The Big Idea

Managing (inflation) expectations

Stephen Stanley | October 15, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The run-up in inflation during pandemic has been shocking. Opinion is sharply divided, even within the FOMC, over whether the acceleration will prove fleeting or persist longer than expected. One of the arguments by more dovish Fed officials that inflation is not worrisome is that long-term inflation expectations are stable, preventing current inflation from becoming embedded in firms’ pricing strategies. Recent research by the New York Fed suggests longer-term inflation expectations remain steady. However, it is not entirely clear how compelling the case is for well-anchored consumers’ inflation expectations.

New York Fed Consumer Expectations Survey

The standard tools that economists employ to measure inflation expectations have been TIPS breakevens, surveys of economists and surveys of consumers. Of the three, TIPS breakevens offer the richest and timeliest data, but there is plenty of noise, as TIPS breakevens reflect a variety of liquidity and volatility premia that make them imperfect as a measure of pure inflation expectations. Consumer surveys are generally the other main source of data. The University of Michigan survey is the most widely watched indicator. It polls 1-, 5- and 10-year inflation expectations monthly.

Fed officials and private economists generally view 1-year inflation expectations as overly sensitive to current figures. Whenever prices surge, usually due to a spike in energy costs, 1-year inflation expectations tend to rise substantially. However, if the price spike is viewed as largely fleeting, as all price accelerations have been for several decades, then longer-run inflation expectations should remain steady.

The New York Fed began monthly household surveys in 2013, asking about a variety of economic topics, including inflation expectations. The monthly results report 1- and 3-year-ahead inflation expectations.

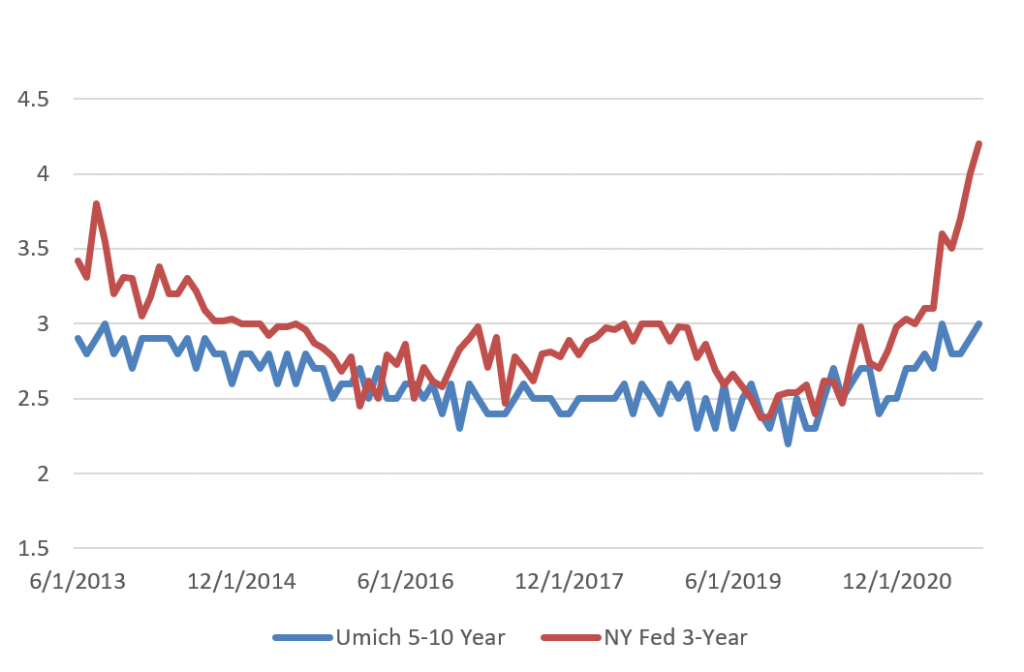

Recently the results of the survey have created a bit of a prickly situation for the Fed. While the University of Michigan long-term inflation expectations gauge has inched higher over the past 18 months, the levels are merely back to where they were earlier in the last decade and, in the view of the leadership at the Fed, “broadly consistent with the Committee’s (FOMC’s) longer-run inflation goal” (from the September FOMC minutes). In contrast, the New York Fed’s 3-year inflation expectations gauge has shot up by over 150 bp since the beginning of the pandemic (Exhibit 1).

Exhibit 1: The NY Fed survey shows rising consumer inflation expectations

Source: University of Michigan, New York Fed.

This has clearly created a certain amount of indigestion among more dovish FOMC members, including, as it happens, New York Fed President Williams, who have been arguing that inflation expectations offer reassurance.

Commissioning a closer look

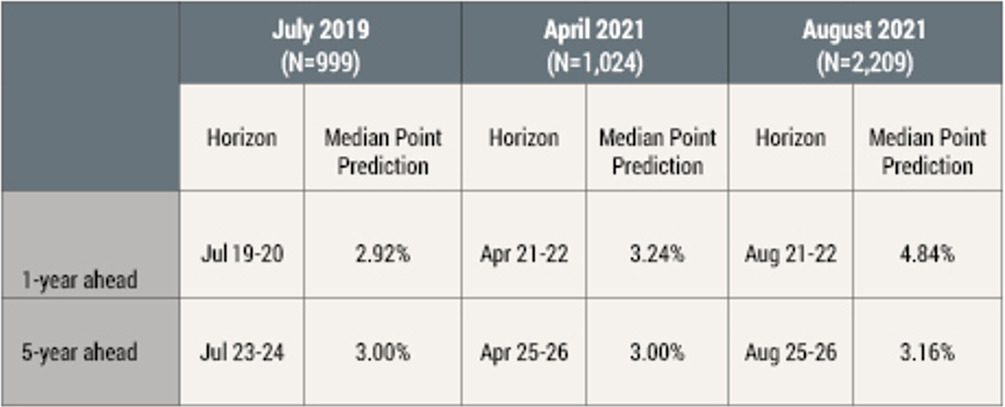

Researchers at the New York Fed recently published a piece taking a more detailed examination of the bank’s consumer survey results for inflation expectations. As it turns out, the New York Fed’s Survey of Consumer Expectations includes, in addition to the regular monthly questionnaire, periodic special surveys that ask supplemental questions. The bank’s research staff has additional unpublished data on inflation expectations that are examined in the New York Fed research paper. In particular, there were three special surveys, in July 2019, April 2021 and August 2021 that asked respondents to provide inflation expectations for the 1-year period four years ahead. So, for example, in the August 2021 survey, consumers would have been asked to predict inflation for the period between August 2025 and August 2026. The paper shows that while 1-year inflation expectations have shot up from about 3% before the pandemic to almost 5% by August of this year, the median expectation for inflation in Year 5 have barely crept higher.

Exhibit 2: Median short-run and long-run inflation expectations

Source: Federal Reserve Bank of New York Survey of Consumer Expectations (2013-2021).

How compelling are these results?

These results are encouraging in that they suggest that consumers for the most part are not projecting the recent surge in inflation out very far into the future. However, it may be a little too soon to think that households would have made any definitive assessments about higher prices. It will be important to see what responses look like six or 12 months from now, assuming inflation keeps running far above recent ranges.

In addition, until this summer—about the time of the most recent special survey—the surge in inflation was very narrowly based, driven by only a handful of categories such as airfares, hotel rates, and used vehicles. In that context, it would be reasonable for a consumer to assume that inflation would recede as soon as those categories reverse. However, over the past couple of months, higher inflation is starting to broaden out. For example, the median CPI and trimmed-mean CPI measures calculated by the Cleveland Fed were only 0.2% and 0.4% in April, when the headline and core CPI were +0.8% and +0.9% respectively. This wide gap points to a very narrowly driven spike in prices. In contrast, in September, the headline and core CPI were +0.4% and +0.2% respectively, but the median and trimmed-mean gauges were both +0.5%. This means that last month, the “special factors” were actually pushing inflation lower, while there were broad underlying pressures.

It is easy to imagine that consumers’ inflation expectations may begin to evolve as they see more and more of the products and services that they buy regularly rising rapidly in price.

Of course, taking a step back, there are two fundamental questions about long-term inflation expectations that have never been answered in modern times because inflation has been so stable. First, do consumers have any special insight about inflation? As an economist, I have a reasonable amount of confidence in my ability to project the economy’s behavior over the next year or two, though even over that time horizon, my (and every other economist’s) forecast error is embarrassingly large. Faced with the question that the New York Fed asked, “What will inflation be in Year 5?,” I could offer little more than a guess. I feel much more comfortable hazarding an estimate for a distant but prolonged period, say five or 10 years, than I do offering a projection for a single year that far in the future. I can only imagine that the average consumer has even less to base such a speculative forecast on.

The response to the questioning of the validity and importance of consumers’ inflation expectations would be that they are in a sense a self-fulfilling mechanism. If consumers believe that inflation will remain low in the future, then they will resist price increases in the present. That has largely held over the past few decades, but, if, as is likely, inflation is more of a non-linear process with discrete breaks over time, it is questionable whether consumers’ current expectations, mostly based on the history of the last few decades, are determinative for future inflation.

This is the second looming question about inflation expectations. Are inflation expectations really predictive if economic fundamentals are evolving in a significant way? One can imagine consumers’ thought process going as follows: “Yes, I thought inflation would be low and steady, but that was before I saw all of these labor and product shortages. I understand that firms have to be able to recoup their higher costs, and, by the way, I have lots of extra savings and my wages have surged so I can afford to pay a little more.” If that conversation becomes commonplace, the vigilance of consumers as inflation killers could erode quickly.

The only remotely relevant episode in modern history to compare against would be the late 1960s and early 1970s, when inflation over a period of five to ten years went from very tame (averaging 1.3% from 1960 through 1965) to out of control. It took a number of years of policy errors and bad luck to get there, but undoubtedly inflation expectations were quite low in the early 1960s. We don’t have TIPS breakevens or consumer survey results to examine, but the nominal 10-year Treasury yield over that 1960-1965 period averaged about 60 BPs lower than real GDP growth, suggesting that inflation expectations were extremely low (if not negative).

Thus, low and well-anchored inflation expectations in the early 1960s did not save the economy from a devastating bout of inflation just a few years later. That era teaches us that Fed officials cannot rely on steady inflation expectations to do all of their work for them. If monetary policy remains too easy for too long, there is a risk, though certainly not the inevitability, of an abrupt regime change for inflation. As a result, while policymakers do well to closely monitor inflation expectations, they may not want to rely quite so heavily on consumers to do their heavy lifting for them.