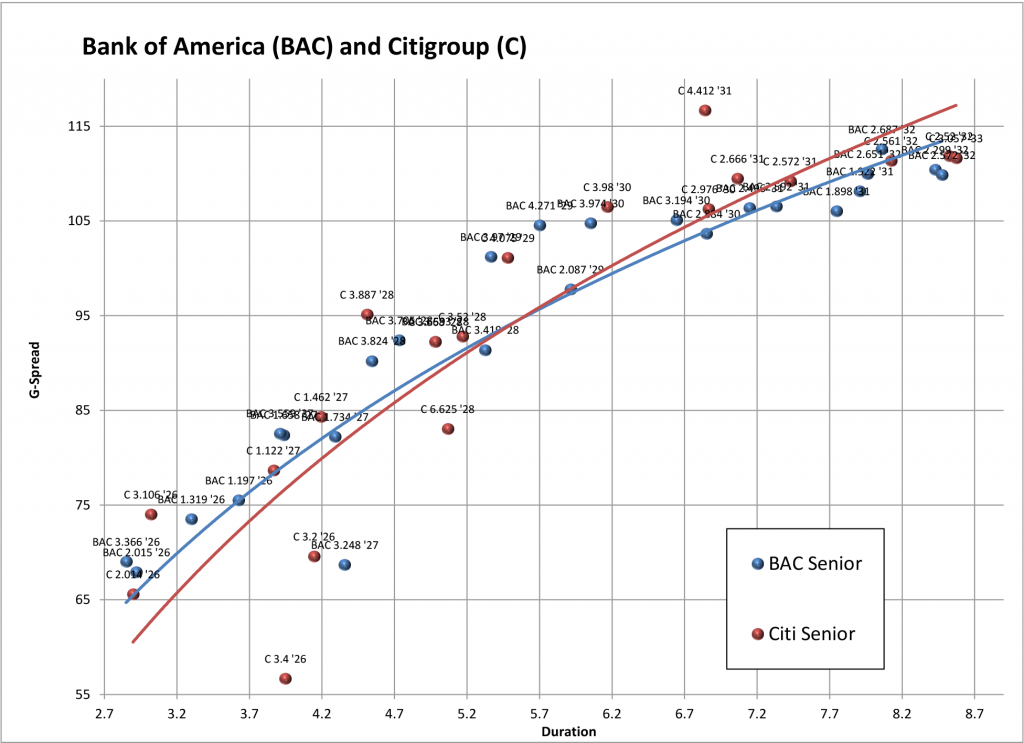

Exhibit 2. We continue to see better risk/reward in Citigroup intermediate paper over Bank of America

Source: Amherst Pierpont, Bloomberg/TRACE G-spread Indications

Despite the outstanding performance versus peers throughout the first three quarters of 2021, Goldman Sachs (GS: A2/BBB+/A) failed to avoid the challenges that were present in JPM and Citi’s results last week. GS shares are down modestly as we approach the market open. Like the other two banks, GS also struggled with weaker than expected fixed income trading revenue, despite another strong performance in investment banking, and higher than expected expenses primarily tied to compensation in 4Q21. Net income declined 13% year-over-year as EPS fell to $10.81 versus the $11.64 consensus estimate. GS managed to beat top-line expectations with a 7.6% rise in net revenue Year-over-year to $12.6 billion versus the $12.0 consensus forecast. Unlike peers that again released reserves to boost earnings, GS took a small provision of $344 million for credit losses. Operating expenses increased 23% year-over-year to $7.3 billion, coming in well ahead of the $6.4 billion consensus estimate, as compensation expenses grew 31% year-over-year to $3.25 billion. Investment banking revenue was up 45% Year-over-year to $3.8 billion, thanks to a 49% year-over-year increase in M&A advisory revenue and an 80% gain in debt underwriting revenue to $948 million. Equity underwriting was down 8% Year-over-year to $1.0 billion. In trading, fixed income was down 1% Year-over-year to $1.9 billion, while equities revenue fell 11% year-over-year to $2.1 billion. We will have to wait until closest peer MS reports later this week to determine if GS maintained the top position for equities trading among the US money center banks – a distinction that has gone back and forth for GS and MS in recent quarters.

Bottom-line: Notwithstanding some of the weakness exhibited in 4Q21, F2021 was an extraordinary year for GS with the bank setting records for revenue and earnings in the first three quarters alone. Undoubtedly, GS has leveled the playing field with its closest peer MS, which had held an edge over GS prior years due to its stronger retail franchise and operational consistency. We continue to see good relative value in GS intermediate bonds versus the broader peer group of US money center banks.

Bank of America (BAC: A2/A-/AA-) provided another consecutive quarter of solid results as net income rose 28% year-over-year to $7.0 billion and loan balances ticked up modestly relative to peers. Shares are up moderately in premarket trading, reacting favorably to the initial headlines, while spreads appear little changed amidst a steady stream of post-earnings supply from the US money center banks. BAC’s 4Q21 EPS was $0.82 versus the $0.76 consensus estimate, while top-line revenue increased 10% to $22.1 billion, falling just shy of consensus expectations. Similar to peers, BAC saw compensation expenses increase 10% year-over-year as the competition to retain talent remains a key theme for the entire industry. The bank released $851 million in reserves against $362 million in net charge-offs for a $489 million benefit to earnings. Allowance for loan losses is now down to $12.4 billion from $13.2 billion sequentially and has steadily declined over the past several quarters with substantial reserve releases since the height of the pandemic. Not surprisingly, BAC’s trading revenue (ex-DVA) fell short of expectations, declining 4% to $2.9 billion versus the $3.1 billion estimate. Fixed income trading revenue fell 10% year-over-year to $1.6 billion, missing the $1.8 billion estimate, while equities trading revenue increased 3% year-over-year and came in slightly ahead of the consensus forecast. Also in line with the broader peer group, BAC saw investment banking fees increase 26% year-over-year to $2.4 billion, led by record M&A advisory fees of $850 million versus a $621 million consensus estimate. The bank’s average loan balance grew 1% year-over-year while average deposits increased 16% year-over-year – a somewhat modest gain in consumer lending but enough to evoke a favorable response from equity investors as a sign that demand is thawing.

Bottom-line: Two consecutive favorable earnings results for BAC appears to have righted the ship versus previous turbulence. We maintain our view that investors continue to be properly compensated for the risk in the name, particularly given the relative stability of the sector amidst a difficult operating environment. However, on a head-to-head basis our preference between the two credits remains with closest peer Citigroup on better risk/reward.

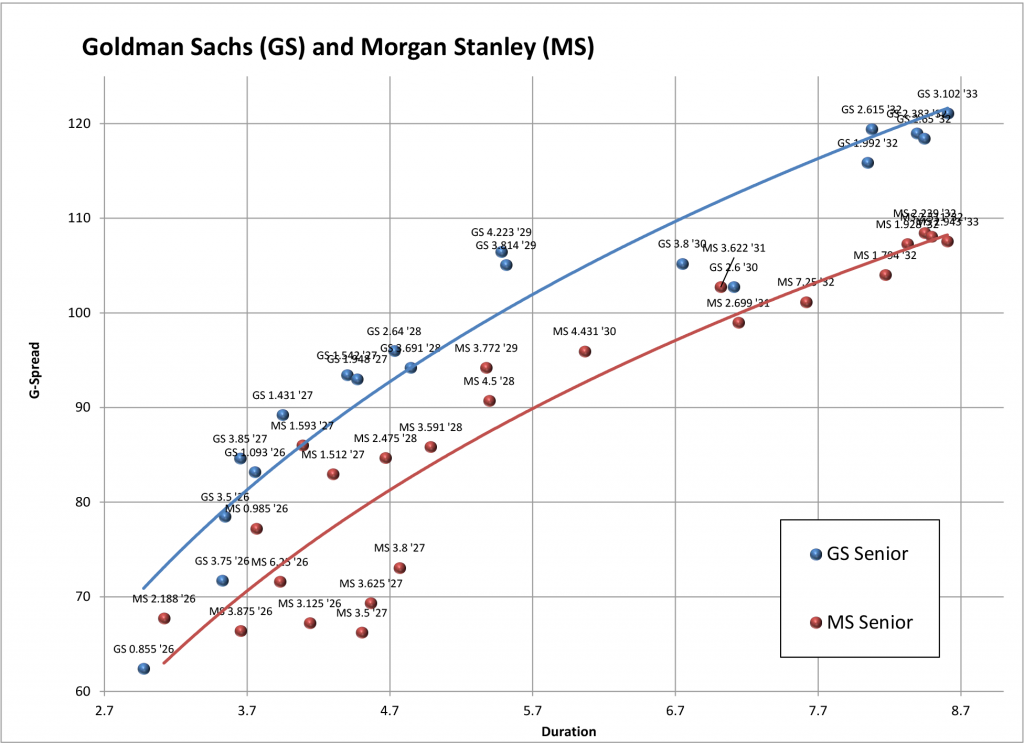

Exhibit 3. Spreads have gotten very tight between GS and MS, but we still prefer the spread pick-up in GS where available in the intermediate part of the curve

Source: Amherst Pierpont, Bloomberg/TRACE G-spread Indications

Morgan Stanley’s (MS: A1/BBB+/A) net income grew 9% year-over-year to $3.7 billion, as the bank saw strong results in equities trading to help offset weakness in fixed income. MS appeared to be less aggressive around compensation than some of its peers in the fourth quarter, as non-interest expenses were up 19% year-over-year, but the increase also included costs related to the ongoing integration of its acquisitions of E*TRADE and Eaton Vance. Top-line revenue increased 7% year-over-year to $14.5 billion, which was slightly ahead of the consensus forecast. Adjusted EPS was $2.08, beating the $1.94 consensus estimate. Investment banking revenue increased 6% year-over-year to $2.4 billion as M&A advisory fees grew 30% Year-over-year to $1.1 billion. That helped offset a 17% year-over-year decrease in equity underwriting revenue at $853 million. Debt underwriting saw a modest gain of 7% year-over-year to $510 million. Equity trading revenue increased 13% year-over-year to $2.9 billion, and once again regained the top spot in the industry versus all US money center peers – most notably closest peer GS ($2.1 billion for 4Q21). That performance helped offset the 31% decline in debt trading revenue to $1.2 billion for the fourth quarter. Contrary to most of the money center banks, compensation expenses across the institutional securities division actually declined Year-over-year to $1.4 billion, which management attributed to deferred compensation plans linked to investment performance. MS continues to stand out versus the broader peer group in wealth management, due to the impact of the E*TRADE acquisition, and investment management, due to the impact of the Eaton Vance acquisition. Those units saw revenue gains of 10% (to $6.3 billion) and 59% (to $1.8 billion), respectively.

Bottom-line: We maintain our view that MS boasts the preferred longer-term franchise for retail brokerage over GS. The integration of both the E*TRADE and Eaton Vance acquisitions continues to be reflected in solid quarterly results. MS and GS both remain core holdings for the US Banking segment–which we currently view as Marketweight. Our trading preference continues to be to target the spread pick in GS over MS seniors in the intermediate part of the curve where available.