By the Numbers

MBS Outlook 2022: A bigger agency footprint with more policy risk

Brian Landy, CFA | November 19, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

Government sponsored lending will likely play an even larger role in mortgage finance in 2022. Higher loan limits should allow agency MBS to capture a larger share of new origination, and government policymakers will attempt to widen the credit box, boost affordability, and increase lending to underserved markets. Tight primary/secondary spreads, falling profits, and possibly heavier regulation should encourage consolidation among mortgage originators. The Fed plans to complete tapering by June but will still own more than 30% of all MBS, and money managers may prove quick to start adding MBS to portfolios. This should keep spreads from widening substantially. Conventional MBS may be more attractive than Ginnie Mae MBS, as the latter faces more perceived, if not real, policy risk.

* * *

A bigger but more negatively convex market in MBS

Agency MBS should grow into a larger share of the broader mortgage market in 2022, but this growth will likely add negative convexity. A large share of loans in private-label MBS, roughly 15% of the balance of prime jumbo 2.0 deals, will become eligible for agency conforming pools if loan limits increase close to 20%. And if all loans in prime jumbo 2.0 deals are in high-cost areas then up to 33% of loans could become eligible for agency execution—either as conforming or jumbo conforming balances. And there are more loans sitting on bank balance sheets that will be newly eligible for agency MBS.

The flow of loans into agency pools should grow agency MBS at the expense of private-label securities and bank portfolios. How fast this happens depends on mortgage rates, but the greater efficiency of agency origination should generally make agency execution more attractive than the alternatives. The higher loan sizes will add negative convexity to agency MBS. This will eventually lower the quality of the TBA as the 2022 vintage grows. That should increase pay-ups to an eroding TBA for specified pools, and originators may start creating specified pools with slightly larger loans.

Negative convexity should also increase as the Fed tapers. The Fed acquires almost all its pools by taking delivery of TBA contracts; as a result, it typically receives the most negatively convex pools from private investors. These pools will flow back into the hands of private investors as the Fed tapers, and the negative convexity of the TBA will increase. After tapering completes, the Fed will continue to buy pools to replace paydowns, but that buying has a smaller effect on the convexity of the TBA compared to purchases that grow the Fed’s portfolio.

TBA investors have enjoyed special dollar roll financing for most of the pandemic, a consequence of the Fed’s heavy buying. But unusual roll specialness is likely to fade by mid-year as the Fed tapers while TBA quality deteriorates, so investors should look to position specified pools. For example, 2019 or 2020 vintage generic pools will have much smaller loan sizes than 2022 production that should eventually dominate TBA delivery. Those vintages also experienced significant home price appreciation, which could lift turnover speeds and add extension protection. In general, low pay-up stories could offer a nice risk-and-reward profile—they stand to gain the most as pay-ups increase due to the weaker TBA and weaker roll, but there is little downside risk since the current pay-up is low.

The administration and its government agencies, like the FHFA and FHA, lean toward policies that expand the reach of government-sponsored lending. The focus will likely be on affordable housing initiatives and boosting homeownership rates, with a specific focus on first-time buyers in underserved communities. For example, the reconciliation package working its way through Congress includes a proposal for a new 20-year mortgage that would be available to first-time, first-generation, homebuyers making less than or equal to 120% of the area median income. Ginnie Mae and the Treasury would subsidize the loan to make the payment comparable to a 30-year mortgage, allowing these borrowers to build equity more quickly. The FHA will explore ways to provide more down payment assistance to certain borrowers, and there have been legislative proposals to fund down payment assistance.

Investors will continue to be concerned about pricing changes at the GSEs and FHA that could lower mortgage costs and increase prepayment speeds. The FHFA and GSEs could tweak their loan-level price adjustments (LLPAs) and the FHA could lower mortgage insurance premiums (MIPs). However, the FHA is at least a few months away from any changes since MIPs were not lowered alongside the FHA’s annual report to Congress. The FHA indicated plans to follow more targeted initiatives until they get more certainty about the resolution of Covid delinquencies. Historically the FHA has not charged different insurance premiums based on income, but it is possible a MIP reduction could be targeted in that way and not lowered for all borrowers. The GSEs are also more likely to take a targeted approach with LLPAs, since the LLPAs paid by better credit borrowers can be used to finance affordability programs. There is little incentive to lower guarantee fees across the board. Instead, the GSEs are more likely to expand programs targeted towards low-income and first-time borrowers.

Many of these loans are likely to have close to 100% LTV ratios and originated after two years of massive home price appreciation. Should HPA continue to roar, then the prepay protection these loans offer will fade quickly. However, those loans should offer extension protection in this scenario, since HPA could fuel turnover, cashout refinances, or a rate-and-term refinance to eliminate mortgage insurance. On the other hand, if home prices were to fall—and the risk may be underappreciated—then these loans would quickly fall underwater. Agency MBS investors do not face the credit risk, but the valuation implications of faster buyouts will depend on the level of mortgage rates. But such a scenario would be problematic for the various government housing agencies.

* * *

Originator consolidation

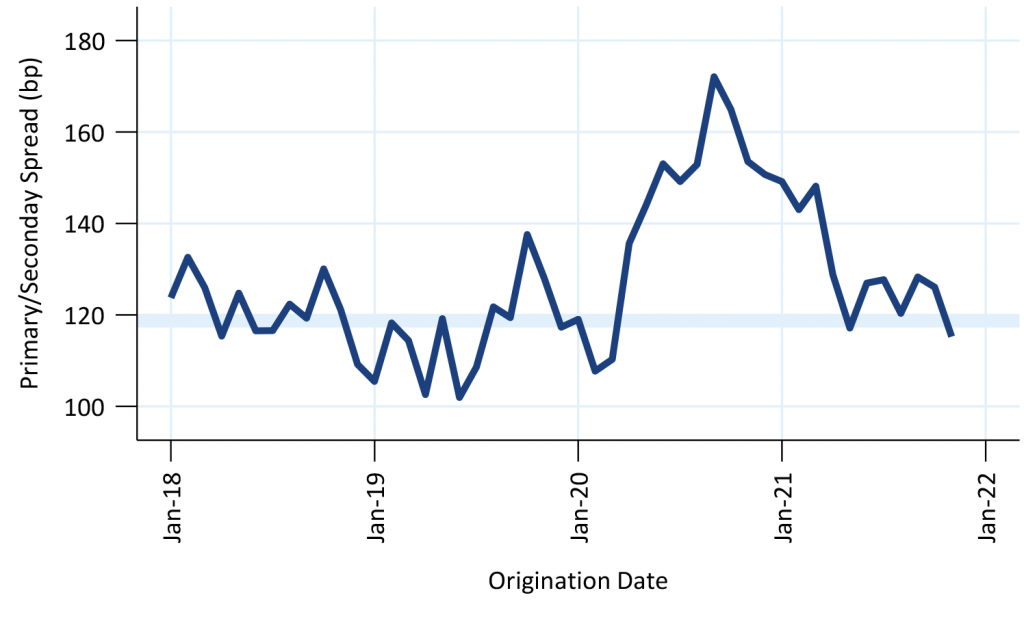

The pressure for originators to consolidate should increase next year. The spread between primary and secondary mortgage rates has fallen back to pre-pandemic levels (Exhibit 1). Originator profits have dropped along with spreads. Origination volumes are also slowing as fewer borrowers have reason to refinance and as tight housing supply has slowed purchase activity. This should push mergers and acquisitions that can eliminate redundancies and save costs.

Exhibit 1. Primary/secondary spreads have returned to pre-pandemic levels

Primary/secondary spread comparing gross WAC of originated 30-year mortgages to a 45-day lagged average of the 30-year MBS current coupon yield.

Source: Amherst Pierpont Securities

Another factor that could push consolidation is heavier regulation. The Financial Stability Oversight Council, for example, is pushing for regulators to require regulated institutions to disclose exposure to climate risk, review climate risk management, and eventually regulators may want institutions to hold more capital against measured climate risk. A heavier regulatory burden typically benefits larger institutions that can afford the costs of compliance, while smaller lenders will need to merge or be acquired. Heavier regulation would also raise the cost of entering the mortgage business. However, this may have a limited role in 2022 as the timeline for some of these initiatives is years away.

Investors will need to keep an eye on MSR trades and M&A activity to anticipate changes in prepayment behavior of the acquired loans. It is likely that the new servicer may be more aggressive about soliciting business than the prior lender. Acquiring lenders are likely to target smaller lenders with slower prepayment behavior, since those servicing portfolios would have been less solicited and therefore likely to have more opportunities to generate business. On acquisition, speeds in the smaller lenders would eventually pick up.

* * *

Money managers balance MBS against corporate debt

The Fed and banks have been net buyers of MBS over the last two years. MBS net supply has been extremely high due to the pace of home sales. At the same time money managers and foreign investors sold a large portion of their MBS holdings, leaving them underweight. The Fed is finally starting to taper purchases and expects to be done by June, although some economists are starting to speculate that inflation will force the Fed to taper faster. The Fed would prefer to finish tapering before hiking rates.

Of course, the response from money managers will almost certainly depend on spreads and the outlook in corporate debt, where managers through the pandemic have gone overweight. Agency MBS may begin to look better than corporates if corporate earnings are disrupted by inflation, labor shortages, and supply chain issues. My colleague Meredith Contente argues that the pandemic has left many corporations with fewer levers to deal with rising inflation, which will squeeze margins. Companies typically offset cost-of-goods increases by cutting operating costs, but many firms cut costs multiple times during the pandemic. And companies will have to spend more on labor costs since many people are refusing to re-enter the workforce. On the other hand, both my colleagues Stephen Stanley and Steven Abrahams see good prospects for corporate margins, with inflation likely to drive up revenues faster than costs.

Conventional MBS should outperform Ginnie Mae MBS

Many factors should favor conventional MBS in 2022. Most Ginnie Mae loans are high LTV, and FHA and rural housing loans could perform poorly if home price growth were to slow or the economy were to falter. A disproportionate share of FHA and rural housing loans recently received assistance during the pandemic and may be poorly positioned to handle another downturn.

Ginnie Mae MBS will also face more perceived, if not real, policy risk. Although the FHA chose not to lower insurance premiums alongside the release of the annual report to Congress, market participants will continue to fear a cut. And a cut may occur in 2022, although contingent on how well the FHA resolves the still-large pipeline of delinquent loans and the ultimate pace of redefaults. And the insurance fund’s capital ratio is highly dependent on home price appreciation. If HPA shifts lower, or negative, then the FHA may not have room to lower premiums.

Finally, the anticipated large jump in loan limits may lower the convexity of Ginnie Mae TBA more than conventional TBA. Although jumbo loans overall are a smaller share of Ginnie Mae production, the loans placed in Ginnie MJM pools have much higher loan sizes than the loans placed in conventional jumbo pools. Most of them are VA loans, and the VA program does not have a maximum loan size. When loan limits increase many loans will be deliverable as conforming, not conforming jumbo, loans. That will permit lenders to include more jumbo VA loans in TBA pools. Since the VA loans are larger than the corresponding conventional loans, the Ginnie TBA’s convexity will drop more than conventional TBA.