The Long and Short

Paving a green path forward with Johnson Controls

This material is a Marketing Communication and does not constitute Independent Investment Research.

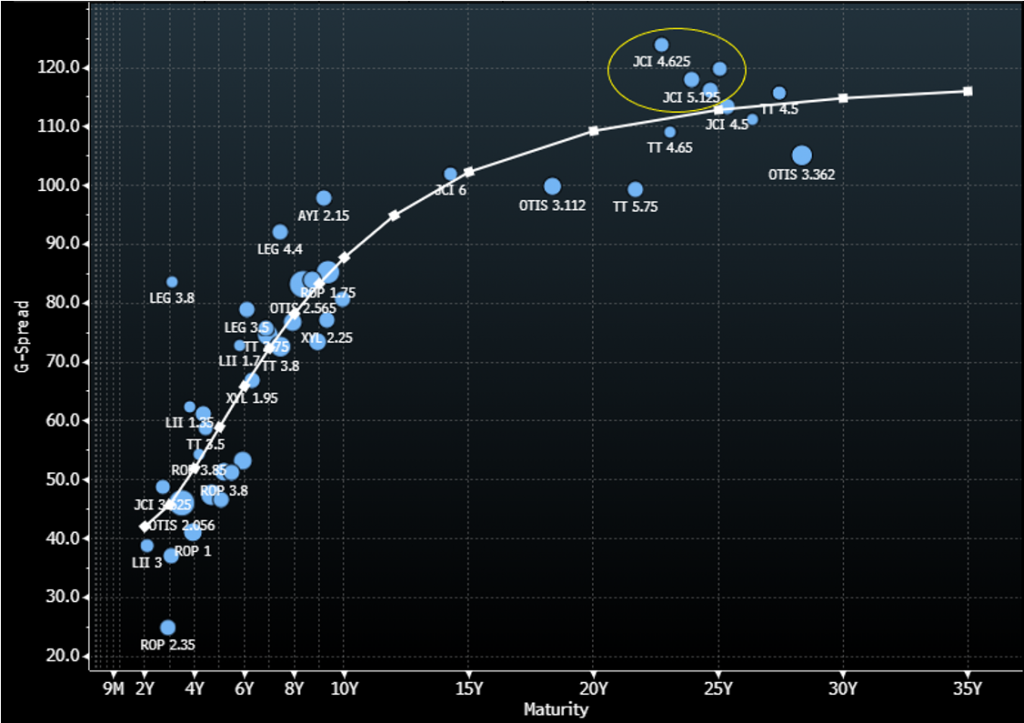

JCI (Baa2/BBB+) is market leader in the evolution of smart, healthy and connected buildings, a need that grew exponentially due to the pandemic. A broad synergistic portfolio which encompasses HVAC, controls, fire and security has enabled JCI to address building needs globally. JCI has demonstrated their leadership in ESG sustainable solutions as companies look to reduce their carbon footprints while operating healthy buildings post-pandemic. Company management believes these two factors present a $250 billion market opportunity over the next decade, which is expected to provide for meaningful top line growth. JCI’s curve remains one of the steepest versus peers such as Otis Worldwide Corporation (OTIS – Baa2/BBB) and Trane Technologies (TT – Baa2/BBB), despite being rated one notch higher at S&P and having the best long-term growth prospects. Relative value investors should move into JCI’s long dated bonds as its curve is likely to compress closer to peers.

Aiding the medium term outlook, roughly 54% of JCI’s revenues are recurring in nature due to its services business, which helps to provide for stability to cash flows. Management is forecasting revenue growth of 6%-7% on a CAGR basis over the next three years and EBITDA margin expansion of 250 to 300 bp over the same time period.

Exhibit 1. BBB Diversified Manufacturing Curve

Source: Bloomberg TRACE; APS

Buildings Play a Crucial Role in Decarbonization Efforts

The building sector represents approximately 40% of the global carbon footprint. With most companies and governments laying out ESG framework for net zero carbon emissions, JCI believes the global decarbonization segment is a $240 billion market over the next decade. HVAC technology solutions will likely be the largest component, representing about 39% of the addressable market, a clear opportunity for JCI given its expertise in HVAC & Controls. This will come from a combination of improving the installed base to achieve the reductions necessary as well as new innovation on how the infrastructure is designed moving forward.

JCI is employing a two-pronged approach by electrifying and digitalizing buildings, which is where JCI’s OpenBlue digital platform comes into play. OpenBlue includes a full spectrum of sustainability offerings tailored to schools, campuses, data centers, healthcare facilities as well as commercial and industrial buildings. The digital platform analyzes energy, water, materials and GHG emissions while helping to optimize siloed pieces of equipment, bringing them together as a whole system. Digitizing existing systems enables them to communicate effectively with power grids, once the systems have been electrified. The communication is necessary in order to not overburden power grids. OpenBlue helps to deliver an additional 50% of efficiency on top of what any single piece of equipment can achieve. JCI is uniquely positioned to offer OpenBlue as an “as a service” model that can help customers with risk management tools while delivering a net zero outcome, for a recurring monthly fee. The demand is likely to be strong for this service, thus increasing the company’s recurring revenue base.

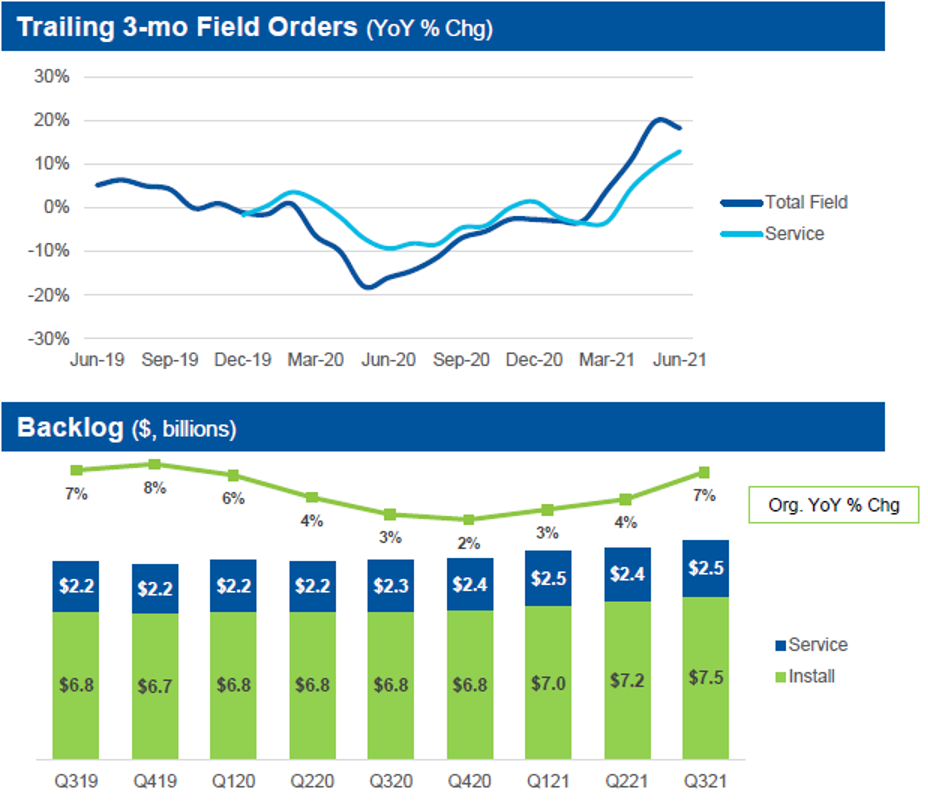

Backlog Hits Record – Growth Exceeding Pre-Pandemic Levels

End markets have continued to improve since 2020 and order growth has accelerated largely driven by retrofit demand. New construction is beginning to recover, but those projects tend to be longer in nature and demand is really in short cycle projects. JCI reported in the most recent quarter that field orders were up 18% year-over-year, while service orders were up 13% and install orders were accelerating at 23%. This has led to a record backlog of $10 billion, which is up 7% year-over-year on an organic basis, with roughly 75% of the backlog related to install base orders. JCI noted that retrofit or smaller turn projects in North America were up 30% year-over-year which has been a big driver of their install business. Looking to 4Q, management does not expect to witness any slowdown in order growth.

Exhibit 2. JCI Field Order Growth and Backlog

Source: JCI Fiscal 3Q Earnings Presentation

For the quarter, JCI posted strong organic sales growth of 15%, which we note was above the overall growth rate witnessed in 2019. JCI witnessed solid growth across all segments with its Global Products unit posting the strongest growth rate of 21%. Solid operational execution in the quarter led to a 30bps increase in the EBITA margin, to 16.2%. JCI is forecasting similar margin growth in fiscal 4Q. For the full year, EBITA margin growth is expected to be in the 80 to 90 bp range on mid-single digit sales growth. JCI raised EPS guidance once again to the $2.64-$2.66 range (up from $2.58-$2.65), which translates to 18%-19% growth from 2020.

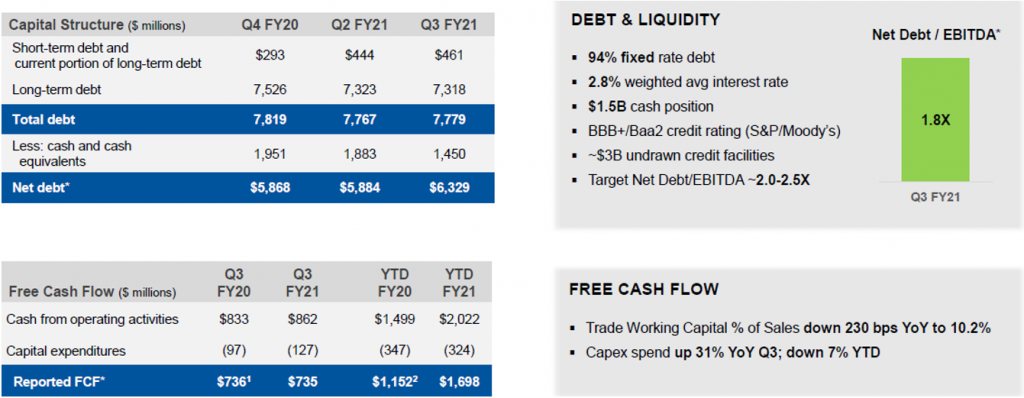

Strong Balance Sheet and Disciplined Capital Allocation Policies

JCI targets a credit rating of high BBB and maintains a strong balance sheet with a net leverage target in the 2.0x-2.5x range. We note that currently JCI is under their net leverage target as they ended the most recent quarter with net leverage of 1.8x. Liquidity also remains strong as JCI ended the quarter with $1.5 billion of cash on hand and $3 billion of availability under its revolvers. JCI has no debt maturing for the remainder of the calendar year or in 2022. The company’s next real debt maturity is not until 9/15/23, when EUR 888 million comes due. Liquidity has also been boosted by strong free cash flow generation, which totaled $1.7 billion year-to-date. This compares very favorably to the $1.1 billion posted in the year-ago period.

Management has explicitly stated that preserving a strong capital structure and green financing instruments remains critical to their financial policies. As such, JCI’s most recent debt issuance was a $500 million sustainability linked bond (SLB) where the coupon steps 12.5 bp annually on 3/16/26 if the company has not met its Scope 1 and Scope 2 key performance indicators (determined by an external verifier) and an additional 12.5 bp if Scope 3 performance targets are not met. We have seen a rise in SLB issuance which essentially holds management teams accountable for achieving ESG goals or compensate bondholders with increased interest payments.

Exhibit 3. JCI Capital Structure & Liquidity

Source: JCI Fiscal 3Q Earnings Presentation

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.