The Big Idea

Implications of higher agency loan limits for volatility

Steven Abrahams | October 22, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The options market and other places where investors delta hedge risk have long kept an eye on the mortgage market and its potential to add to volatility. A nearly 20% rise in agency loan limits next year should push up demand for options and delta hedging from mortgage servicers, originators and investment portfolios that hedge mortgage risk. For other risk assets, rising volatility often means wider spreads.

Both realized and implied rate volatility have depended at times on negative convexity in mortgage loans and MBS. Portfolios that hedge mortgage risk spread the volatility created by negative convexity to other parts of fixed income. The heavy refinancing waves of 2003 and efforts by Fannie Mae, Freddie Mac and others to hedge mortgage risk have imprinted the relationship on market memory. The state of mortgage negative convexity consequently has become key to anticipating shifts in market volatility.

The rapid rise in US home prices through pandemic has almost surely lifted potential negative convexity in all US mortgages and MBS. Part of the lift comes from record levels of home equity, making it easier to refinance when opportunity arises. And part of the lift comes from the larger loans needed to finance more expensive homes. Since the early 1990s, the market has recognized that larger loans refinance much faster than average for a range of reasons—their ability to recoup fixed costs faster, their larger stream of absolute savings, even their tendency to come from certain states.

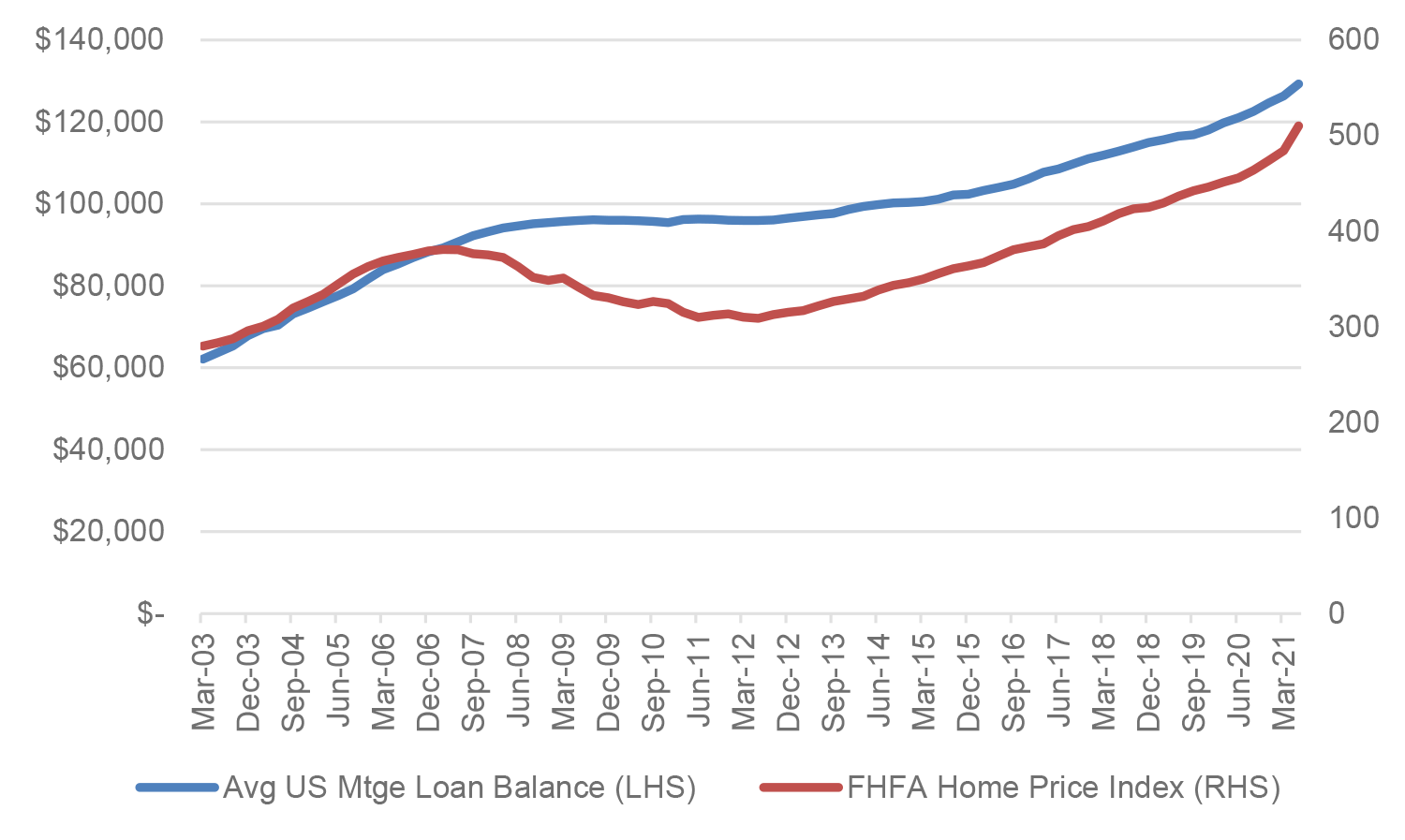

Rising loan balances and increasing potential negative convexity in mortgage loans and MBS is not new even though it has become more pronounced lately. The average US mortgage balance rose almost lockstep with rising home prices from 2003 into 2007 (Exhibit 1). After home prices then fell into 2012, the average mortgage balance plateaued. And when home prices started rising again after 2012, loan balances started rising again, too. The steady climb in loan balance has steadily created more potential negative convexity in mortgage debt and MBS.

Exhibit 1: Rising home prices lift the average US mortgage balance

Note: Average US Mortgage Loan Balance calculated by taking the amount of consumer mortgage debt outstanding and dividing by the number of consumer accounts reported in the New York Fed Consumer Credit Panel/Equifax.

Source: NY Fed, FHFA, Amherst Pierpont Securities.

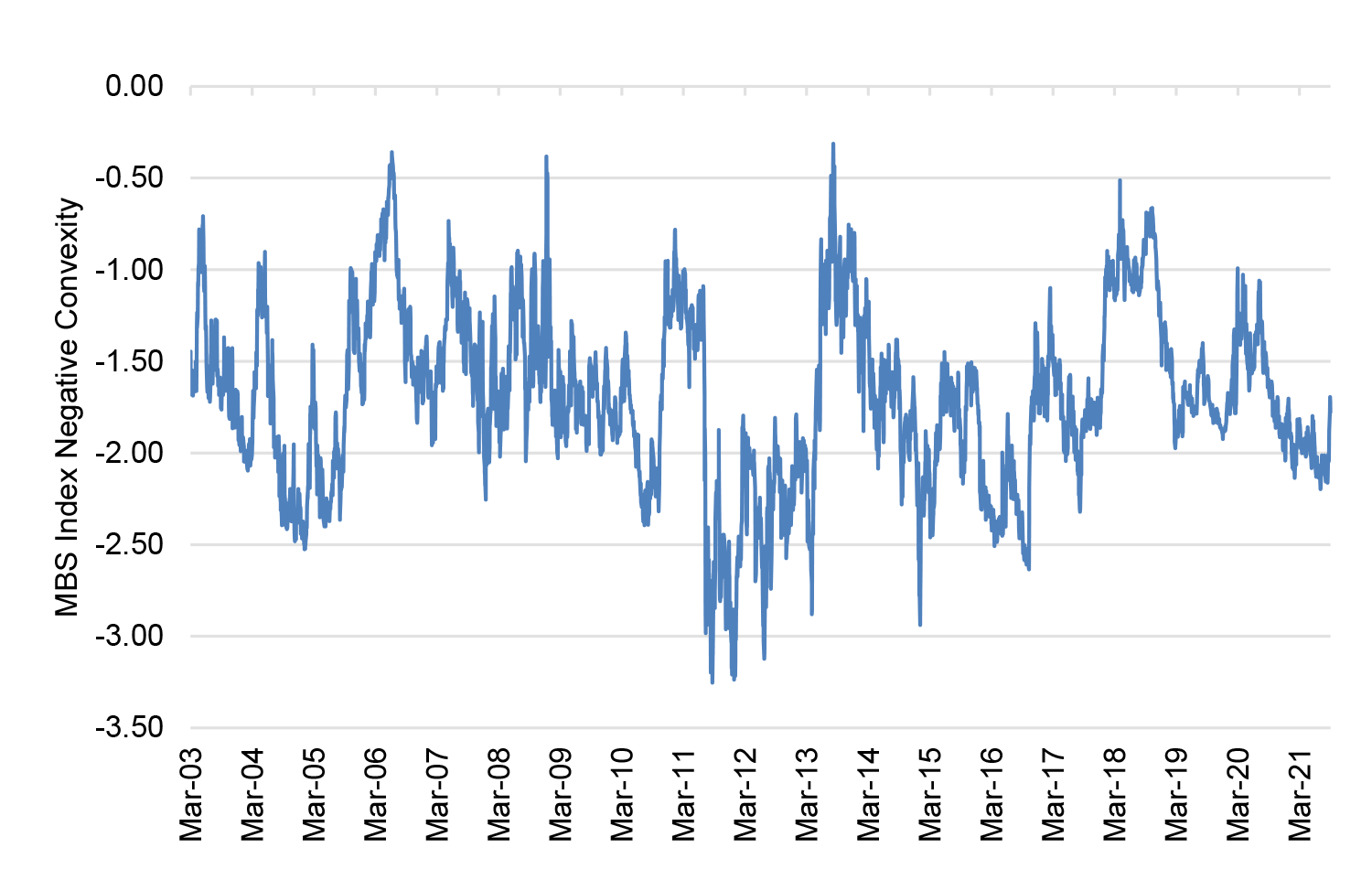

Realized negative convexity has also depended on interest rates. If rates suddenly shift and give most outstanding loans either very large refinancing incentives or none at all, negative convexity declines. It is only when prevailing mortgage rates are roughly at the average of outstanding loan rates that realized negative convexity peaks. At that point, modest shifts in rates can significantly raise or lower prepayment speeds. And in the last few decades, negative convexity has varied with interest rates without an obvious trend higher—despite a steady rise in loan balances (Exhibit 2). For now, mortgage negative convexity is well below historic peaks and roughly at its average of the last two decades

Exhibit 2: Mortgage negative convexity has varied without a clear trend higher

Source: Bloomberg Barclays US Mortgage Index, Amherst Pierpont Securities

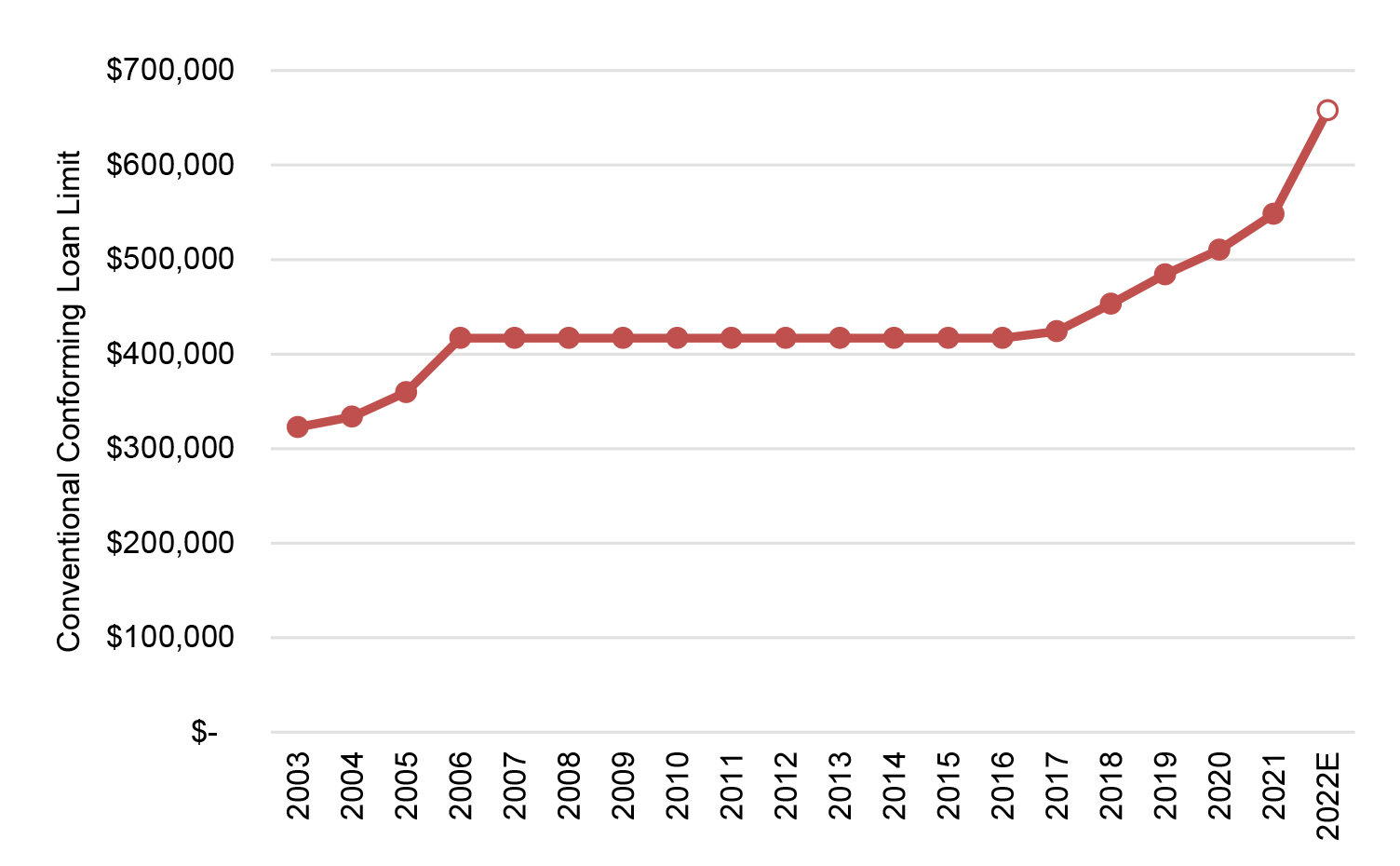

Even though mortgage negative convexity right now is around its average, the active hedging of negative convexity is likely to rise on the margin because of one thing: the likely sharp rise in Fannie Mae, Freddie Mac and Ginnie Mae loan limits. After home prices peaked in 2006, for instance, Fannie Mae and Freddie Mac conventional conforming loan limits plateaued for a decade at $417,000 until prices recovered (Exhibit 3). Limits have moved up since 2016, but a likely 20% jump in 2022 should take the limit close to $658,000—and in expensive markets such as New York or San Francisco, closer to $1 million.

Exhibit 3: Conventional conforming loan limits should jump in 2022

Source: Amherst Pierpont Securities

Agency loan limits shift negative convexity from outside to inside the agency mortgage market. And once inside the agency market, active hedging of mortgage risk increases in a few places:

- Agency MBS securitization creates origination pipelines, where negative convexity is usually hedged

- Agency MBS securitization creates servicing strips, where negative convexity is usually hedged, and

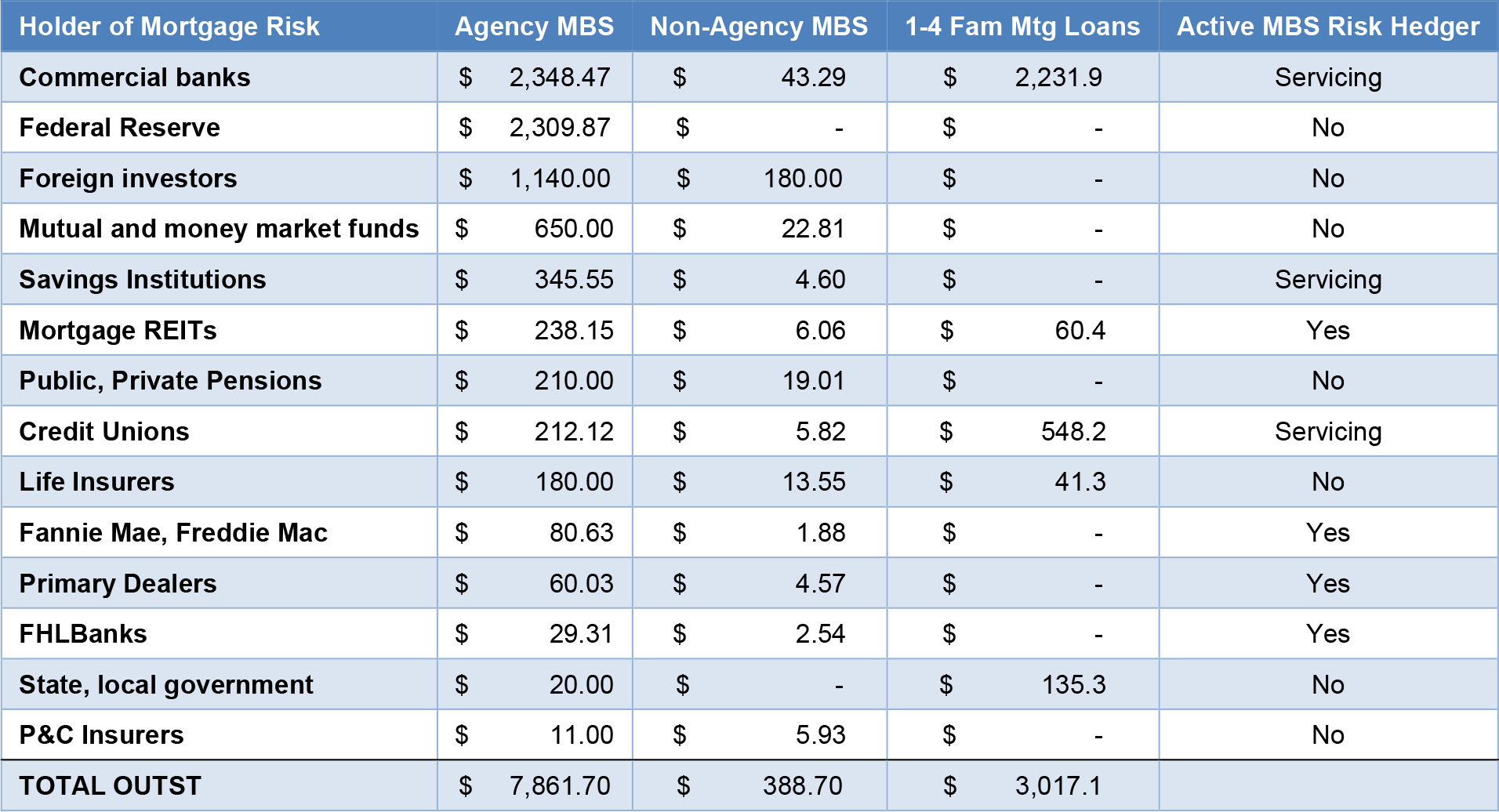

- Agency MBS put negative convexity on balance sheets, such as the FHLBanks, REITs and broker/dealers, that are much more likely to hedge than the balance sheets that held the risk before in loan or non-agency MBS form, such as banks or insurers (Exhibit 4)

Exhibit 4: Holders of mortgage risk vary in their tendency to hedge negative convexity

Note: All figures in $million as of the end of 2Q2021. Although banks and other depositories are not active hedgers, except for servicing, shifts in mortgage duration will often trigger adjustment of balance sheet interest rate risk over time.

Source: Inside MBS & ABS, Federal Reserve Z.1, Amherst Pierpont Securities

The jump in agency MBS loan limits next year should raise demand for interest rate options or lead to more delta hedging by mortgage originators, servicers and by the FHLBanks, REITs, broker/dealers and others that try to limit net MBS duration exposure. Hedging by FHLBanks, REITs and broker/dealers could also get magnified by Fed tapering, which my colleague Brian Landy points out removes a portfolio from the MBS market that has absorbed an important part of the market’s negative convexity since the launch of new QE in March 2020. All else equal, implied and realized volatility should rise.

Rising implied and realized volatility has important implications for MBS and other risk assets, where spreads usually widen with volatility. Owners of risk asset should consider reducing exposure or getting long options to offset risk in 2022.

* * *

The view in rates

The Fed RRP continues to soak up a healthy amount of system liquidity. After peaking at $1.6 trillion on September 30, it is closing Friday at $1.403 trillion. The recent rise in rates has left RRP yields of 5 bp now below the yields on T-bills beyond November, a potential drag on balances. However, RRP is now yielding more than SOFR, which closed Friday at 3 bp.

Settings on 3-month LIBOR have closed Friday at 12.388 bp, a level toward the middle of the recent range. LIBOR clearly is trading with an eye on transition to other benchmarks by June 30, 2023. All interdealer swap trades have moved to SOFR effective October 22, with dealers, banks and others urged to create no new LIBOR exposures after December 31 this year.

The 10-year note has finished the most recent session at 1.63%, up 6 bp from a week ago. The market has been absorbing the FOMC and its intent to taper and hike, and it has been reassessing inflation. Breakeven 10-year inflation is at 264 bp, up 8 bp in the last week and at its peak for the year. The 10-year real rate finished the week at negative 100 bp, down from negative 99 bp a week ago.

The Treasury yield curve has finished its most recent session with 2s10s at 118 bp, unchanged on the week, and 5s30s at 87 bp, flatter by 5 bp on the week.

The view in spreads

The bullish case for credit and the bearish case for MBS continues. Corporate and structured credit has held spread through most of the year despite the steady approach of Fed tapering. MBS, on the other hand, generally widened from the end of May before starting to tighten after the September FOMC.

The difference is partly in the composition in demand across the sectors and in strong corporate fundamentals. The biggest buyers of credit include money managers, international investors and insurers while the only net buyers of MBS during pandemic have been the Fed and banks. Credit buyers continue to have investment demand. Demand from Fed and banks should soften as taper begins, Once the Fed shows it hand on the timing and pace of taper, the market should be able to fully price the softening in Fed and bank demand and spreads should stabilize. But something else is on the horizon.

MBS stands to face a fundamental challenge in the next few months as the market starts to price the impact of higher Fannie Mae and Freddie Mac loan limits. Home prices are tracking toward a nearly 20% year-over-year gain, which should get reflected in new agency loan limits traditionally announced in late November for loan delivered starting January 1. The jump in loans balances should add significant negative convexity to the TBA market and increase net supply. And this will come just as the Fed leans into tapering, which will take out a buyer that often absorbed the most negatively convex pools from TBA and a large share of net supply. The quality of TBA should deteriorate and the supply swell.

The view in credit

Credit fundamentals continue to strengthen. Corporations have record earnings, good margins, low multiples of debt to gross profits, low debt service and good liquidity. The consumer balance sheet now shows some of the lowest debt service on record as a percentage of disposal income. That reflects both low rates and government support during pandemic. Rising home prices and rising stock prices have both added to consumer net worth, also now at a record although not equally distributed across households. Consumers are also liquid, with near record amounts of cash in the bank. Strong credit fundamentals may explain some of the relatively stable spreads.