By the Numbers

Weighing corporate debt against securitization for financing

This material is a Marketing Communication and does not constitute Independent Investment Research.

The two largest, public single-family rental operators have both recently tapped the corporate debt market for financing. Despite the single-family rental sector tracking toward a record year of new securitizations, some observers have speculated that more operators could start turning towards senior unsecured debt. The added flexibility of issuing unsecured debt comes at a cost, however, and its use will probably remain restricted to companies with investment grade ratings.

The financing challenge for REITs

Most single-family rental operators are structured as private or public REITs, restricting their ability to growth through retained earnings. REITs are required to distribute a minimum of 90% of their taxable income to shareholders. Growing a REIT nearly always requires tapping sources of outside financing. REITs can raise equity capital by selling more shares, through joint ventures or otherwise attracting outside investors. That process can be slow, expensive, and it dilutes ownership, so debt financing is often preferred.

Secured debt is typically cheaper financing

The asset-backed securities market often provides highly efficient funding. Lenders like collateral and generally will loan money at lower rates when the loan is secured by tangible assets. The higher quality and more liquid the assets, the better. Analysis of recovery rates by S&P Global Ratings shows that senior secured bonds have average nominal recovery rates of 66.9% and discounted recovery rates of 55.9%. Senior unsecured bonds have average recovery rates of 52.3% and 44.9%, respectively. The higher recovery rates for secured debt translates into lower credit risk, all else equal, and a lower cost of funds compared to unsecured debt for the same counterparty. In the event of default, if the liquidation of the assets is not enough to cover the claims of the senior secured debt holders, the residual claims are pari passu with those of the senior unsecured debt holders.

When properly structured, asset-backed securities can have a higher rating than the unsecured debt of the sponsor. A low investment grade or non-investment grade company can often finance high quality assets through asset-backed securitization at a much lower cost of funds than the company could achieve on an unsecured basis. Unfortunately, trying to get a clean apples-to-apples comparison between secured and unsecured debt is tough. SFR securities typically have some combination of prepayment risk, amortization, risk that the coupon may decline over time, substitution risk in the collateral, and extension risk in the loans that can drive yields above that of a plain vanilla, fixed-rate corporate bond—at least for a highly rated issuer.

SFR securitizations vs senior unsecured

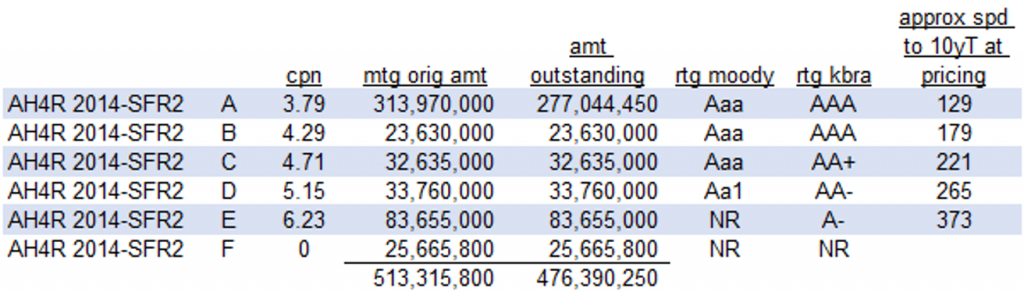

When single-family rental securitizations were still in their infancy, American Homes 4 Rent issued a 10-year, fixed-rate securitization in October 2014 with classes rated from AAA to A- (Exhibit 1). Approximate spreads to the 10-year Treasury, which was trading just above 2.50% at pricing, ranged from 129 bp for the ‘AAA’ front cash flow A class to 373 bp for the ‘A-‘ E class. The debt had a weighted average interest rate of 4.42%. From 2014 through 2015, AMH issued four SFR deals with weighted average interest rates ranging from 4.14% to 4.42%.

Exhibit 1: SFR securitization of American Homes 4 Rent

Note: The AH4R deal priced on 9/10/2014 and has a maturity date of 10/9/2024. The 10-year Treasury was 2.50% and spreads assume the securities were issued at par.

Source: Bloomberg, Amherst Pierpont Securities

Since 2014, SFR spreads have tightened as the market has become deeper and more liquid, the 10-year Treasury is 125 bp lower and credit spreads are hovering near post-2007 lows. Strong fundamentals and strong earnings for the second quarter of 2021 for SFR REITs contributed to an excellent opportunity for American Homes 4 Rent and Invitation Homes to tap the corporate debt market (Exhibit 2) for very competitive financing.

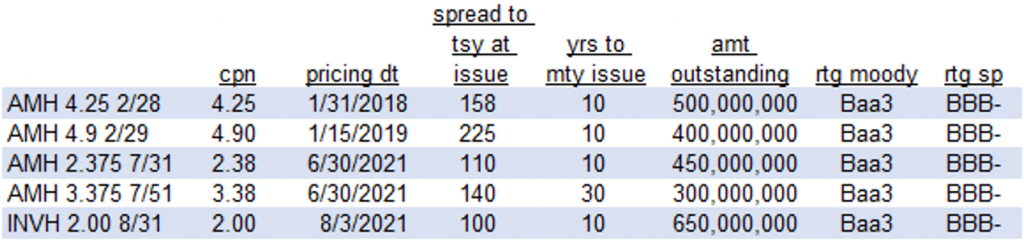

Exhibit 2: Senior unsecured debt of American Homes 4 Rent

Note: In its annual report, AMH notes that they effectively hedged their 2028 notes to yield an interest rate of 4.08% instead of the stated coupon rate of 4.25%.

Source: Bloomberg, AMH 2020 Annual Report, Amherst Pierpont Securities

AMH (Baa3/BBB-) had issued 10-year senior unsecured debt twice before, in 2018 and 2019, at interest rates of 4.25% and 4.90%, which was 158 bp and 225 bp over the 10-year Treasury, respectively. Their June 10-year issue came at 110 bp over Treasuries, while INVH managed to tap the market in August when 10-year Treasury rates were 30 bp lower and managed a spread 10 bp tighter.

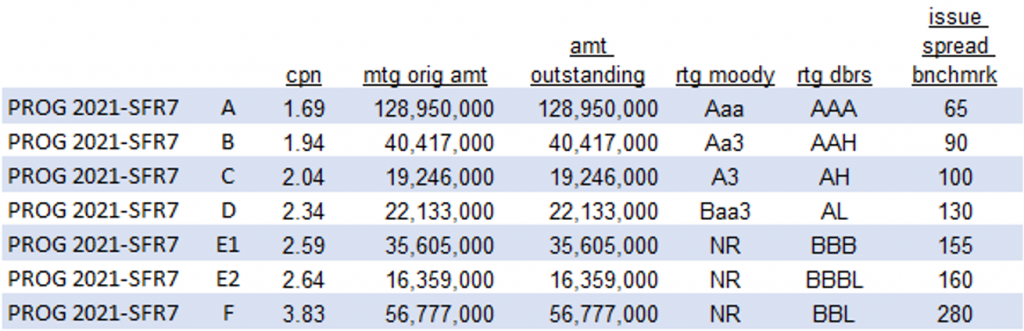

It is difficult to compare the AMH securitizations to its corporate debt precisely. AMH has not financed homes through the SFR securitization channel since 2015, and INVH’s last SFR deal was in October of 2018. Until last year, the home portfolios of both companies were not growing appreciably so there was no strong need for new financing. It is possible to get a ballpark idea of where a new deal might come. Progress Residential priced an SFR deal on July 22 that has a 7-year weighted average life (Exhibit 3).

Exhibit 3: Progress Residential SFR securitization (priced 7/22/2021)

Note: the pricing benchmark for all classes is the 7-year swap rate. The bonds were issued at par.

Source: Bloomberg, Amherst Pierpont Securities

The weighted average coupon for the offered classes is 2.32%, or 128 bp over the 7-year swap rate, which is equivalent to the ‘Baa3/A-‘ D class of the securitization. That 2.32% cost of funds for secured debt can be thought of as roughly in-line with the AMH 2.375% 10-year senior unsecured debt, which has a lower BBB- rating but lacks all the prepayment and other risks embedded in the SFR debt.

Unsecured debt provides more flexibility

Investors can weigh the additional yield of the SFR securities against the added risks of corporate debt from the operator when and if its available. But there is little overlap between buyers of secured and unsecured debt from the same entity.

The upside for issuers is that unsecured debt provides a tremendous amount of additional flexibility, especially around realizing gains in properties. SFR operators who want to refinance, sell or tap equity in their properties are restricted from doing so while the properties are held in the trust backing a securitization. Rules vary across deals, and some do allow for collateral substitution or prepayments, but those allowances are typically on the margin. An operator experiencing rapid home price appreciation cannot easily sell properties to finance growth if they are trapped in a pool.

Other advantages may also draw SFR sponsors. Longer-term debt also reduces refinancing risk for the assets. Build-to-rent initiatives also likely require equity or unsecured financing. And SFR securitizations only finance finished, stabilized properties, not homes under construction. Equity or unsecured financing can allow for growth until construction is complete and an operator can replace it with cheaper, secured funding.

Unsecured debt certainly has a place in the capital structure of SFR operators, especially ones with investment grade ratings that may be able to get low rates. The additional source of financing is likely to drive more growth and eventually lead to a stronger securitized market as opposed to cannibalize SFR.

This material is intended only for institutional investors and does not carry all of the independence and disclosure standards of retail debt research reports. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This message, including any attachments or links contained herein, is subject to important disclaimers, conditions, and disclosures regarding Electronic Communications, which you can find at https://portfolio-strategy.apsec.com/sancap-disclaimers-and-disclosures.

Important Disclaimers

Copyright © 2026 Santander US Capital Markets LLC and its affiliates (“SCM”). All rights reserved. SCM is a member of FINRA and SIPC. This material is intended for limited distribution to institutions only and is not publicly available. Any unauthorized use or disclosure is prohibited.

In making this material available, SCM (i) is not providing any advice to the recipient, including, without limitation, any advice as to investment, legal, accounting, tax and financial matters, (ii) is not acting as an advisor or fiduciary in respect of the recipient, (iii) is not making any predictions or projections and (iv) intends that any recipient to which SCM has provided this material is an “institutional investor” (as defined under applicable law and regulation, including FINRA Rule 4512 and that this material will not be disseminated, in whole or part, to any third party by the recipient.

The author of this material is an economist, desk strategist or trader. In the preparation of this material, the author may have consulted or otherwise discussed the matters referenced herein with one or more of SCM’s trading desks, any of which may have accumulated or otherwise taken a position, long or short, in any of the financial instruments discussed in or related to this material. Further, SCM or any of its affiliates may act as a market maker or principal dealer and may have proprietary interests that differ or conflict with the recipient hereof, in connection with any financial instrument discussed in or related to this material.

This material (i) has been prepared for information purposes only and does not constitute a solicitation or an offer to buy or sell any securities, related investments or other financial instruments, (ii) is neither research, a “research report” as commonly understood under the securities laws and regulations promulgated thereunder nor the product of a research department, (iii) or parts thereof may have been obtained from various sources, the reliability of which has not been verified and cannot be guaranteed by SCM, (iv) should not be reproduced or disclosed to any other person, without SCM’s prior consent and (v) is not intended for distribution in any jurisdiction in which its distribution would be prohibited.

In connection with this material, SCM (i) makes no representation or warranties as to the appropriateness or reliance for use in any transaction or as to the permissibility or legality of any financial instrument in any jurisdiction, (ii) believes the information in this material to be reliable, has not independently verified such information and makes no representation, express or implied, with regard to the accuracy or completeness of such information, (iii) accepts no responsibility or liability as to any reliance placed, or investment decision made, on the basis of such information by the recipient and (iv) does not undertake, and disclaims any duty to undertake, to update or to revise the information contained in this material.

Unless otherwise stated, the views, opinions, forecasts, valuations, or estimates contained in this material are those solely of the author, as of the date of publication of this material, and are subject to change without notice. The recipient of this material should make an independent evaluation of this information and make such other investigations as the recipient considers necessary (including obtaining independent financial advice), before transacting in any financial market or instrument discussed in or related to this material.

Important disclaimers for clients in the EU and UK

This publication has been prepared by Trading Desk Strategists within the Sales and Trading functions of Santander US Capital Markets LLC (“SanCap”), the US registered broker-dealer of Santander Corporate & Investment Banking. This communication is distributed in the EEA by Banco Santander S.A., a credit institution registered in Spain and authorised and regulated by the Bank of Spain and the CNMV. Any EEA recipient of this communication that would like to affect any transaction in any security or issuer discussed herein should do so with Banco Santander S.A. or any of its affiliates (together “Santander”). This communication has been distributed in the UK by Banco Santander, S.A.’s London branch, authorised by the Bank of Spain and subject to regulatory oversight on certain matters by the Financial Conduct Authority (FCA) and the Prudential Regulation Authority (PRA).

The publication is intended for exclusive use for Professional Clients and Eligible Counterparties as defined by MiFID II and is not intended for use by retail customers or for any persons or entities in any jurisdictions or country where such distribution or use would be contrary to local law or regulation.

This material is not a product of Santander´s Research Team and does not constitute independent investment research. This is a marketing communication and may contain ¨investment recommendations¨ as defined by the Market Abuse Regulation 596/2014 ("MAR"). This publication has not been prepared in accordance with legal requirements designed to promote the independence of research and is not subject to any prohibition on dealing ahead of the dissemination of investment research. The author, date and time of the production of this publication are as indicated herein.

This publication does not constitute investment advice and may not be relied upon to form an investment decision, nor should it be construed as any offer to sell or issue or invitation to purchase, acquire or subscribe for any instruments referred herein. The publication has been prepared in good faith and based on information Santander considers reliable as of the date of publication, but Santander does not guarantee or represent, express or implied, that such information is accurate or complete. All estimates, forecasts and opinions are current as at the date of this publication and are subject to change without notice. Unless otherwise indicated, Santander does not intend to update this publication. The views and commentary in this publication may not be objective or independent of the interests of the Trading and Sales functions of Santander, who may be active participants in the markets, investments or strategies referred to herein and/or may receive compensation from investment banking and non-investment banking services from entities mentioned herein. Santander may trade as principal, make a market or hold positions in instruments (or related derivatives) and/or hold financial interest in entities discussed herein. Santander may provide market commentary or trading strategies to other clients or engage in transactions which may differ from views expressed herein. Santander may have acted upon the contents of this publication prior to you having received it.

This publication is intended for the exclusive use of the recipient and must not be reproduced, redistributed or transmitted, in whole or in part, without Santander’s consent. The recipient agrees to keep confidential at all times information contained herein.