The Big Idea

Look for banks to move from cash to securities

Steven Abrahams | July 30, 2021

This material is a Marketing Communication and does not constitute Independent Investment Research.

The pace of bank deposit growth and bank investing has slowed steadily over the last few quarters and looks set to slow further. Federal spending, QE and growth all point in that direction. But that has not taken the pressure off banks to deliver earnings. Loan demand looks anemic, and expense reduction looks played out. Then there is that big stockpile of cash on bank balance sheets. It should start to get reallocated into securities.

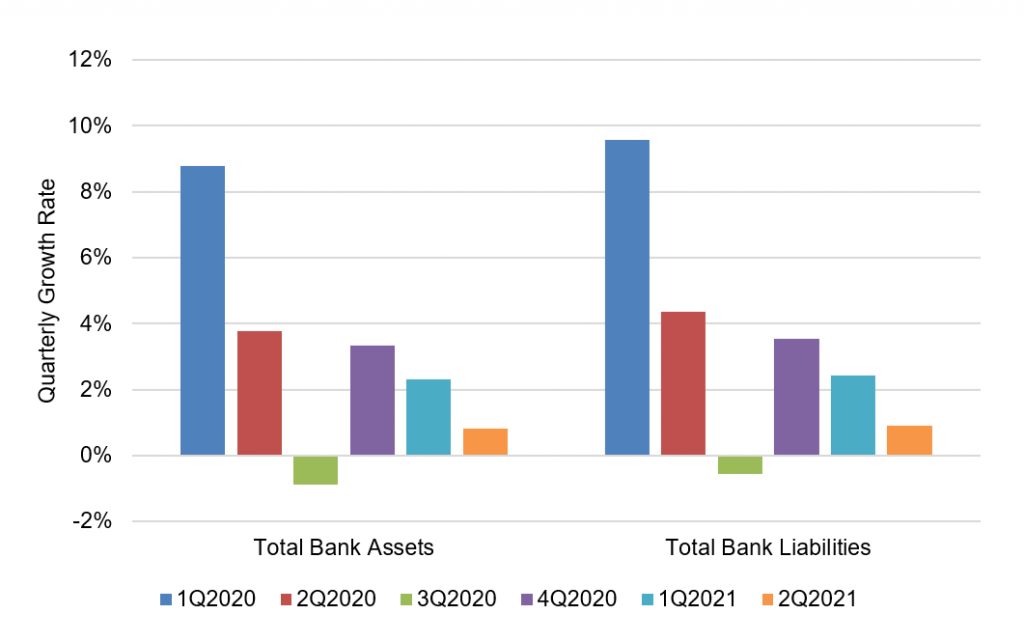

Bank liability growth has dropped way off from early 2020 and has continued to slow over the last three quarters, and asset demand has come down with it. Fed QE and the CARES Act helped turbocharge liability growth in the first quarter last year by 9.6% and in the second quarter by 4.4% (Exhibit 1). After slipping in the third quarter, liability growth in the fourth quarter rebounded to 3.5%. This year the first quarter saw liability growth of 2.4% and second quarter growth of 0.9%. Asset growth has run in perfect parallel.

Exhibit 1: Asset and liability growth has slowed steadily since early 2020

Source: Federal Reserve H.8, Amherst Pierpont Securities

The slowdown should continue, thanks partly to a diminishing fiscal lift and eventually to tapering of QE. Congressional Budget Office projections show federal spending for fiscal 2022, which starts October 1, 2021, dropping by $1.3 trillion or 19%. New infrastructure legislation could change that, but infrastructure spending is likely to get spread out over five years or more. Fed tapering could also trim QE contributions to deposit growth through 2022. Economic growth could pick up some of the slack from fiscal and monetary policy, but CBO, Fed and private forecasts see growth slowing into calendar 2022. Large banks also saw temporary Fed rules lapse at the end of March that made it easier to expand their balance sheet with Treasury debt and excess reserves, and that has led some to discourage growth.

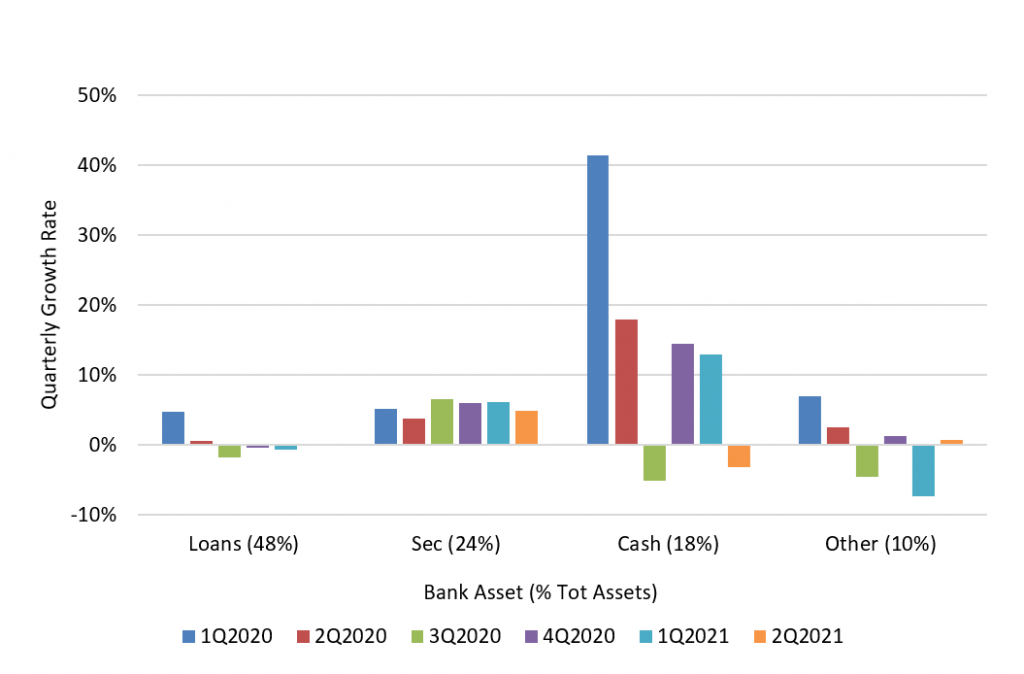

Slower deposit growth should take some pressure off banks to invest the deposits, but the latest quarter of bank earnings underscored low expectations for loan demand, and that keeps the earnings pressure on. Banks hold 48% of their assets in loans, but growth has been anemic. PPP loans helped lift loan growth in the second quarter last year, but it has dropped every quarter since before eking out 0.2% growth last quarter (Exhibit 2). Banks have steadily grown securities holdings, which now make up 24% of assets. Cash asset growth has swung wildly, with cash now making up 18% of assets. All other assets make up the balance.

Exhibit 2: Anemic loan growth, steady securities growth, variable cash and other

Source: Federal Reserve H.8, Amherst Pierpont Securities

Banks look likely to respond to earnings pressure by allocating out of cash in coming quarters and into anything else. Balances in cash assets—mainly excess reserves—dropped in the second quarter with balances in loans, securities and other assets up. Collecting 15 bp in IOER likely will not help hit earnings targets, so cash should flow first to loans, next to securities and then to other assets. But with loan demand low—corporations and consumers have ample cash on hand and limited need for net borrowing—securities should absorb the largest share of the reallocation. The overall size of bank investment flows should drift lower, but securities could get a rising share.

The incentives of running a bank these days will still likely point bank portfolios toward relatively safe, liquid assets. Portfolios traditionally provide the liquidity to fund lending or M&A. And while loan demand may lag for a few quarters, the incentives for M&A have only become stronger. Balance sheets rich in capital and liquidity along with low current yields have made it harder to generate earnings, so many banks have focused on expenses. But the easiest expense reduction is past, and many banks last quarter told the market to expect expenses to rise. If expenses start to squeeze earnings, M&A only becomes more compelling. And M&A creates incentives to have big blocks of liquidity sitting in the portfolio.

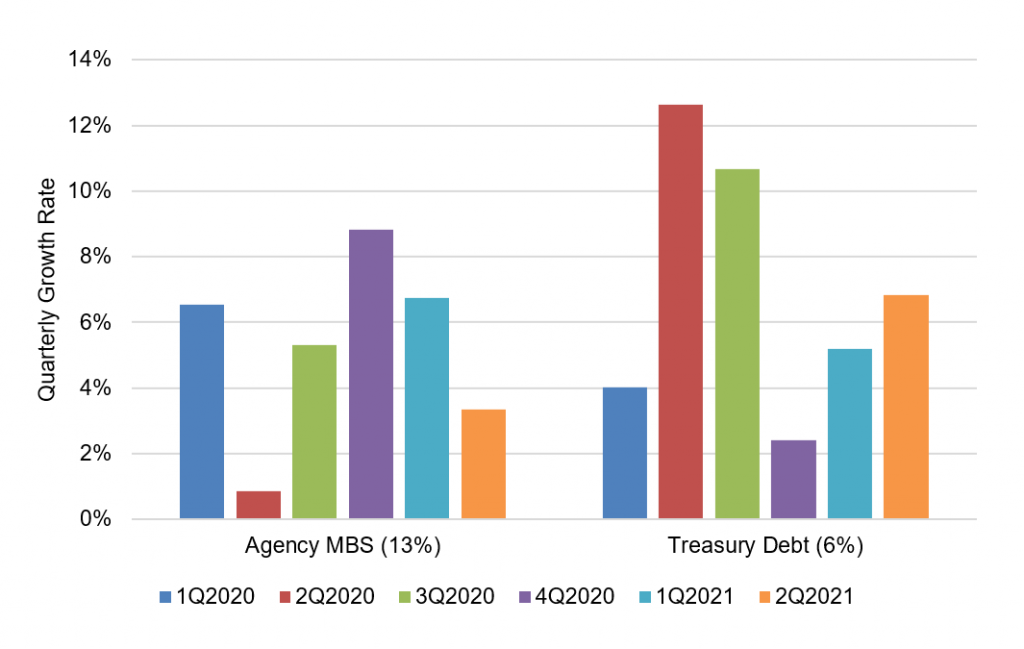

That puts banks solidly in the market for Treasury debt and agency MBS. Holdings in both assets have grown in each of the last six quarters, with Treasury holdings showing surprising growth (Exhibit 3). The Treasury growth speaks to the value banks assign to liquidity even at the expense of some yield and earnings.

Exhibit 3: Steady growth in holdings of agency MBS and Treasury debt

Source: Federal Reserve H.8, Amherst Pierpont Securities

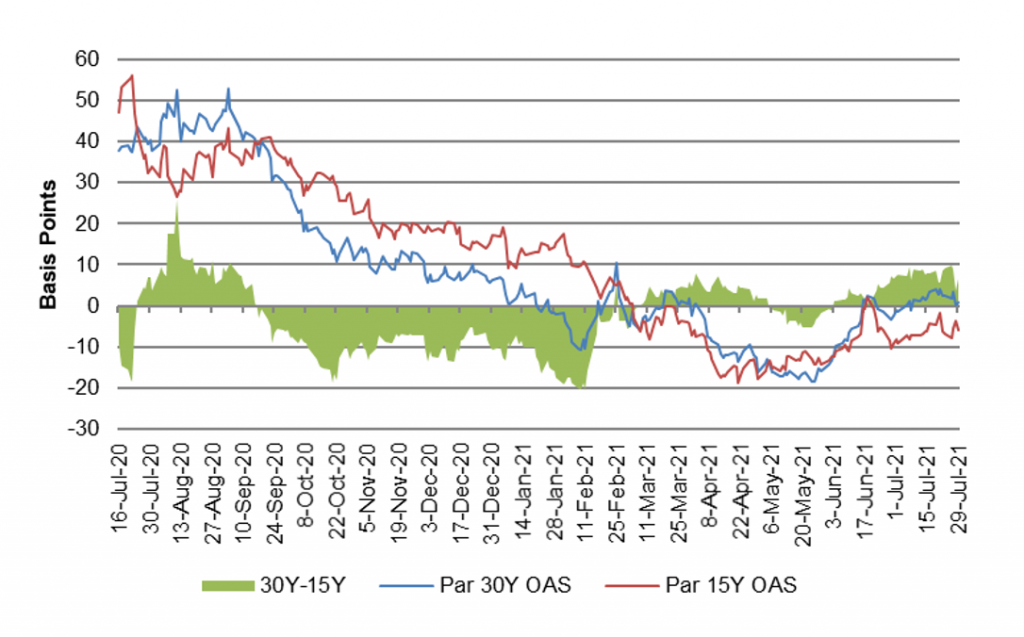

The market for 15-year pass-throughs anecdotally has seen the impact of bank demand for a balance of liquidity and yield along with lighter supply in the last few months. Spreads there have largely held their ground while 30-year pass-throughs have widened (Exhibit 4). A 15-year pass-through amortizes principal faster and has better convexity, both good things for bank portfolios.

Exhibit 4: Better performance in 15-year MBS likely reflects a good bank bid

Source: Bloomberg, Amherst Pierpont Securities

Some banks have started exploring assets with more yield and less liquidity such as non-agency MBS and CLOs, but these tend to be smaller banks where a modest amount of exposure can add material net interest income. With most banks awash in capital, concerns about the capital required for these assets in a stress test is less of a factor. The balance of yield and steady return of principal in ‘AAA’ non-QM MBS and in short CLOs make a strong case for adding them to a bank balance sheet.

* * *

The view in rates

Fed RRP balances closed Friday at a record $1.04 trillion. The Treasury General Account at the Fed still holds $128 billion more in funds than the Treasury’s $450 billion target at the end of July, so it is possible more cash will flow into the money markets and end up posted to the RRP.

Settings on 3-month LIBOR have remained steady over the last week at around 12.5 bp, still near the lowest setting ever. Fed tapering should keep cash pouring into the front end into the second half of 2022, so money market rates look likely to remain low into 2022, as well.

The 10-year note has finished the most recent session at 1.23%, down 5 bp on the week. Breakeven 10-year inflation is at 240 bp, up on the week by 5 bp. The 10-year real rate finished the week at negative 117 bp, down 10 bp on the week. Real rates are driving the market and are pricing in a massive and persistent supply of cash in excess of demand to borrow.

The Treasury yield curve has finished its most recent session with 2s10s at 104 bp, 4 bp flatter than a week ago. The 5s30s curve has finished at 119 bp, flatter by 1 bp.

The view in spreads

Prospects for credit look more promising than for MBS. In credit, benchmark investment grade cash spreads are tighter by 1 bp from the end of May and should continue to outperform. Demand from mutual funds, international portfolios and insurers looks healthy. Low rates should continue supporting corporate balance sheet strength. Ratios of EBITDA to interest expense are in the middle of the range despite high ratios of debt to EBITDA. Investor demand for yield should keep spreads relatively tight. A strong economy should help credit spreads, but relative value flows at money managers could still soften credit spreads if MBS gets wide enough.

The prospect of Fed tapering and heavy net supply should keep weighing on MBS spreads until the Fed shows its hand and the market can price the impact. The market has already priced additional risk of soft demand and steady supply, with the nominal spread of par 30-year MBS to the 7.5-year Treasury at 72 bp, wider from the end of May by 10 bp. Spreads look vulnerable to going still wider as the Fed likely leans into tapering or tapering-and-hiking faster than its 2013-to-2015 cycle.

The view in credit

Fundamental credit looks strong and generally continues to improve, helped by Covid reopening and low rates. Consumers finished the first quarter of 2021 with net worth up $5 trillion. The second quarter should add to consumer net worth with equities and real estate higher and rates even lower. Consumers have not added much debt. Corporate balance sheets have taken on more leverage, although mitigated by strong cash balances and low interest costs. EBITDA-to-interest-expense is at healthy levels. Strong economic growth in 2021 and 2022 should lift most EBITDA and continue easing credit concerns. Eventually, rising interest expense in 2023 should compete with EBITDA growth. Fundamental credit should hinge on whether the Fed can orchestrate a soft landing as it starts to tighten financial conditions.