The Long and Short

A planned split and a massive tender offer

Dan Bruzzo, CFA | November 12, 2021

This document is intended for institutional investors and is not subject to all of the independence and disclosure standards applicable to debt research reports prepared for retail investors. This material does not constitute research.

A day after announcing plans to split the remaining company, General Electric (GE: Baa1/BBB+*-/BBB) launched a massive $23 billion debt tender offer with proceeds from the recently closed sale of GE Capital Aviation Services (GECAS) to AerCap, in a transaction worth over $29 billion. GE had pledged to direct the bulk of proceeds toward its long-running debt reduction mandate, with a goal to get net leverage below 2.5x.

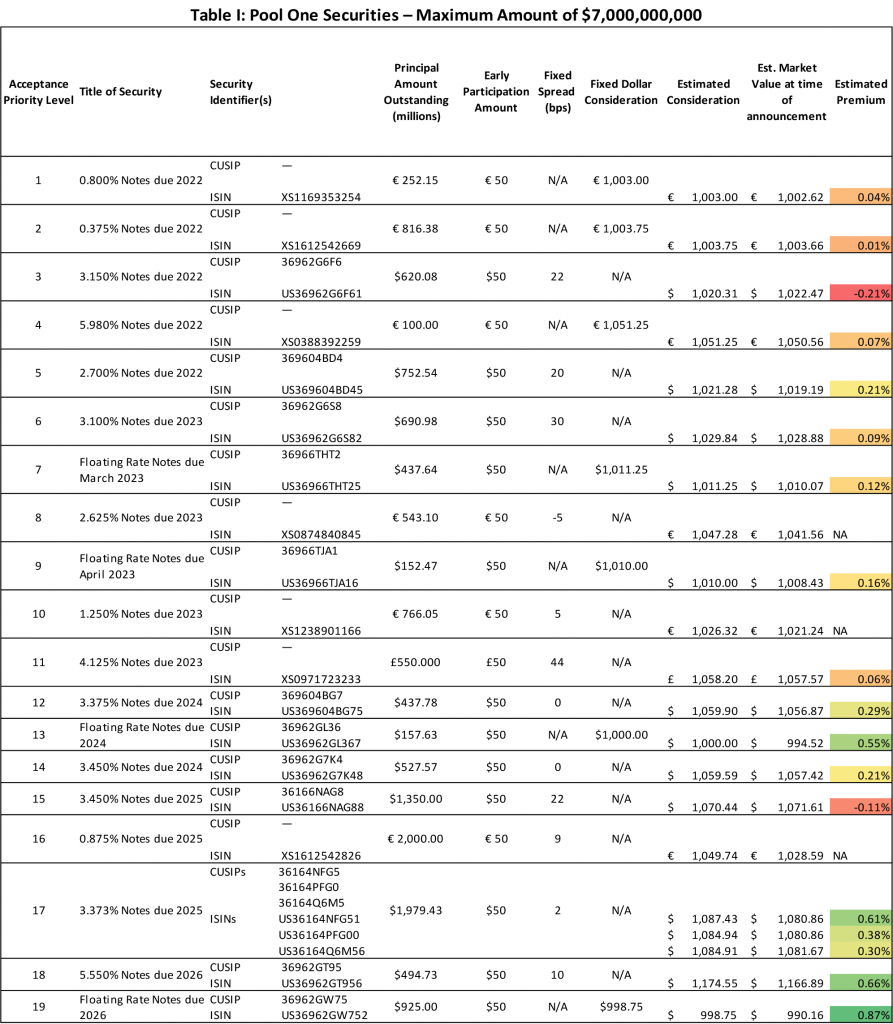

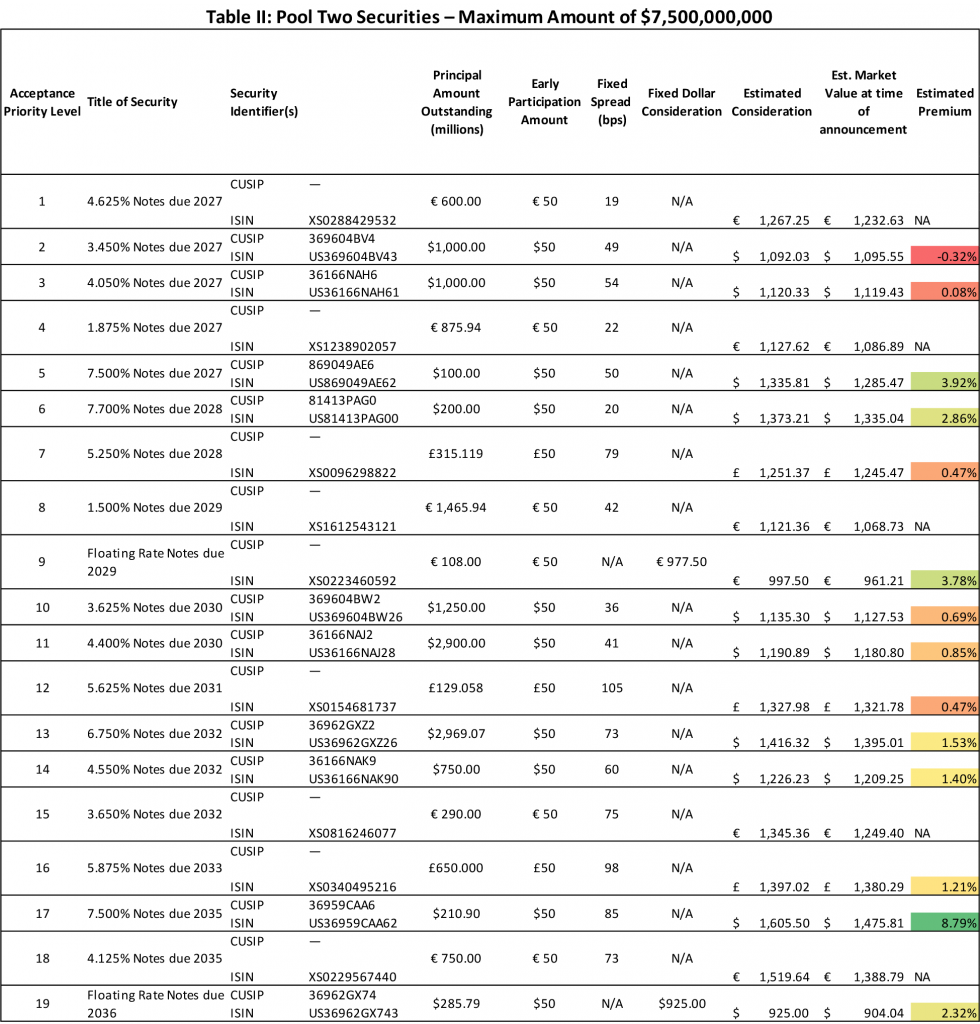

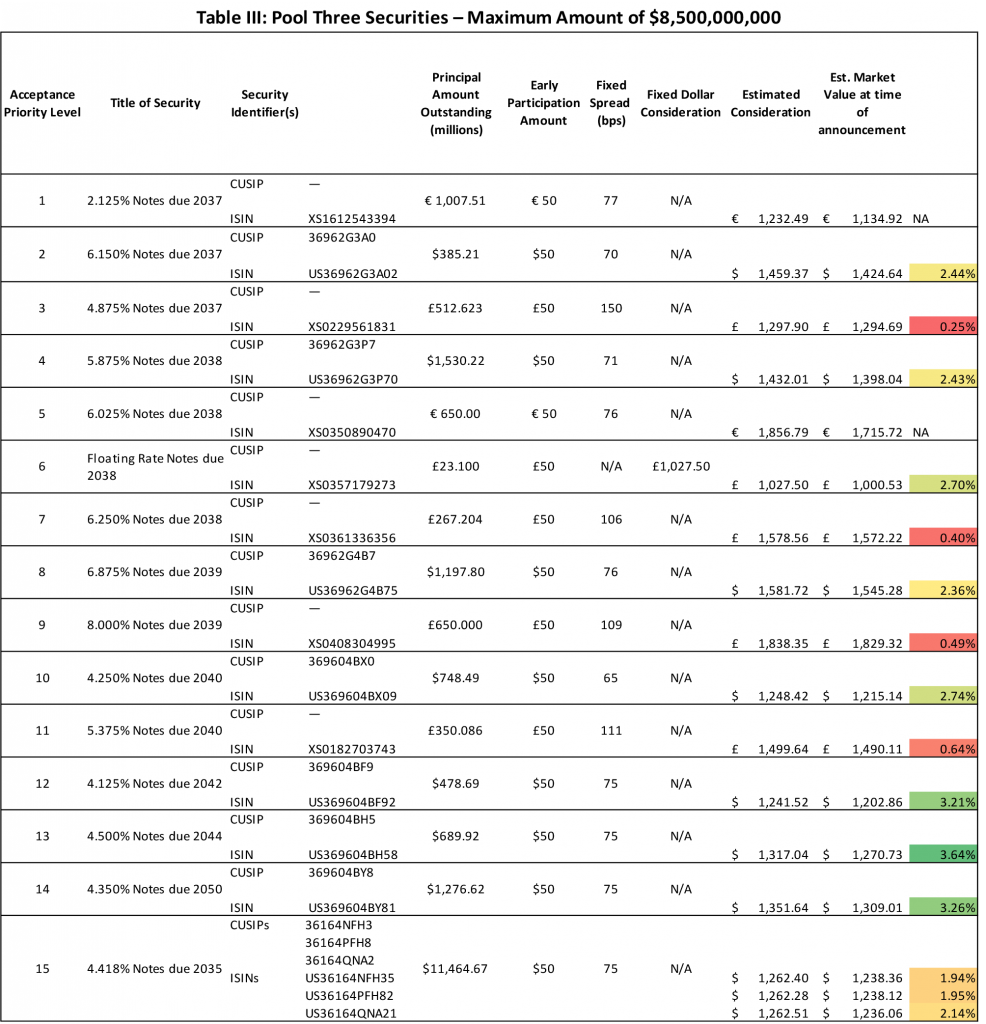

Each tranche of debt included in the three tender pools, along with estimated premiums associated with the tender offer levels over market values at the time of announcement (Wednesday morning 11/10/21), is shown in Exhibits 1-3. GE is seeking to redeem a total of $23 billion across three tender offer waterfalls ($7 billion from Pool I, $7.5 billion from Pool II, and $8.5 billion from Pool III), which will be accepted in the order of the listed priority of acceptance. Many of the issues included in this offer had previously been tendered for in GE’s $7 billion debt repurchase executed back in June of this year.

Key takeaways from the debt tender pools:

- Only about 25% of the total principal amount tendered for is in the front-end of the curve (<5-year maturities), the remaining 75% is in intermediate-to-long end. This at least initially indicates GE is taking a more balanced approach to debt reduction rather than focusing strictly on upcoming maturities.

- Not surprisingly, most of the front-end debt tranches being targeted in Pool I are being offered with very limited premium over market prices.

- The GE 4.418% ‘35s and the GE 3.373% ‘25s are at or near the bottom of their respective tender priorities (15, 17). This is relevant not just given the large size of the respective debt deals ($11.5 billion, $2 billion), but the fact that these securities were issued out of GE Capital International Funding Co (guaranteed by GE Co) during GE’s large-scale recapitalization in 2015. Some market participants had been projecting that these debt tranches would have a high priority in the tender offer given that they are the last remaining vestiges of the old GE Capital Corp and therefore most closely linked to the jettisoned GECAS operations from which the proceeds are being used to pay down debt. These debt tranches are also the only GE issues that remain outstanding that still qualify as “finance companies” in the Bloomberg Barclays IG Index.

- High coupon intermediate debt is being offered with some of the more attractive premiums in the debt tender. This includes Priority Level 5, 6 and 17 in Pool II.

- Floating rate notes also appear to have attractive premiums to current market value according to the study. These include Priority Level 13, 18 and 19 in Pool I, Priority Level 9 in Pool II and Priority Level 6 in Pool III.

- The long-end debt deals that had already previously been included in the June tender offer also appear to be offering some of the more attractive premiums to current market pricing. These include Priority Level 12, 13 and 14 in Pool III.

Exhibit 1.

Source: Bloomberg LP, Company Press Release, Bloomberg/TRACE BVAL pricing; bonds priced off interpolated Rate not included in premium study.

Exhibit 2.

Source: Bloomberg LP, Company Press Release, Bloomberg/TRACE BVAL pricing; bonds priced off interpolated Rate not included in premium study.

Exhibit 3.

Source: Bloomberg LP, Company Press Release, Bloomberg/TRACE BVAL pricing; bonds priced off interpolated Rate not included in premium study.

The announcement came just a day after GE revealed plans to break-up the remaining company into three distinct business units via two planned tax-free spinoffs over the course of the next two years. GE Aviation will be the remaining business after first spinning off the GE Healthcare business in early 2023 and retaining a 20% stake. A year later, GE will spin-off the GE Energy businesses in early 2024. The company will incur estimated one-time separation costs of $2 billion and tax costs of under $500 million for the restructuring. Each of the new standalone companies will issue debt securities and use the proceeds to pay down additional debt outstanding at the remaining GE entity. A lot remains unknown about the prospective capital structures of the three separate entities, and whether management’s long-held plan of achieving single-A ratings still applies to the remaining GE entity. So far management has only indicated that they anticipate investment grade ratings, without providing further detail. Following the separation announcement, S&P placed the BBB+ rating on watch negative reflecting the uncertainty of the new plans, while Moody’s affirmed the Baa1 rating and left the outlook negative.